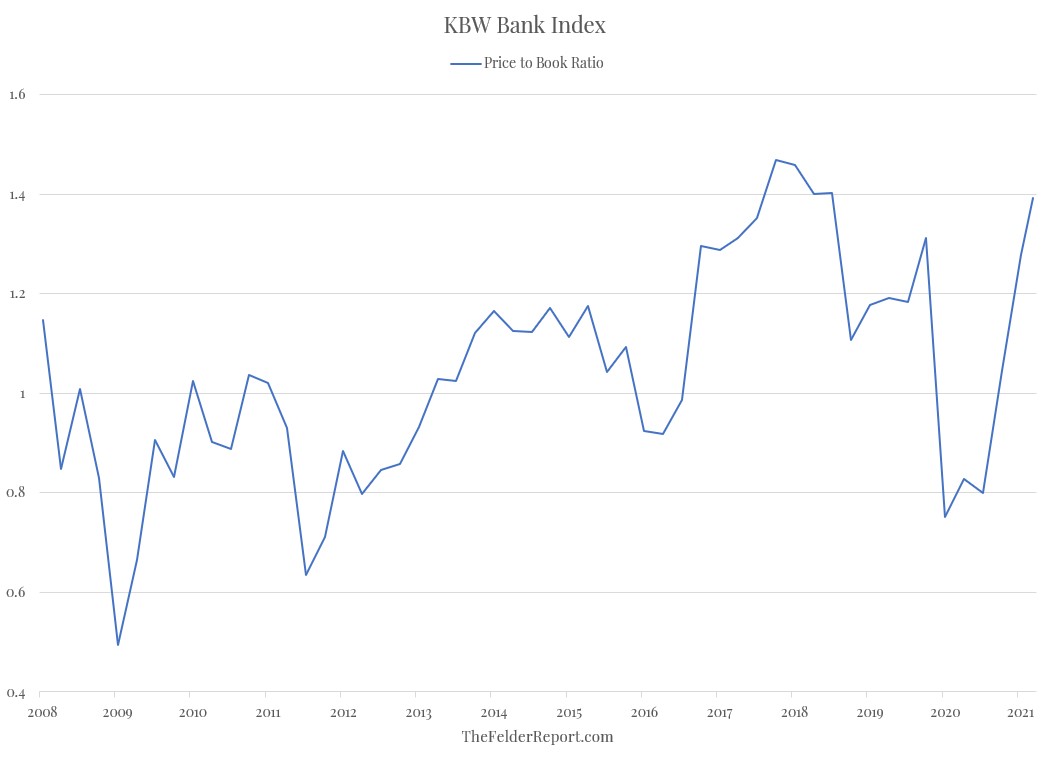

Back in October I suggested investors had probably gotten too bearish on the banks. Since then these boring, old, nocoiner institutions have dramatically outperformed the broader stock market. Hell, Wells Fargo has more than doubled in price over just the past seven months. But, as a group, these stocks can no longer be considered cheap.

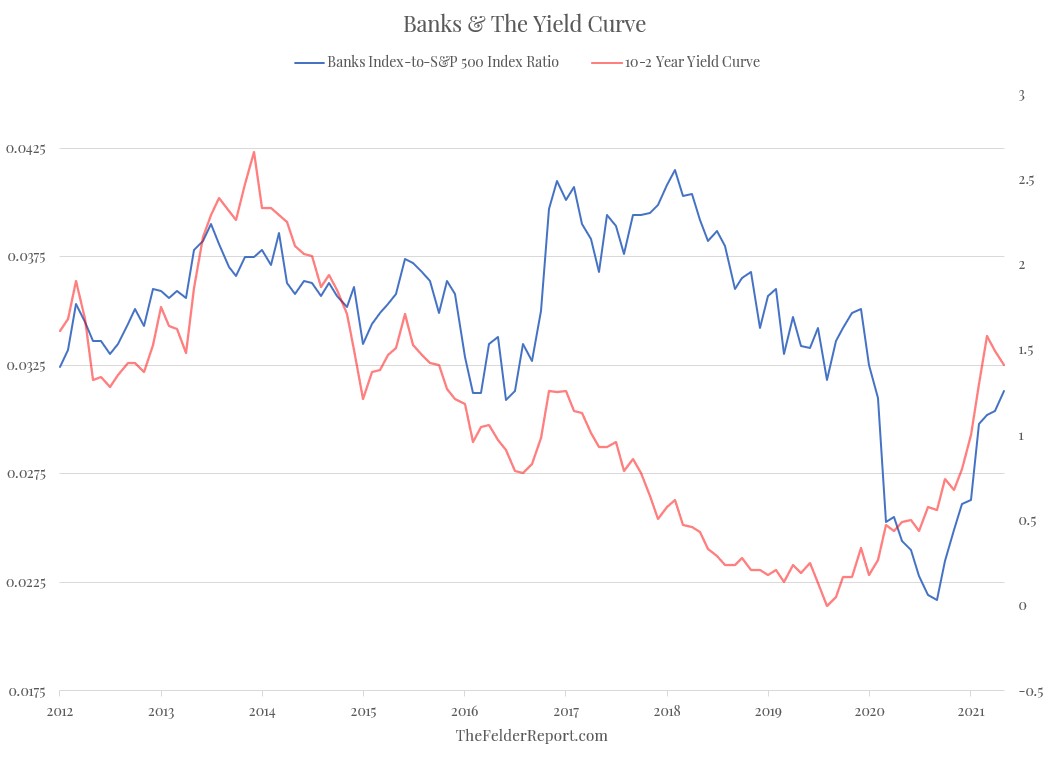

Furthermore, the best indicator of the trend in their relative performance, the yield curve, recently stopped running higher and has now reversed to the downside. In other words, the primary tailwind for the banks (and their net interest margins) is now potentially becoming a headwind.

And with the short end of the yield curve at the zero lower bound, it would take a further rise in long-term yields to power the yield curve higher from this point. However, 2.5% looks like important horizontal technical resistance for the 30-year yield which may prove quite challenging to overcome.

In all, it’s hard to say the banks offer anywhere near the absolute and relative value they did back in the fall. And if the Fed is forced to start raising interest rates sooner rather than later, as some seem to believe, then there’s a good chance the recent reversal in the yield curve could accelerate to the downside which would be a truly bearish development for the banks.