Junk bonds have been selling off rather dramatically lately and are now testing their October lows. This stands in stark contrast to the strength in stocks which are just off of their all-time highs. This divergence stands out because both asset classes are typically very closely correlated due to the fact that they appeal to similar risk appetites.

However, many market players are reacting to it by saying, ‘don’t worry about junk bonds; it’s different this time.’ They write it off to the energy sector saying that the weakness there will be contained and not extend to anywhere else in the economy. Or they say, ‘great! That’s bullish because it means the Fed will have to be more accommodating for longer.’ This just smacks of classic rationalizing to me. Folks want to stay bullish so they try to spin even the most negative data points that way.

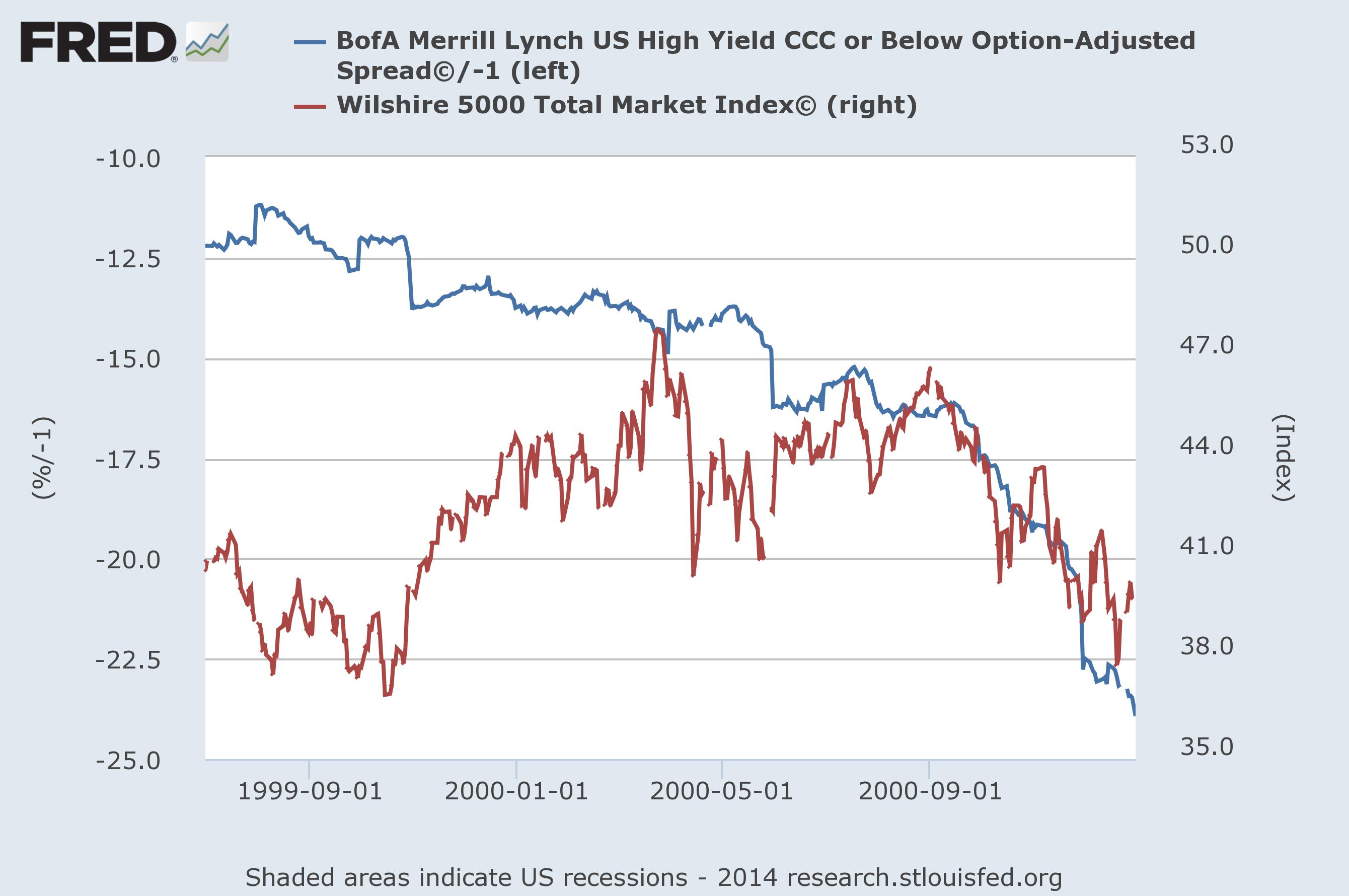

I’d just like to point out a couple of precedents for the weakness we’re now seeing in high-yield. First, way back in 1999-2000, the junk bond market (as measured by yield spreads) diverged from the price high made in late March 2000 suggesting that stocks were missing something. Notice in the chart below that when the stock market (red line) made a new price high in March, high-yield spreads (blue line – inverted) had actually been widening (declining) for months. When stocks tried to make another new high in the fall of that year, high-yield again told a different tale, unable to show any sign of improvement. For those that don’t remember, this marked the beginning of the internet bust.

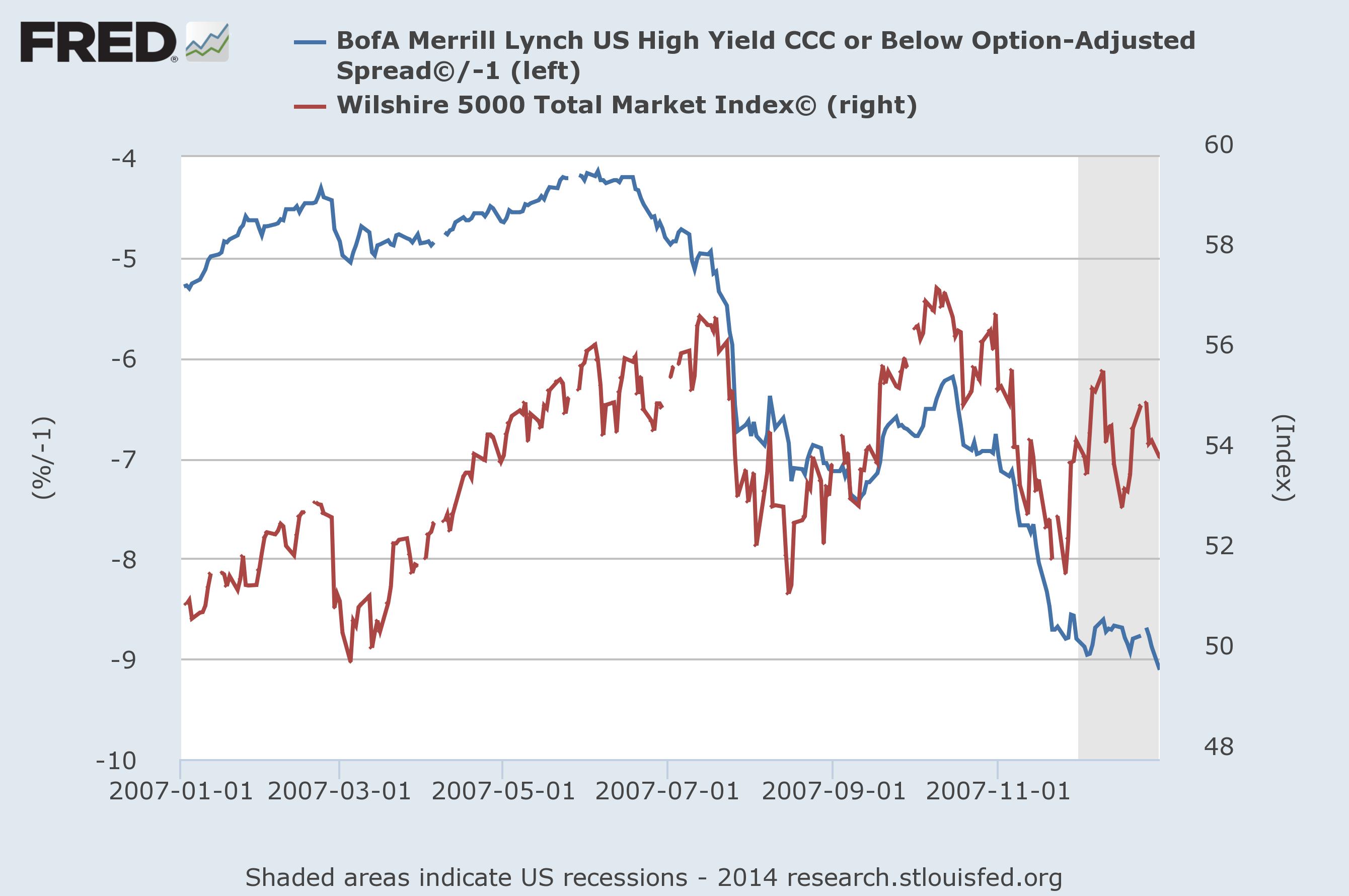

Again in 2007 we saw a similar scenario unfold. Stocks rallied to new highs during the summer of that year even while junk bonds began to roll over. In the fall, stocks made another new high yet high-yield couldn’t manage much more than a small rally. Once again, the bond market was telling a tale the stock market was deaf to. Then came the financial crisis.

Again in 2007 we saw a similar scenario unfold. Stocks rallied to new highs during the summer of that year even while junk bonds began to roll over. In the fall, stocks made another new high yet high-yield couldn’t manage much more than a small rally. Once again, the bond market was telling a tale the stock market was deaf to. Then came the financial crisis.

Today, we’re seeing the very same movie. Stocks recently made new highs even while junk bonds have gotten slammed. This may, in fact, be the greatest disconnect between the two markets as that divergence is just gaping.

Maybe it is different this time. Maybe this weakness in the junk bond market is just, “full of sound and fury, signifying nothing.” But considering the past precedents I think that’s probably not the wisest interpretation.