My recent piece, “The New Wolves Of Wall Street,” struck a nerve. I think it taps into both advisers’ insecurities and investors’ worries about not getting what they pay for. Good. That’s what I was going for.

Before I follow up on that piece, though, let me make a couple of things clear. First, there are some truly wonderful advisers out there. My experience, however, tells me they are more the exception than the rule. As WSJ’s Jason Zweig tweeted this morning many, “treat clients like Sioux treated the buffalo.”

Second, I’m not criticizing either the RIA model or index funds right now (though these aren’t without their own problems). All in all, they are a net positive for individual investors because they reduce conflicts of interest and bring down costs. I’m focused on the problems that arise when you put the two together.

"The investment-management business is insane." -Charlie Munger http://t.co/7m6CSbGGym via @jasonzweig

— Jesse Felder (@jessefelder) September 12, 2014

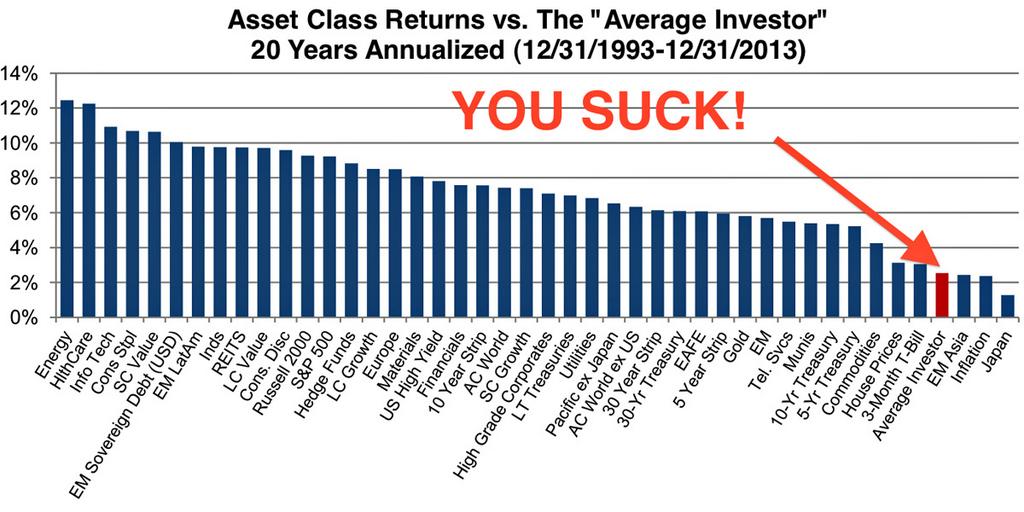

Ultimately, this discussion is focused on the massive underperformance individual investors experience in their own portfolios on a consistent basis:

Most pundits like to blame this on the fact that individual investors are just “dumb money.” Indeed, there is a “behavior gap” that causes investors to become euphoric with the crowd and buy at the wrong time and then panic in the midst of a bear market and sell at precisely the wrong time. This is human nature.

What the wolf doesn’t want you to know, however, is that he’s just as much to blame for your underperformance as your caveman brain is (see “Where’s Wall Street’s Blame In The Buy High Sell Low Game?“). In fact, even if he does a perfect job managing your natural instincts along with his own, he’s going to cost you big time – like half of all of your profits over the long run, big time.

So the problem as I see it two-fold. Both the “behavior gap” and obscene fees are significant contributors to the problem of massive underperformance. Addressing the first part is a good start. But ignoring the second part or – even worse – pretending, as an adviser, to pursue a low-cost approach while charging predatory fees is counterproductive, at best.

In fact, I’ll take it a step further. An adviser who is recommending passive index funds should not charge a “management fee” at all. Management fees are just that – fees for managing investments. If you’re not managing investments – you’re just overseeing a passive portfolio – you don’t deserve a management fee. Period.

Investment advice like this is valuable, though. Investors deserve to be educated about how their biases screw up their investment plans. And I think there’s a huge opportunity for advisers interested in doing this the right way.

Investment advice like this should be compensated just like all the other “advice” given by professionals out there – attorneys, accountants, therapists, etc. – on an hourly rate. Get paid for the advice you’re giving. Nothing more – nothing less. What would you say to your CPA if, instead of his hourly rate, he asked you for 2% of all your money every year for the rest of your life just for doing your taxes?

Too many “advisers” simply gather assets, charge their management fee for a one-time recommendation and then just ride the gravy train. And can you blame them? Under a management fee structure this is the overwhelming financial incentive. They maximize their profits by bringing in as much money as possible to charge a perpetual management fee on and then do as little management or advising as possible.

If advisers were compensated for the time they spent actually advising rather than the amount of assets they gathered then that’s how they would spend their time. This would much better align investor needs with adviser incentives. And it would also help keep human advisers relevant in the era of the robo-adviser. Somebody’s going to see the light here and seize this opportunity, I’m sure.

Still, I believe that the vast majority of investors are capable of overcoming the “behavior gap” on their own. They certainly don’t need pay an annual tithe to have it managed for them. My hope is that this helps inspire them to help themselves. And there are some wonderful role models out there like Stephanie Mucha.