It was just about a year ago I wrote “Mr. Market Is Not Impressed With Apple (And Why He’s Wrong).” It was probably the most popular post I’ve ever written (thanks in large part to @gruber). It was the day after the company’s first quarter earnings announcement and the stock had fallen 12% to close at $450 per share. Today, after a very similar reaction by investors to the company’s results the stock fell 8% to $506 per share.

It was the company’s “disappointing” iPhone sales that investors are blaming for the selloff. Apple sold 51 million in the holiday quarter and analysts had expected that number to be about 10% higher. Now we can nitpick all we want about certain goals Wall Street sets for the company but the fact of the matter is this is a company that has revolutionized consumer tech products. The iPhone and iPad have become the gold standard and millions and millions of people around the world now feel they just can’t live without them.

"Apple can't innovate."

Motherf***er you're watching a movie on a 4 ounce plate of glass.

— Downtown Josh Brown (@ReformedBroker) January 28, 2014

Oh, and Apple makes a tidy profit at this, as well. Over the last 12 months the company has generated $53 billion in cash flow and has grown the total hoard to nearly $160 billion – a truly unfathomable number. Using various valuation methodologies (discounted cash flow – assuming it grows only at the rate of inflation, the company’s historical valuation lows, and the average valuation of its 3 nearest competitors: Google, HP and Microsoft) I come up with a fair value for the stock somewhere in the $800-$900 range.

Just bought $500 mln more $AAPL shares. My buying seems to be going neck-and-neck with Apple's buyback program, but hope they win that race.

— Carl Icahn (@Carl_C_Icahn) January 28, 2014

Maybe this is why Carl Icahn has been buying with both hands lately. But this is only a small part of the story…

Wall Street can be a wacky place. This is why Ben Graham came up with his now famous “Mr. Market” analogy (read it here). Mr. Market doesn’t always price things correctly. In fact, he regularly suffers from too much optimism or too much pessimism usually as a result of projecting recent history out into the future rather than looking at the big picture

A couple of years ago, Apple could do no wrong and Mr. Market regarded nearly every announcement from the company as a buying opportunity. Flash forward to today and the company can do nothing right. Nearly every announcement, related to earnings or products, etc., is regarded as a disappointment and is sold – despite the fact that the company is insanely profitable, respected by critics and loved by consumers.

It’s amazing how quickly Mr. Market’s attitude toward the company has changed. Wired wrote about this today in a piece titled, “Why Nothing Apple Does Is Ever Good Enough.” All I could think while reading it was ‘if Mr. Market’s blind optimism about the stock at $700 18 months ago was a contrarian sell signal then this has to be a terrific contrarian buy signal.’

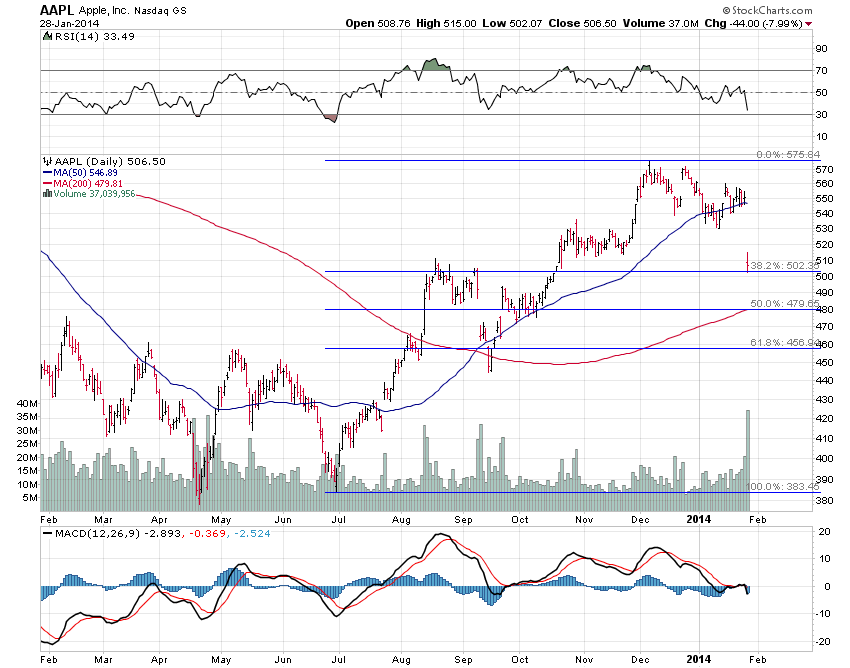

Taking a look at the charts, technically this pullback in the stock looks fairly routine. Today it found support right at the 38.2% Fibonacci retracement level and is now entering oversold territory (see RSI at the top of the chart):

It may very well pull back all the way to the 61.8% level around $456 but I would still consider that “healthy” or “normal.”

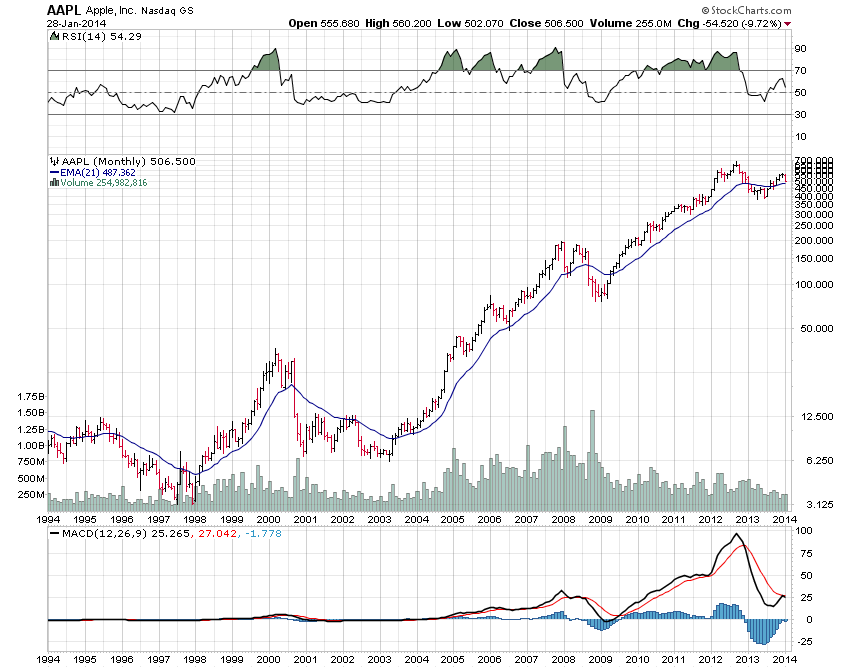

On a much longer time frame, the stock is still above its 21-month moving average (which sits at $487) and MACD lines are getting very close to crossing higher which I would consider a very bullish development:

What it may take to get the stock going is a new product category. The iPad was introduced 4 years ago and the company hasn’t really announced anything new since then. Sure there have been rumors of an iWatch or a television but the company hasn’t made anything official.

Bottom line: Apple needs a new product. Growth with current line up is done.

— Jay Yarow (@jyarow) January 27, 2014

However, Tim Cook did say yesterday that they intend to change all that this year and finally introduce new products. And if they come up with anything that is even fractionally as successful as the iPad or iPhone, the stock will be seen as a growth co. once again. At that point, 5 times EV-to-EBITDA will look like a bargain in the eyes of Mr. Market once again. And investors not plagued by his current myopic condition will stand to benefit greatly.