Last week the Wall Street Journal reported:

After a long hiatus, George Soros has returned to trading, lured by opportunities to profit from what he sees as coming economic troubles. Worried about the outlook for the global economy and concerned that large market shifts may be at hand, the billionaire hedge-fund founder and philanthropist recently directed a series of big, bearish investments, according to people close to the matter.

Since then there’s been much debate about the veracity of this story. ‘Is George really bearish?’ seems to be the question most are asking right now and, more importantly, ‘why?’

If you have paid any attention at all to what his former lead portfolio manager, Stan Druckenmiller, has been saying recently, it should be fairly obvious. Here’s Druck from last year:

80% of the big, big money we made was in bear markets and equities because crazy things were going on in response to what I would call central bank mistakes during that 30-year period.

And here’s what he had to say more recently:

By most objective measures, we are deep into the longest period ever of excessively easy monetary policies.

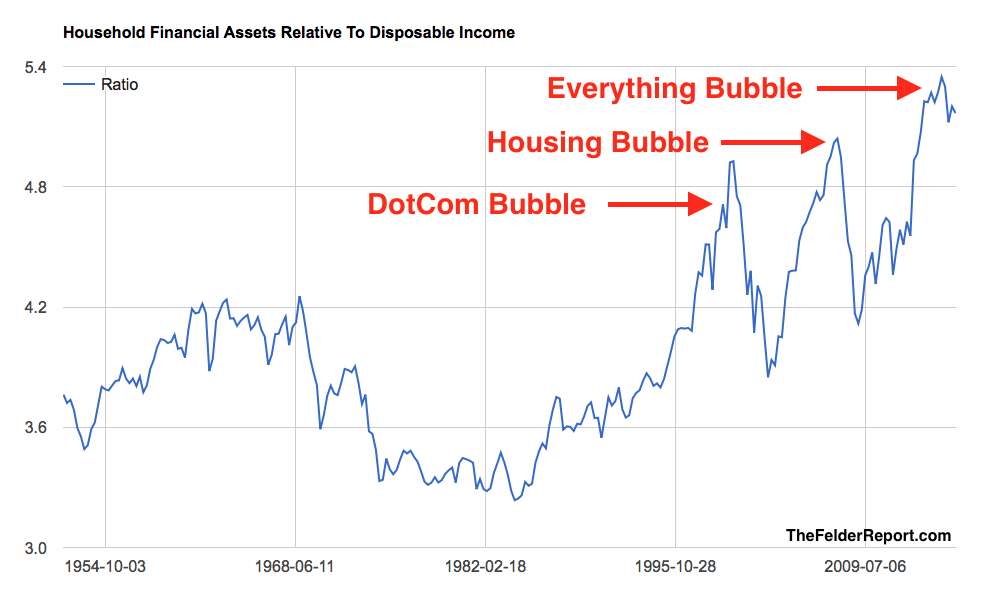

In other words, he believes that the central bank has now made what could be the single greatest mistake in its history. 7 years of ZIRP (zero percent interest rate policy) have led investors to do “crazy things” yet again, like push the valuations of stocks, bonds and all sorts of other asset classes to rare extremes.

During their immensely profitable partnership Soros and Druck found no greater source of profit than taking advantage of just these sort of central bank “mistakes” by putting on “big, bearish investments” that paid off handsomely during the inevitable busts that followed.

They have not made any secret about this. In fact, I find it fascinating that they (along with others like Carl Icahn) are more public than ever about their concerns and, rather than heed their warnings, investors broadly insist on disparaging or simply ignoring them – even when they are validated by long-time Fed insiders.