A few weeks ago I took a look at the margin debt numbers using them to argue that overall demand for stocks could have already peaked. There are plenty of other indicators confirming what this one seems to be saying but this is just one slice of the demand picture. There’s an entirely unrelated demand factor that may be even more troublesome for the stock market.

Before we get to that, however, let’s take a look at the latest margin debt figures. From the chart below, it looks as if investors may have, indeed, run out of buying power. Total margin debt/negative credit balances peaked from all-time record levels just about a year ago and have essentially flatlined since.

Chart via Doug Short

Chart via Doug Short

Taking a look at Rydex funds, the ratio between bullish and bearish funds is now greater than it was at the peak of the internet bubble, mainly because almost nobody sees the need for downside protection anymore (see assets in bear funds and the bottom of the chart). Even total capitulation by those invested in bearish funds would not move the needle much in terms of demand for stocks.

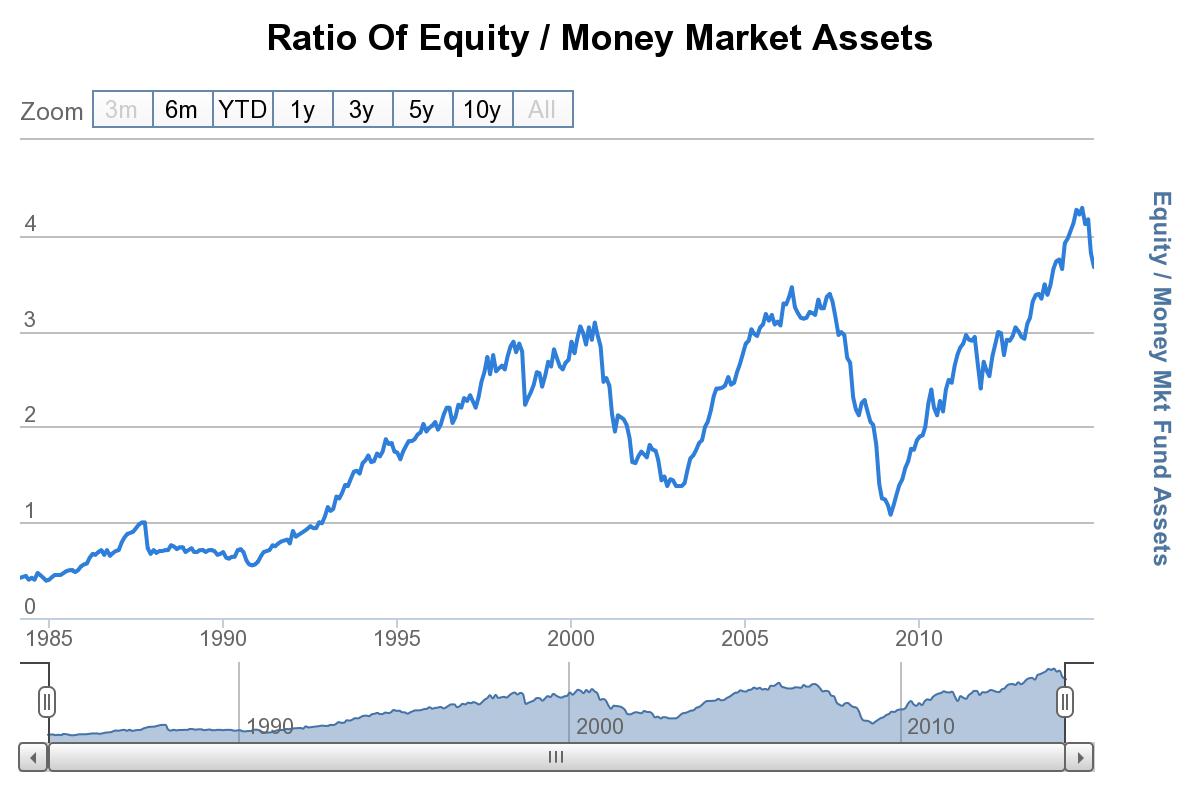

This is also confirmed by the total amount of money invested in equity funds in relation to money market funds. Like the Rydex indicator, the bullishness expressed here has never been higher. Of course, more money could flow from money market funds into equities but, considering how this indicator is already historically stretched, it doesn’t seem likely.

Chart via SentimenTrader

Chart via SentimenTrader

What may be the most fascinating and underreported aspect of the demand picture, however, is the incremental demand the equity market has seen from sovereign wealth funds over the past few years. Considering these hold roughly $7 trillion in assets today, they are no small factor in the discussion.

The two largest funds in Japan and Norway now have equity allocations over 50%. This is already a fairly aggressive allocation these days for large pension-type plans so it’s not likely they will significantly increase this exposure. We certainly won’t see Japan go from a 0% allocation to equities to 50% again as we have recently.

And there is an interesting case to be made that this growing demand could be tapped out, or worse, convert to supply at some point in the near future. I’ll let Marc Faber, via Barron’s, explain:

Sovereign wealth funds rose to $6.8 trillion as of September 2014, from $3.2 trillion in 2007. Of that growth, 59% came from oil, gas, and related revenue. As oil prices fall, what will happen to the growth of sovereign wealth funds, which have been buying financial assets around the world? Their funding is going to evaporate, and they might be forced to sell.

If the price of oil doesn’t rebound relatively soon some of these funds may find their source of funding, which has grown dramatically over the past few years, has run dry hence their ability to purchase or even hold their current level of equities.

So domestic investors are already “all in” and foreign investors, via sovereign wealth funds, are essentially as well. Where then does the incremental demand come from to push the stock market higher?

Like these foreign funds, I guess if the social security trust fund could convert those IOUs it holds into dollars they could begin to allocate some of the $2.7 trillion there toward our stock market. However, considering the facts that, unlike other funds which are still growing, the social security trust fund is already facing large annual deficits and is due to run out of money altogether in about 15 years, this would be a very tough sell, especially to a congress now leaning fiscally conservative. And, sadly, these sort of proposals really never gather any steam when it’s truly an attractive time to do so.

All in all, I find it hard to imagine where the demand is going to come from to push stock prices much higher, especially when valuations are already historically stretched and fundamentals seemingly beginning to deteriorate. To me it looks like potential supply far outweighs potential demand at this point. In other words, potential risk far outweighs potential reward.