As Bloomberg recently reported, stock buybacks are now running at over $40 billion per month. With margin accounts already maxed out and households along with the largest sovereign wealth funds already “all in,” buybacks now represent the single greatest source of demand for equities.

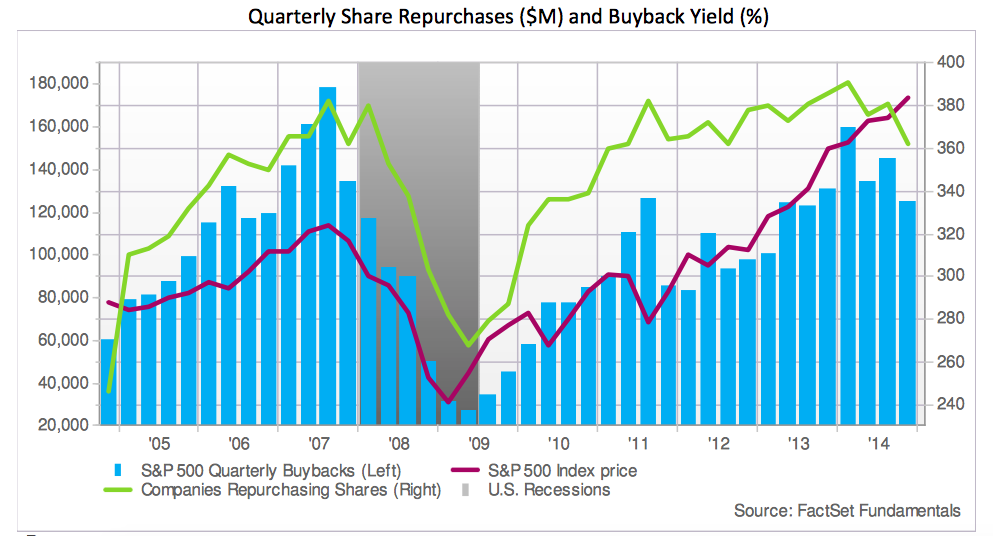

On the surface, this should give investors great comfort. Stock buybacks may be the most effective way for companies lacking growth opportunities to enhance shareholder value. Look a little deeper, however, and this fact should give investors pause. Why? Because companies may be the worst market timers there are. They routinely set buyback records at major market peaks and buy only a tiny fraction of that amount at major bottoms. Chart via Factset

Chart via Factset

How can that be? Shouldn’t the companies be in the best position to most accurately estimate their own intrinsic value and future prospects and thus most effectively buy low and sell high? Yes BUT companies are far more capable of buying back stock when cash is plentiful – when money is easy to borrow and profits are high.

The time when money is easy to borrow and profits are high, however, usually coincides with high equity prices. When money is hard to borrow and profits squeezed like during a recession, stock prices are usually much lower but companies are not in a position to take advantage. Buybacks, then, are very highly correlated with corporate profits and bond market risk appetites.

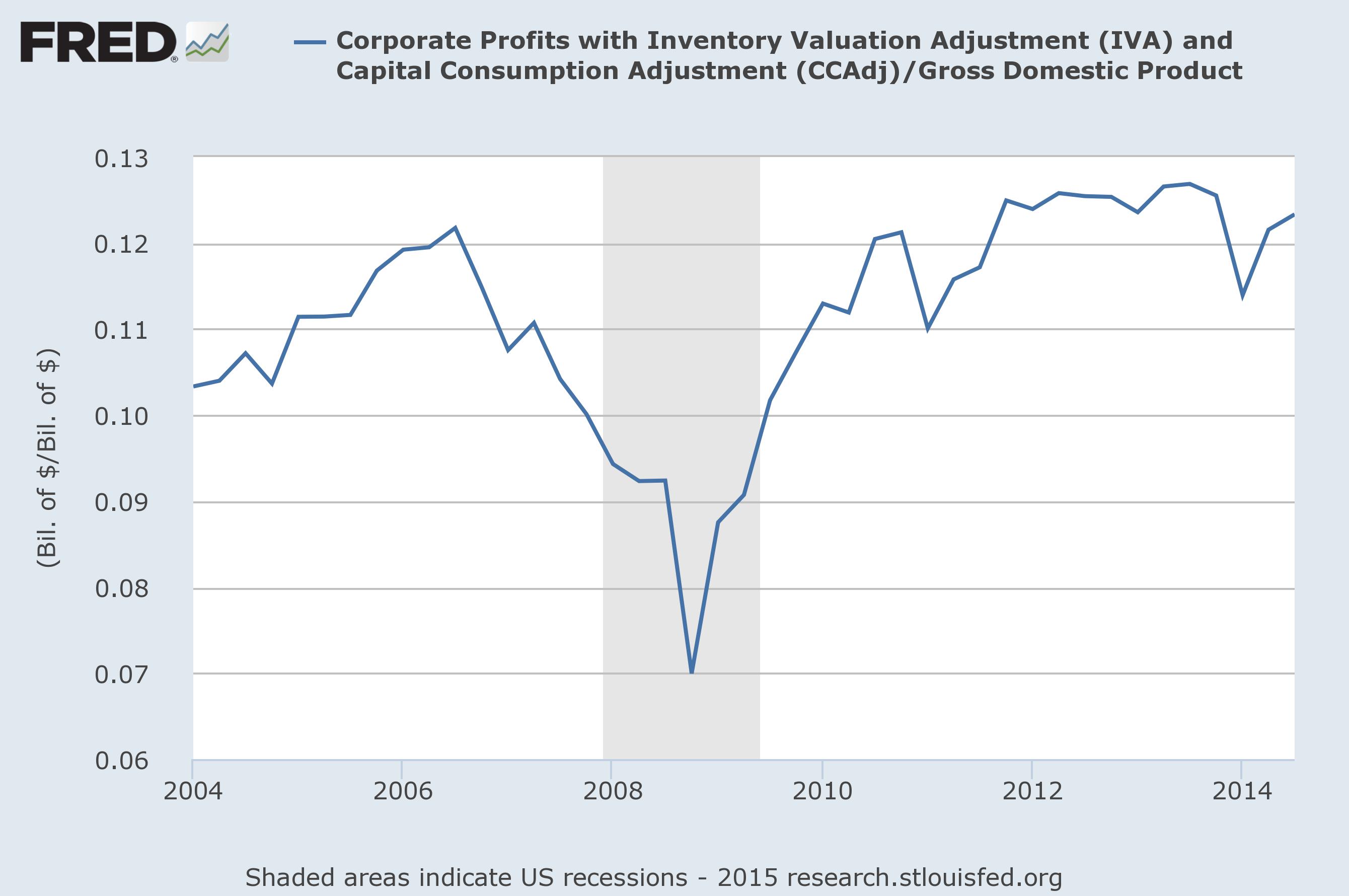

Right now companies are spending fully 95% of their profits on buybacks and dividends. As I recently wrote, profit margins peaked over a year ago. And aggregate corporate profits are expected to decline over the next two quarters for the first time since the great recession. It’s hard to imagine companies being able to maintain near-record buyback levels amid this pressure in profits.

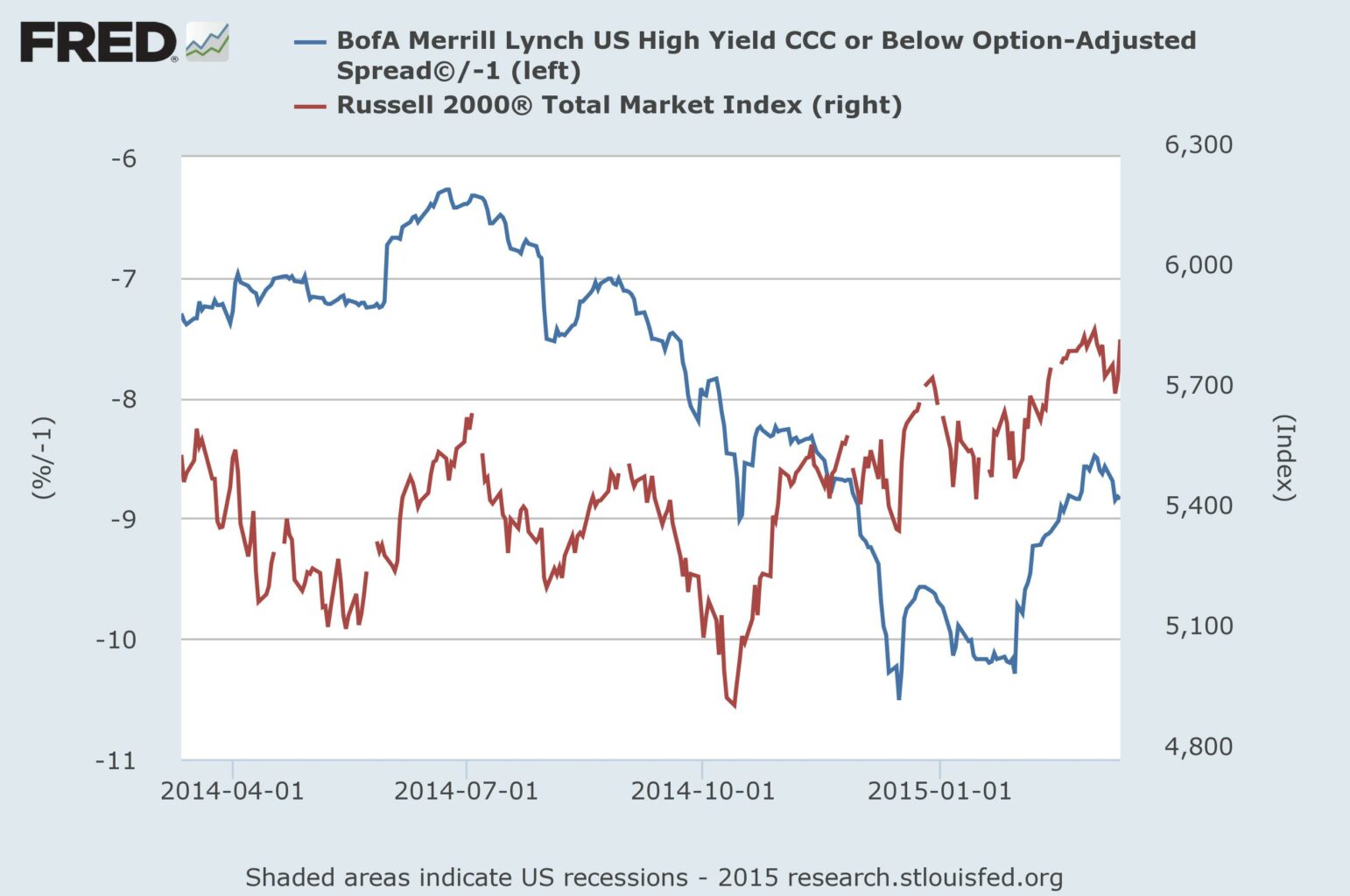

But they can still borrow money to buyback shares, right? Well, borrowing power is also tied to profits and investors’ willingness to buy their debt. I have also written recently that bond market risk appetites peaked last summer and have diverged from equities ever since. Should this trend continue, it would not be supportive of continued buybacks.

All in all then, just like margin traders, households and the largest pension funds on the planet, the greatest source of demand for equities right now may also be maxed out.

A version of this post first appeared on The Felder Report PREMIUM