INDIVIDUAL INVESTOR: Is it time to buy stocks yet?

ME: Actually, I’ve been saying for a while now, ‘please don’t buy anymore stocks,’ and I haven’t changed my mind yet.

II: Why?

ME: Because stocks are extremely overvalued and the potential downside is significant (30-60%).

II: How do you know?

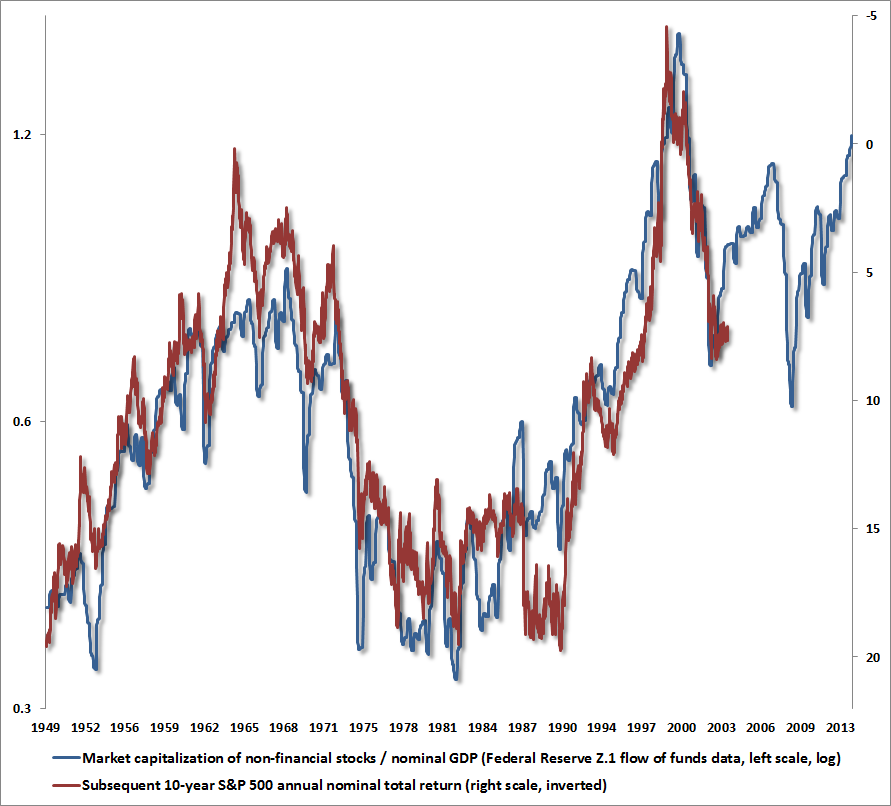

ME: Well, we only need to look at a couple of charts to understand. First, is the total value of the stock market relative to the economy, which just so happens to be Warren Buffett’s favorite valuation yardstick:

via John Hussman

via John Hussman

ME: Stocks have only been more highly valued than they are today at one point during the past 60+ years and that was at the height of the internet bubble. In the words of Mr. Buffett, at this point investors are, “playing with fire.”

II: Still, just because stocks are overvalued doesn’t mean they will fall.

ME: Of course not, they could just trade sideways while earnings grow. In fact, the chart above suggests that is exactly what should happen over the next decade: stocks are priced to return 0% over that time (right scale). This is a great visual representation of, “the price you pay determines your rate of return.” Clearly, the chart shows how accurate this valuation measure (blue line) has been at predicting the coming decade’s returns (red line).

II: That’s still different than saying stocks will go down so why do you say think there is significant downside for stocks?

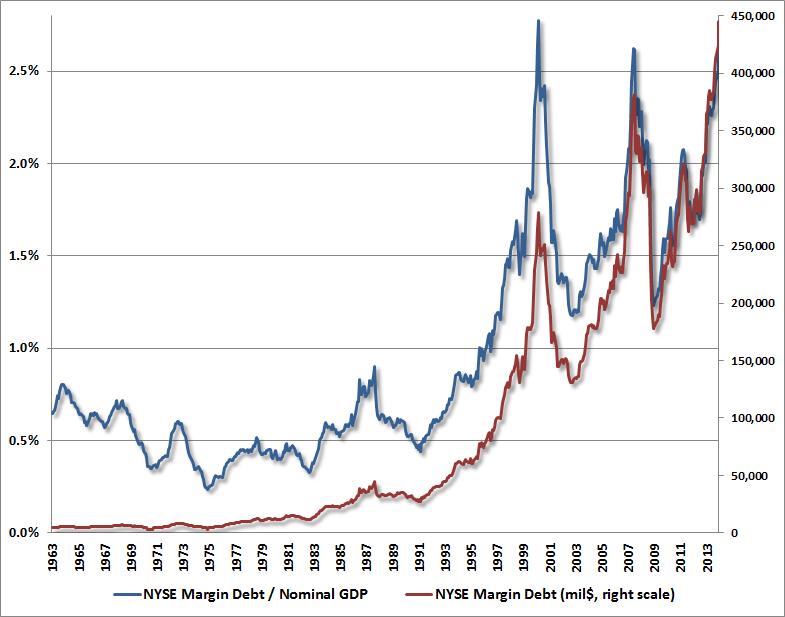

ME: There’s a lot of time between now and 2024; a lot can happen in that span. And another chart suggests a lot could happen. Below is the total level of margin debt and how it also relates to GDP:

via John Hussman

via John Hussman

ME: Never before have so many stocks been purchased with borrowed money. Relative to GDP, again only one period has surpassed the current level and that was at the height of the internet bubble.

II: So?

ME: What’s troublesome about this metric is that the stock market, like all markets, is moved by basic supply and demand. Investors borrowing money to buy stocks amounts to massive demand that pushed prices higher, as we saw last year. On the flip side, however, when these investors decide (or are forced by margin calls) to sell, this massive demand all of a sudden becomes massive supply. This is why each time margin debt has surged like it has recently, stocks have lost at least one-third of their value over the next couple of years.

II: That doesn’t sound good.

ME: Right. Unless you are itching to lock in a zero-percent rate of return over the next decade, it’s probably best to wait until valuations allow for better prospective returns.

II: What valuation level is that?

ME: According to Buffett, it’s about 30-40% below current prices (70-80% of GDP versus 120% today).

II: Wait, that’s just about the same amount that you said stocks typically fall after margin debt surges like it has recently.

ME: UmmHmm.

II: How far have stocks fallen so far?

ME: 5%.