Clearly, this is one of those times individual investors think it’s okay to get back into the stock market. Hell, they’ve poured a massive amount of money into equity mutual funds lately, the most since 2000. It’s just another example of investors buying high (after selling low at the depths of the financial crisis). And it’s exactly why I started this blog back in 2005.

Back then the real estate bubble was nearing its zenith and everybody and their mom (literally) was getting levered to the real estate boom. Not only that they were bragging about it. Today, it’s easy to see how asinine it was but at the time it seemed to a whole lot of people like the right thing to do. So I took it upon myself to warn them that their stupidity would have a serious financial cost. Not only did I send up the warning flag here, I also published a couple of editorials that the local paper reluctantly ran (real estate ads were HUGE business for them). I don’t know if I actually helped anyone but at least I tried.

Today, I’m writing bearish articles about the stock market because once again investors are giddy about getting in on the fun and I don’t think they have any real clue about what a reasonable expected rate of return should be from today’s prices. To the first point, I asked Jason Goepfert of SentimenTrader yesterday to put in perspective for me the current level of bullishness. A couple of days ago I pointed out that the Rydex Bull/Bear ratio currently stands at 8.7 but I wondered, ‘how does this compare to the 2000 and 2007 peaks?’ Jason responded:

@jessefelder @keith_dubauskas 8.7 a/o yesterday, 8.3 in '00, only 2.1 in '07.

— Jason Goepfert (@sentimentrader) November 6, 2013

So the current reading is higher than that seen at the 2000 peak and FAR higher than that seen at the 2007 peak. In this sense, you could say investors are more bullish than ever. Another way of saying it, is ‘investors are greedier than ever’ and you know what Mr. Buffett has to say about greed.

To the second point regarding future returns, I’m pretty confident individual investors have no clue what to expect. They’re taught that, ‘stocks typically go up 8-10% a year and this year has been more like 25% so let’s hop on board, baby!’ What they don’t get is that your future returns are based on the price you pay. After a gain of 160% over the past 5 years stocks have now risen to valuations that make it nearly impossible for them to deliver on this 8-10% promise.

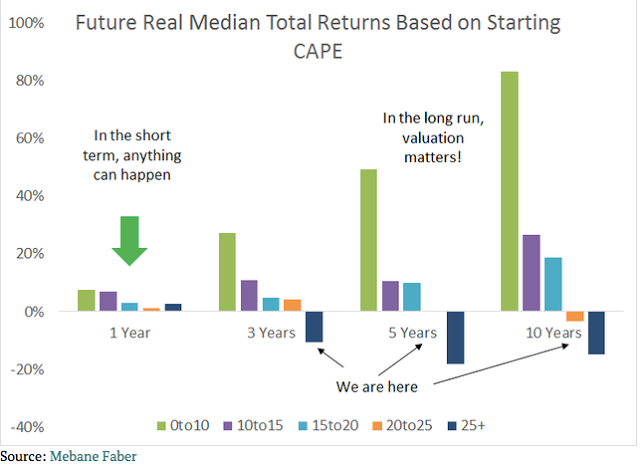

Based on Doug Short’s excellent valuation models stocks are anywhere from 45-85% overvalued. This means that earnings have to increase by this amount simply to have a good chance at break even. And if that doesn’t happen then they could easily fall 30-40% (or worse as bear markets typically overshoot on the downside) just in the process of reverting to mean/getting back to fair value. The following graphic (courtesy of @ukarlewitz) explains it perfectly. When you overpay for stocks, you are virtually guaranteed to lose money (in real terms) over the long term:

So, please don’t buy anymore stocks right now. I know it probably feels right but basic math says you’re wrong. Follow Warren Buffett’s lead and be fearful while everyone and their mom gets greedy. You’re welcome.

So, please don’t buy anymore stocks right now. I know it probably feels right but basic math says you’re wrong. Follow Warren Buffett’s lead and be fearful while everyone and their mom gets greedy. You’re welcome.

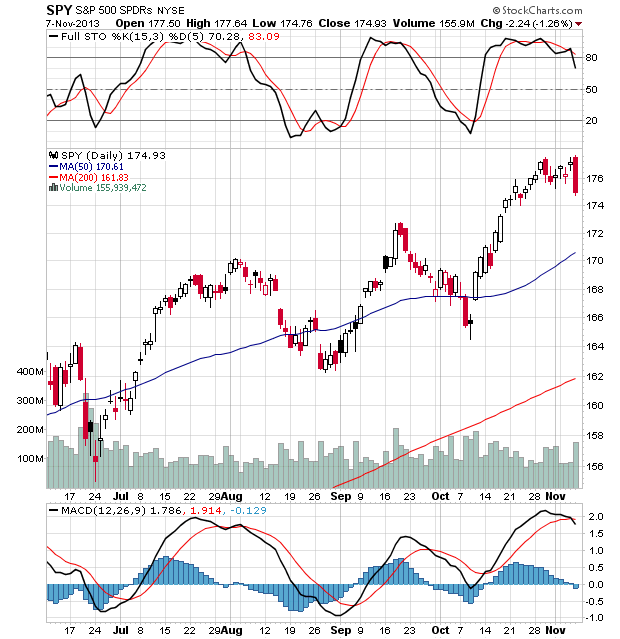

Chart of the Day:

The S&P 500 climbed to another new all-time high this morning before reversing and closing lower than yesterday’s low (in fact, all of the previous week’s lows). This is a classic “outside reversal” or “bearish engulfing” pattern.