I continue to be amazed at the rampant rationalizing that is fueling this market. In my first “Mania” post, I began with a quote from professor Shiller regarding his CAPE ratio and what it currently suggests about stock market valuation:

“The United States stock market looks very expensive right now. The CAPE ratio, a stock-price measure I helped develop — is hovering at a worrisome level…. above 25, a level that has been surpassed since 1881 in only three previous periods: the years clustered around 1929, 1999 and 2007. Major market drops followed those peaks.” -Robert J. Shiller, Nobel Prize-Winning Economist and Author of “Irrational Exuberance”

Impersonating the rationalizers I mimicked the popular response: “the CAPE ratio is flawed and valuations don’t matter anyway; stocks are only worth what someone else is willing to pay.”

Lo and behold, somebody stepped up to the plate and took the rationalization to a whole new level (via CNBC):

[Charles] Dumas argues that including the Great Depression, two world wars and the Cold War into the long-run average makes it an “unduly poor comparator”. Instead, if you disregard this period, the CAPE is only 7 percent above the post-Cold War average, according to Dumas.

In other words, ‘if we take out all the bad stuff (decades and decades of market history) and focus only on the good times, the market is only 7% overvalued – AND that’s somehow bullish.’ How can this guy say this with a straight face? The whole purpose of the CAPE ratio is to adjust for cycles; it’s an acronym for “cyclically-adjusted price-to-earnings” ratio. Is he really suggesting we throw out professor Shiller’s Nobel Prize-winning work and only use a BLPE, “bubble-level price-to-earnings” ratio?

The article continues by quoting his cohort, Jack Boroudjian who writes the CAPE off as a, “strange equation.” I would literally pay money to hear these guys rationalize Buffett’s favorite yardstick right now. It’s incredibly entertaining.

Also, just off hand in my earlier piece, I mentioned the ad hominem attacks directed at John Hussman. Well Larry Swedroe subsequently jumped the shark in this regard (via ETF.com):

One investor recently asked me to comment on Hussman’s latest musings, which had made him quite nervous. Now, I knew that Hussman had been persistently bearish for quite some time, and I have been asked about his columns fairly frequently. So I went back into my files and dug up what I had written about his comments on the market from Jan. 14, 2013. It provides a great example of why he should be ignored, along with all other forecasters.

A reader asked you to comment on his “latest musings” so rather than read his “latest musings,” Larry, you went back 18 months and roughly 75 weekly reports ago. Ignore the argument put to you and resort to “genetic fallacy” to prove he’s an idiot: ‘he was wrong 18 months ago so he must be wrong today,’ is not logic. It’s simply avoiding the issue and it only makes you look like an idiot, Larry.

He continues:

As further evidence of why you should ignore market forecasts like Hussman’s, consider the following performance data on his flagship fund, Hussman Strategic Growth (HSGFX). As of Aug. 4, 2014, the fund had $1.1 billion in assets—less than 40 percent of what it had just 19 months earlier—as investors fled, unhappy with the poor performance.

Please take a quick peek at Wikipedia’s definition of “genetic fallacy,” Larry. Your argument clearly, “fails to assess the claim on its merit,” and relies solely on, “something or someone’s origin rather than its current meaning or context.” Oh, and also the bandwagon fallacy: ‘if people are bailing out of his fund he must be an idiot because mutual fund investors are always brilliant traders!’

If you take the time to actually read Hussman’s “latest musings” you’ll find he’s not making 1-year forecasts, as Larry would have us believe. He’s making 10-year forecasts, something even Warren Buffett does regularly to assess the future prospects of owning stocks. And Hussman uses indicators like Buffett’s favorite valuation yardstick which are very highly correlated to future 10-year returns.

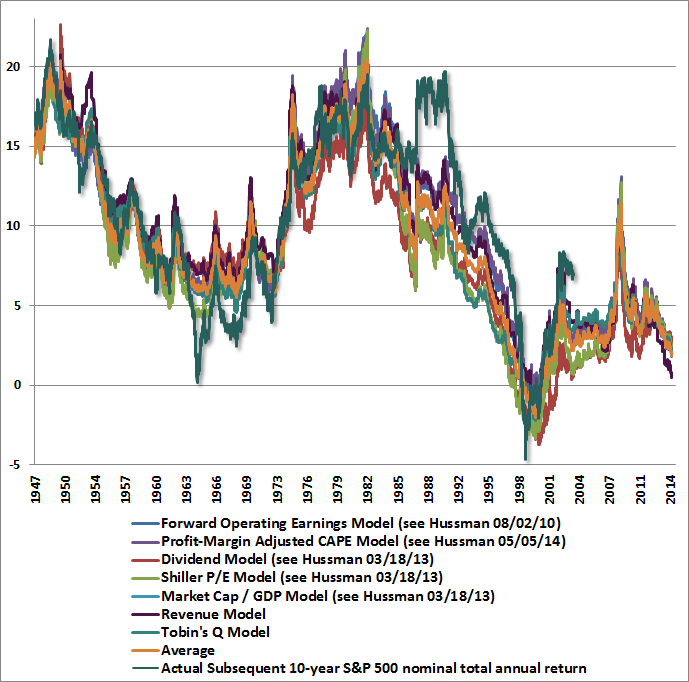

I urge you to actually take a look at some of his “latest musings” and see what his indicators are saying right now:

As the chart above clearly indicates a multitude of independent indicators (including Shiller’s CAPE and Buffett’s favorite yardstick, market cap-to-GDP), all of which are highly correlated to future returns, suggest that owning stocks over the next decade will yield close to zero annual return, one of the worst prospects in history – this based on simple math and statistics supported by nearly 80 years of data.

So rationalize it however you like. Or simply ignore it. That’s your prerogative. Just know this type of mental gymnastics only happens in the midst of a mania. And it’s just fascinating to witness.