Jesse Livermore said, “History repeats itself all the time in Wall Street.” Well, it certainly looks like there is a decent chance we are now repeating the 1937 episode Ray Dalio recounted a while back. The similarities are simply stunning. Below are a few unedited excerpts from his piece. The only change I made was to replace his charts tracking the 1937 experience with ones that plot our recent experience.

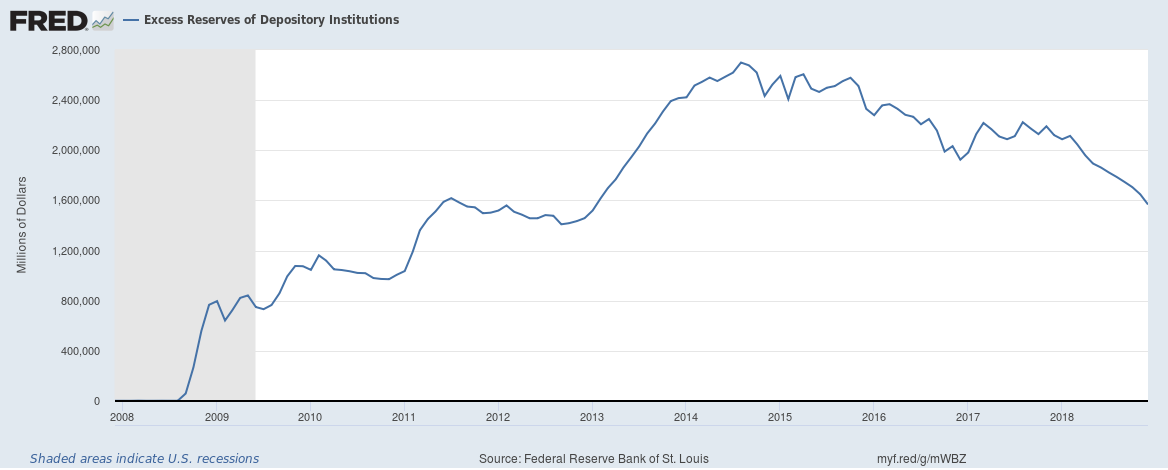

After the first tightening in August 1936, there was one in March 1937 and another one in May 1937… As a result of reserve tightening, excess reserves fell in the manner shown in the chart below.

The economy remained strong into early 1937. The stock market was still rising, industrial production remained strong, and inflation had ticked up to around 5%. The second tightening came in March of 1937 and the third one came in May…. The tighter money and reduced liquidity led to a selloff in bonds, a rise in the short rate, and a selloff in stocks.

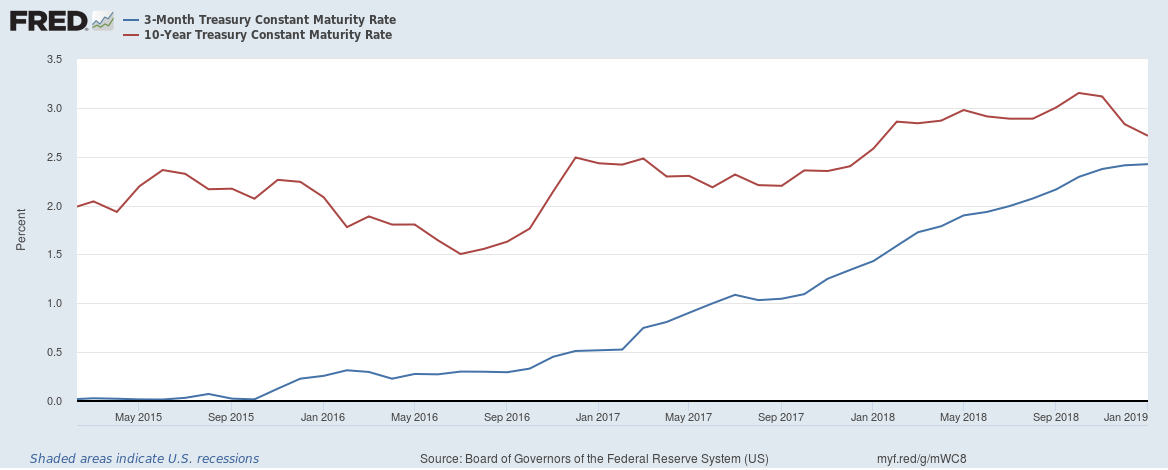

Following the second increase in reserves in March 1937, both the short term rate and the bond yield spiked (see below).

Stocks also fell that month nearly 10%. They bottomed a year later, in March of 1938, declining more than 50%.

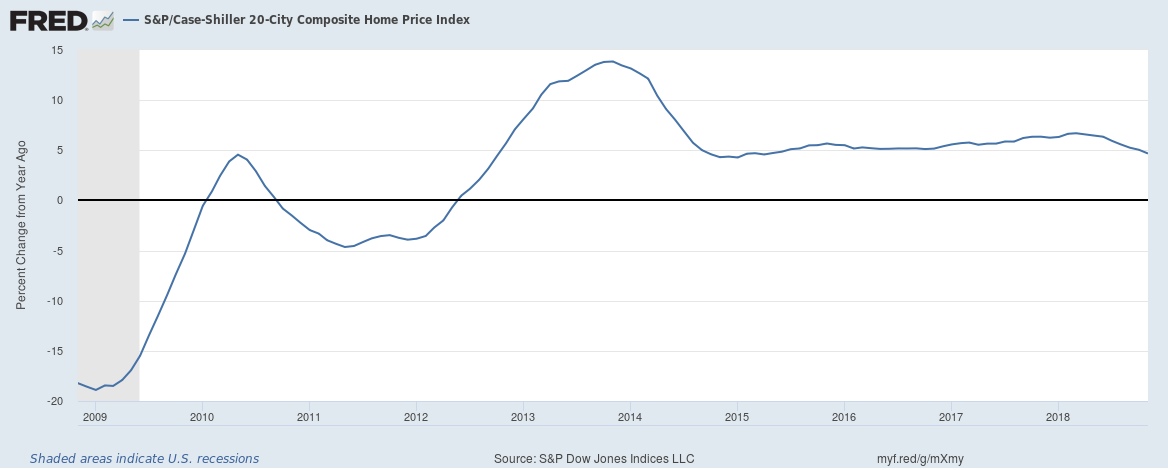

Stocks fell the most but home prices arrested their gains and dipped negative, as well.

The decline in asset prices and wealth kicked off a self-reinforcing downward cycle, in which the decline in the stock market led to a weakening of the economy that reduced earnings, which contributed to further stock weakness.

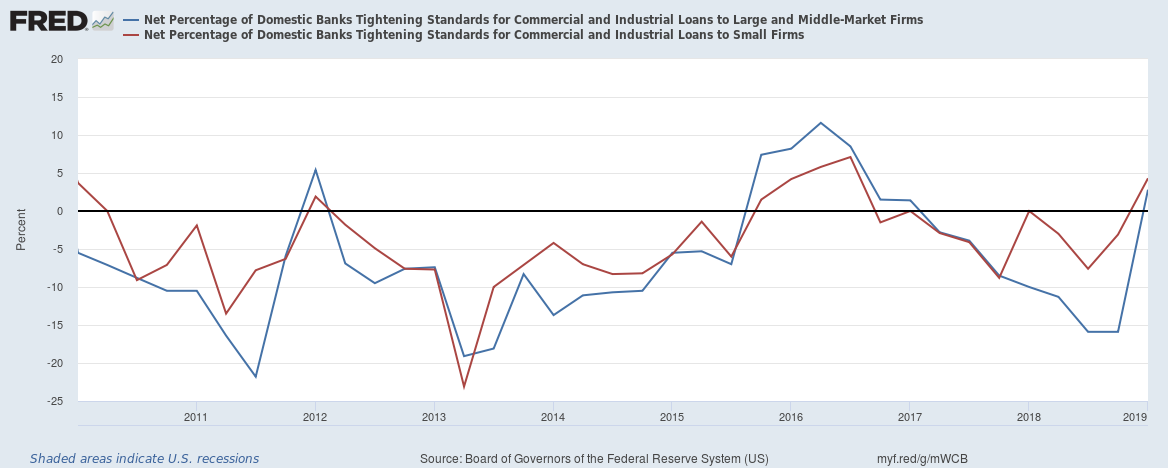

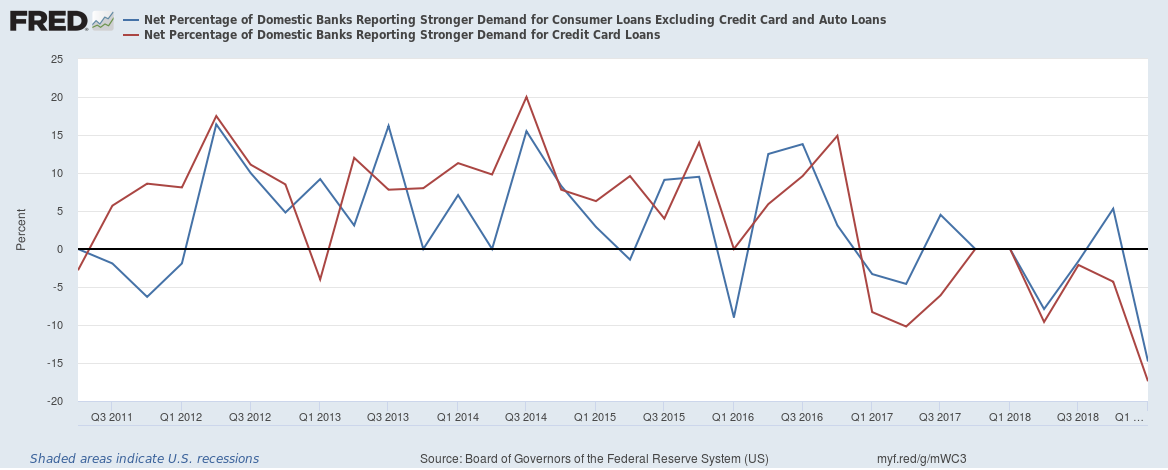

As a result, credit growth slowed as well, both in aggregate and across all sectors.

…and spending and economic activity fell.

So maybe it wasn’t just the stock market selloff late last year that inspired the dovish flip flop on the part of Jay Powell & Co. It could have been just a bad case of deja vu.