Apple reported earnings this week and the latest numbers have some some pounding the table bullish. For example, here’s Forbes from an article titled “Why Apple Is Very Undervalued“:

Apple still trades at 13x earnings. The S&P 500 trades at 16x. Apple trades at 13x next year’s projected earnings. The S&P 500 trades at 16.5x. Clearly it’s undervalued compared to the broader market. What about Apple’s monster cash position? Apple has even more cash now–a record $237 billion. If we excluded the cash from the valuation, Apple trades at 8.6x earnings. Though not an apples to apples (pun), and just for a reference point, that valuation would group Apple with the likes of these S&P 500 components that trade 8x earnings: Dow Chemical, Prudential Financial, Bed Bath & Beyond, a Norwegian chemical company (LBY), and Hewlett Packard Enterprise. It’s safe to say no one is debating whether or not Hewlett Packard is at the pinnacle of its business. Yet, if we strip out the cash in Apple, AAPL shares are trading at an HPE valuation.

There are a few things that are problematic with this analysis. First of all, the S&P actually trades at 25 times trailing earnings not 16. I assume the author is using operating not net earnings in arriving at 16x. So an apples to apples comparison (please excuse the pun) makes Apple look even cheaper relative to the broad market. But I’ve never found this to be a terribly valuable way to determine whether a stock is cheap or not.

The other problem with this analysis is that if you want to back out Apple’s cash you also have to consider all of the debt the company has piled up in recent years. In fact, as MarketWatch reports today, Apple actually added more debt to their balance sheet than cash last quarter. The $237 billion in cash is not nearly so impressive when you consider the company is now on the hook for $87 billion in debt. Net cash then is only $150 billion. I agree that factoring in a company’s net cash or net debt gives you a better picture of their overall financial valuation but looking at just the cash and not the debt is deceiving.

Subtracting the net cash out of Apple’s $620 billion market cap yields an enterprise value of $470 billion. Still, to compare this number to earnings is also deceiving when the company earns more than a billion dollars per year simply in interest income. Yes, that might be a trivial amount for a company of Apple’s size but we should still be diligent about comparing apples to apples. Backing out the interest income, Apple earned $44 billion last year. It currently trades at an enterprise value roughly 10.7x that number, not 8 as the Forbes author would have you believe.

Again, 11x might look cheap relative to the 25x the broad stock market trades at but I find little utility in this approach. In fact, Apple has traded at a discount to the broad market for years now and investors might want to try to understand why it has been persistently “undervalued.” Apple trades at $115 per share today. It first hit this level almost two years ago. That was the last time I wrote about the stock, revealing why I was selling it. I first bought the stock in early 2013 because I thought it was cheap back then. At the time, I wrote:

The current market capitalization is $422 billion (938 million shares times $453 per share). Back out the cash of $137 billion [Apple had no debt at the time] and you get an enterprise value of $285 billion. That amounts to a mere 6 times the company’s free cash flow over the past twelve months. In other words, investors get a 16.6% free cash flow return on their investment at the current share price. What’s more, Apple, on an enterprise value to EBITDA measure, is now cheaper than the likes of Microsoft and Radio Shack.

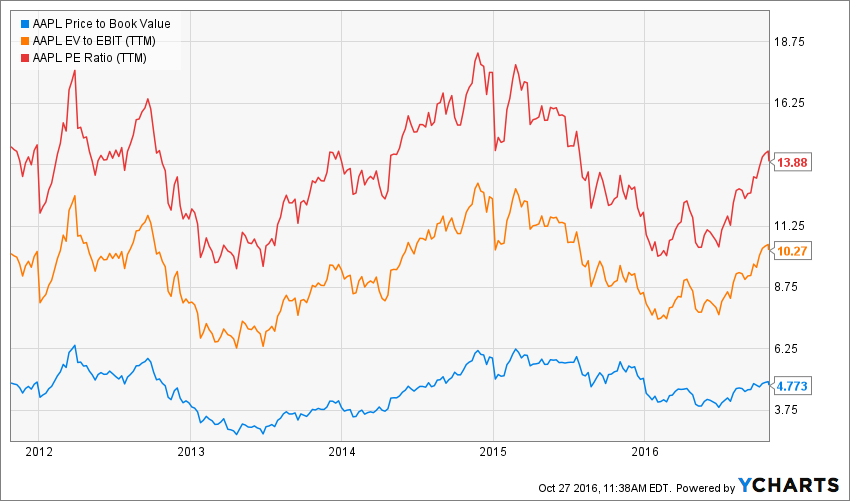

Even when you don’t back out the cash in its bank accounts the stock currently trades at its cheapest valuation at any time over the past decade. Over that time, Apple’s stock price has typically found a bottom near 10 times gross cash flow. In 2011, it bottomed at 8.5 times cash flow before running 75% higher over the next 12 months. Today, it trades at 7.5 times cash flow. Any way you slice it that’s damn cheap and for one of the most admired brands/most profitable companies in history.

I like to compare a company’s valuation to its own history and to its peers in determining whether it’s cheap or not. In early 2013, it was cheap by both standards but let’s update these numbers to see if it’s still true today. Apple’s enterprise value today is nearly 9x its free cash flow, versus 6x back in early 2013. And if you look at any number of other valuation measures, the stock currently trades right in line with its own 5-year averages. Based on its own history, then, the stock is not cheap; it’s just in line with average.

The real thing investors need to consider, though, with Apple is the fact that sales back in 2013 were still growing very fast. The stock traded 6x free cash flow while sales were still growing 18% year-over-year. Furthermore, Apple hadn’t even begun to sell iPhones in China yet so it still had a huge growth opportunity in front of it. Today, the stock trades 9x FCF and sales are falling nearly 8% year-over-year. Operating income is falling at an even faster 15% clip. Furthermore, there is no layup growth opportunity out there like there was back then that I can see.

Sure, Apple is spending very heavily on research and development that may pay off in the future. As an investor, though, this is very difficult to value (and this might have been why the greatest value investor of all time recently sold out of his position). Can Apple come up with another product as popular and as profitable as the iPhone? Or is the company just a one-hit-wonder? Personally, I think this is an open question. And investors are free to gamble on this outcome but that’s not really investing, is it?

Related: