A few months ago I wrote The Art Of Doing Nothing, in which I argued that, while it may be the most difficult thing for an investor to do, the vast majority of the time an investor should simply do nothing at all. Truly wonderful opportunities don’t come around very often but having the patience to wait for them is what separates the best investors on the planet from the rest.

However, it’s not only the waiting that is critical to success; it is also the courage to act when the time arises. Aside from being too active, another major mistake investors make is simply being too timid, or becoming too comfortable with doing nothing at all and this can be just as costly if not even more so. As Warren Buffett has said, mistakes of omission, or failing to act, have cost him far more than mistakes of commission, or acting when he shouldn’t have.

I have written a great deal about the opportunity in energy over the past few months. In fact, my proverbial fists are sore from pounding the table. As I wrote in The Art Of Doing Nothing, “When it comes time to actually do something, to put money to work, you will know by the fact that it is such an attractive opportunity you would be foolish not to take advantage of it,” and I have done my level best to describe the situation in energy as just such an opportunity.

Most investors, however, are either oblivious or are in some stage of disbelief. “When a truly terrific opportunity arises they are paralyzed by the fear of going it alone, without the comfort of the company of others, ala stocks in 2009, real estate in 2012 or gold in 2015. Or they just aren’t paying attention,” is how I described it in that earlier piece. Before energy’s recent rally, I suspect most were too fearful. Now they either believe they missed it or that it’s just another false dawn.

But this is exactly what it feels like at the beginning of a major bull market. Skepticism towards a rally is the healthiest sign you’ll find and the skepticism towards the rally in energy is so thick you could cut it with a knife. Bloomberg ran an editorial last week very critical of Exxon Mobil even after the stock put in its best monthly performance in history. It also ran, in the most glaring headline I’ve ever seen, a story proclaiming, “Peak Oil Is Suddenly Upon Us.”

But this is exactly what it feels like at the beginning of a major bull market. Skepticism towards a rally is the healthiest sign you’ll find and the skepticism towards the rally in energy is so thick you could cut it with a knife. Bloomberg ran an editorial last week very critical of Exxon Mobil even after the stock put in its best monthly performance in history. It also ran, in the most glaring headline I’ve ever seen, a story proclaiming, “Peak Oil Is Suddenly Upon Us.”

These are not the sort of signs you see at the end of a rally. They are precisely the sort of signs you see when it’s time to be buying with both hands. The trick is learning to feel FOMO when you should feel it, when it feels like nobody else in the world could imagine feeling it, rather than allowing yourself to feel FOMO at a time when everyone else is actually feeling it.

And to that latter point, there are a growing number of signs suggesting we have reached new levels of FOMO in the broad stock market. The day before Thanksgiving saw 35 million call options traded, a daily record. Volume on the Nasdaq during the holiday-shortened week was double what it was last year. Over the past 20 days, an average of 20 million calls have traded, also a record. Last month, equity ETFs took in $81 billion, another record. Rydex traders bullish positioning is also at a record extreme.

Everywhere you look there are signs of euphoria like we have never seen before. As Jeremy Grantham told the Financial Times, “There is as much craziness now as there was in late 1999 or 1929. It is bewildering, impressive and for financial historians like me, exciting. This is the real thing… It looked like we were in a bubble mode this summer, but the real craziness has come out in the last few months.”

As I have written before, it’s very reminiscent of what we saw 20 years ago in late-1999 and into 2000. Back then, fears of how computers may have reacted when the calendar rolled from 1999 to 2000 inspired a massive upgrade cycle in both software in hardware. After the date rolled over and there were no problems, a black hole of demand materialized and, as soon as revenue growth rates began to decelerate, stocks began to plunge.

Investors had bid stock prices up as if the growth rates were sustainable indefinitely into the future. When it became clear that that was a miscalculation the fallout was fast and furious. A similar reckoning awaits the market today. Investors have once again bid stocks to the moon under the assumption that their pandemic-boosted growth rates were sustainable indefinitely.

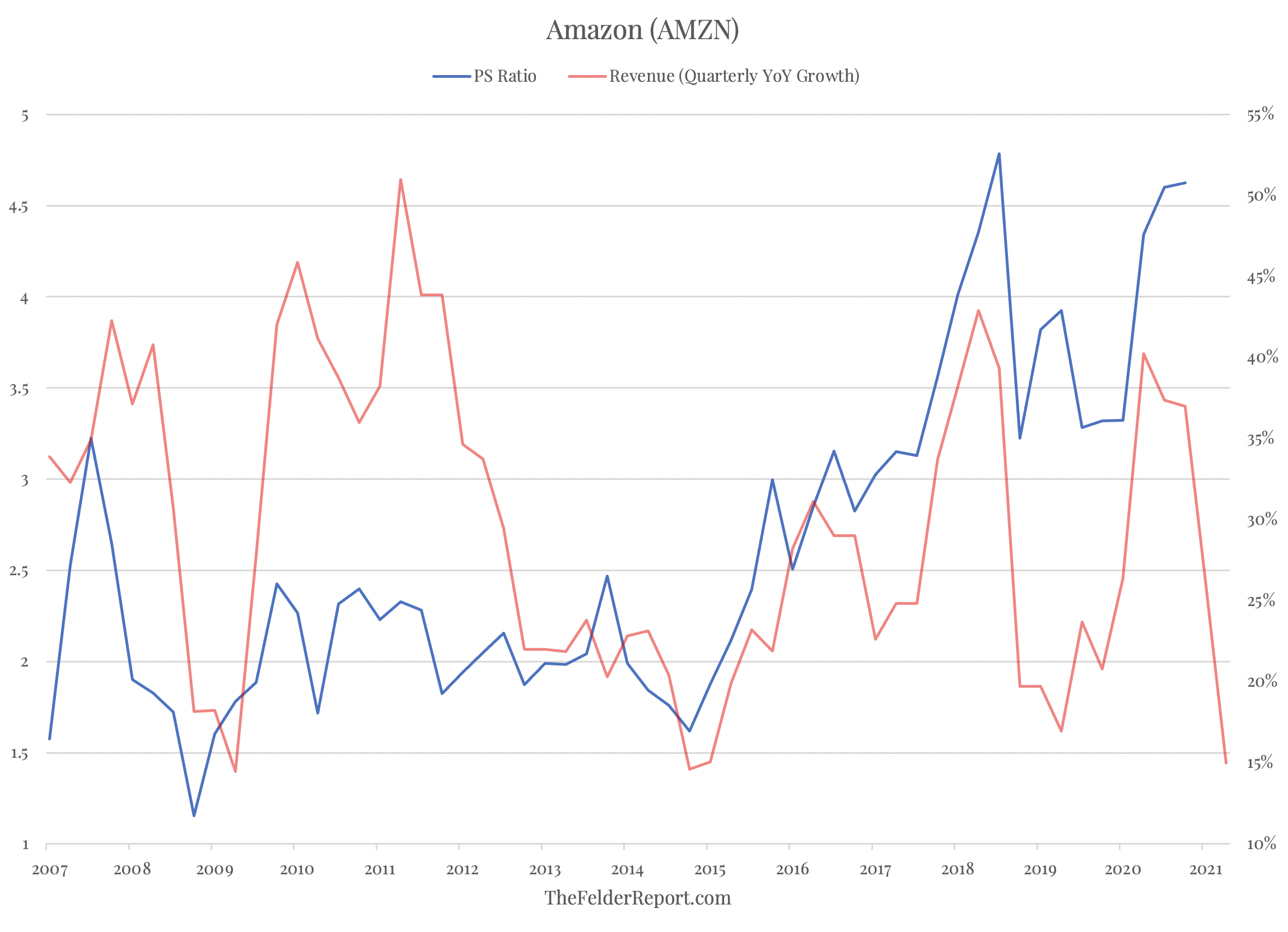

However, another black hole of demand will soon materialize. And first quarter numbers will be the first to show a deceleration in growth for many firms. Amazon, for one, is already showing a deceleration. Second quarter revenue growth for the company was 40% year-over-year. Third quarter was 37% and fourth quarter is expected to match that. First quarter next year, though, is expected to fall to 26% and the quarter after that, when comps really start to get difficult, is expected to be just 15%.

The last time Amazon saw revenues grew more than 40% (almost a decade ago) its price-to-sales ratio was half what it is today. What should its valuation be then when revenue growth is more than cut in half? And there are far more extreme examples of this dynamic. Generally, though, the most popular stocks in the market have all benefitted, to some degree, from the pandemic. They all will start facing very tough comparisons over the next few quarters.

The last time Amazon saw revenues grew more than 40% (almost a decade ago) its price-to-sales ratio was half what it is today. What should its valuation be then when revenue growth is more than cut in half? And there are far more extreme examples of this dynamic. Generally, though, the most popular stocks in the market have all benefitted, to some degree, from the pandemic. They all will start facing very tough comparisons over the next few quarters.

And just as they begin to face these tough comparisons, which peak in the second quarter of next year, the pandemic could be coming to an end. There is a certain amount of surplus demand that could immediately evaporate for products and services boosted by the pandemic once it’s over. It’s not hard to imagine revenue growth not just decelerating for many of these companies then but actually flatlining or turning negative. The market is already overdue in pricing in this sort of risk.

By the same token, just as there has grown a certain amount of surplus demand for these companies, there is now a measure of pent-up demand for products and services rendered unavailable by the pandemic. It’s end could usher in more than just a return to normal; it could mean a boom like we haven’t seen in a very long time.

As Paul Tudor Jones told Yahoo!Finance, “The vaccine’s going to bring us back. We’re going to have an incredible growth rebound. I have four kids in their 20s. And, it’s like a horse at the beginning of a race. They’re so ready to get to see their friends, to get to restaurants, to vacation. They’re just ready to get out and go crazy, like I think everyone else in the world.”

The situation for energy is perhaps the most explosive. Production has been cut dramatically and, for a number of reasons, cannot be ramped back up easily here in the U.S. if at all. Oil inventories are already falling even amidst the current economic weakness. For this reason, “the imminent danger is not the collapse of fossil fuel use; the imminent danger is an oil supply shortage and oil price shock,” as Steven Bregman recently wrote.

Meanwhile, energy is still priced as if it’s going out of business. The bullish disconnect is one of the largest I’ve seen in my career. Similarly, the bearish disconnect between prices and fundamentals for the broad stock market, largely driven by tech, is also unquestionably one of the largest I’ve seen.

However, there is no opportunity without these sort of disconnects so you might otherwise phrase it as these are two of the greatest opportunities I’ve seen in my career: one to go long, the other to go short. I would never claim that either one would be suitable for the faint of heart. In fact, the greater the disconnect, the greater the courage required to take advantage of it. But for those with the courage (and expertise) to do so, the rewards could be spectacular.