Back in December, I wrote, “Considering the fact that the majority of investors are still betting on a transitory outcome, there could be some fireworks in the asset markets should they eventually be forced into an inflationary epiphany. Furthermore, what may exacerbate those fireworks, particularly in the stock market, is an earnings recession amid the most extreme valuations in history.” And that actually sounds like a pretty fair assessment of 2022 so far even though these trends continue to unfold.

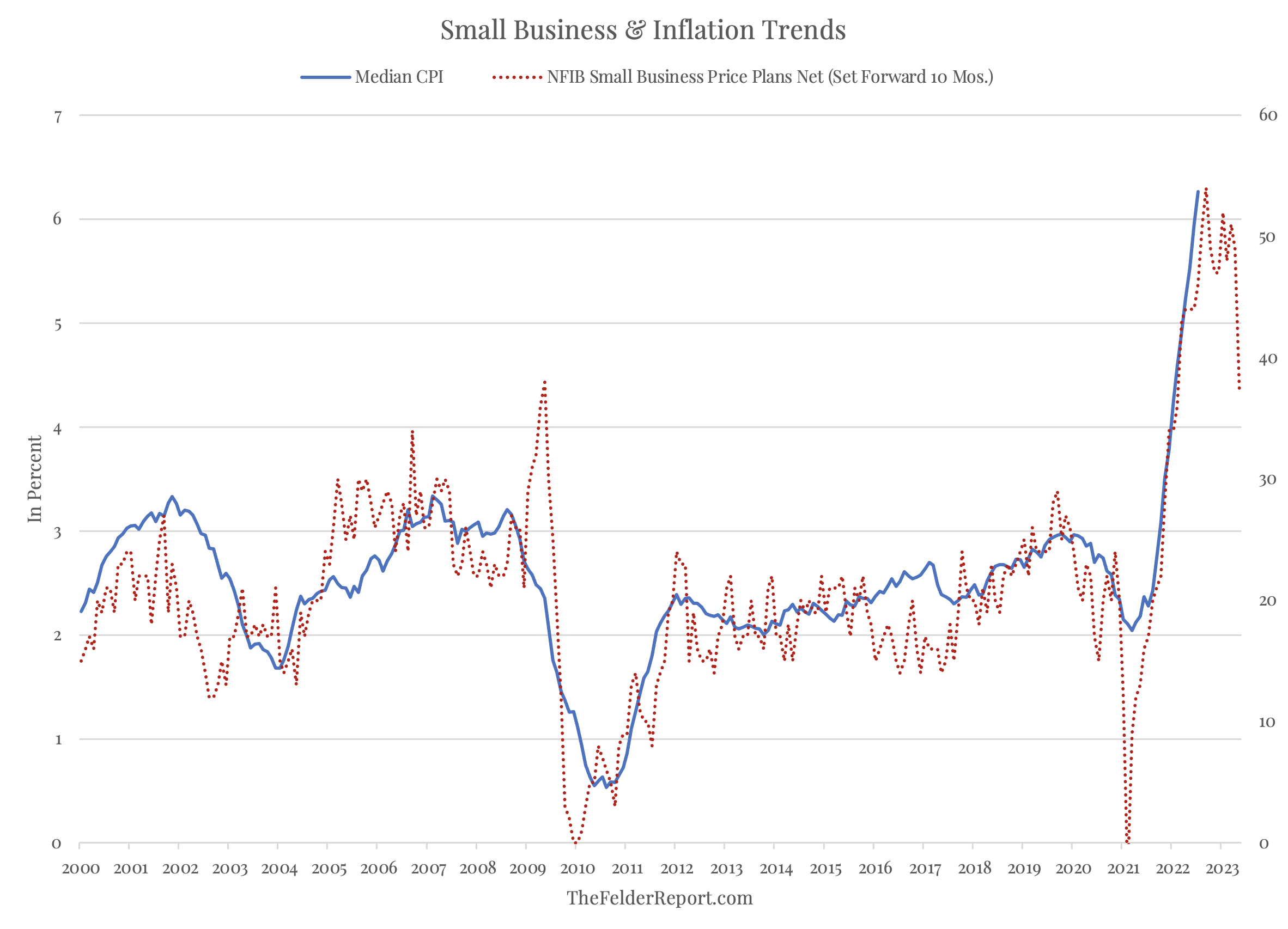

The data that led me to the conclusion that inflation would surprise on the upside and corporate earnings would surprise on the downside this year was provided by the NFIB survey of Small Business Economic Trends. Back in December, the number of business owners planning on raising prices had been soaring for some time, indicating inflation would follow. That indicator peaked a while back, suggesting inflation could plateau or over reverse to some degree which we began to see in the July CPI report released today.

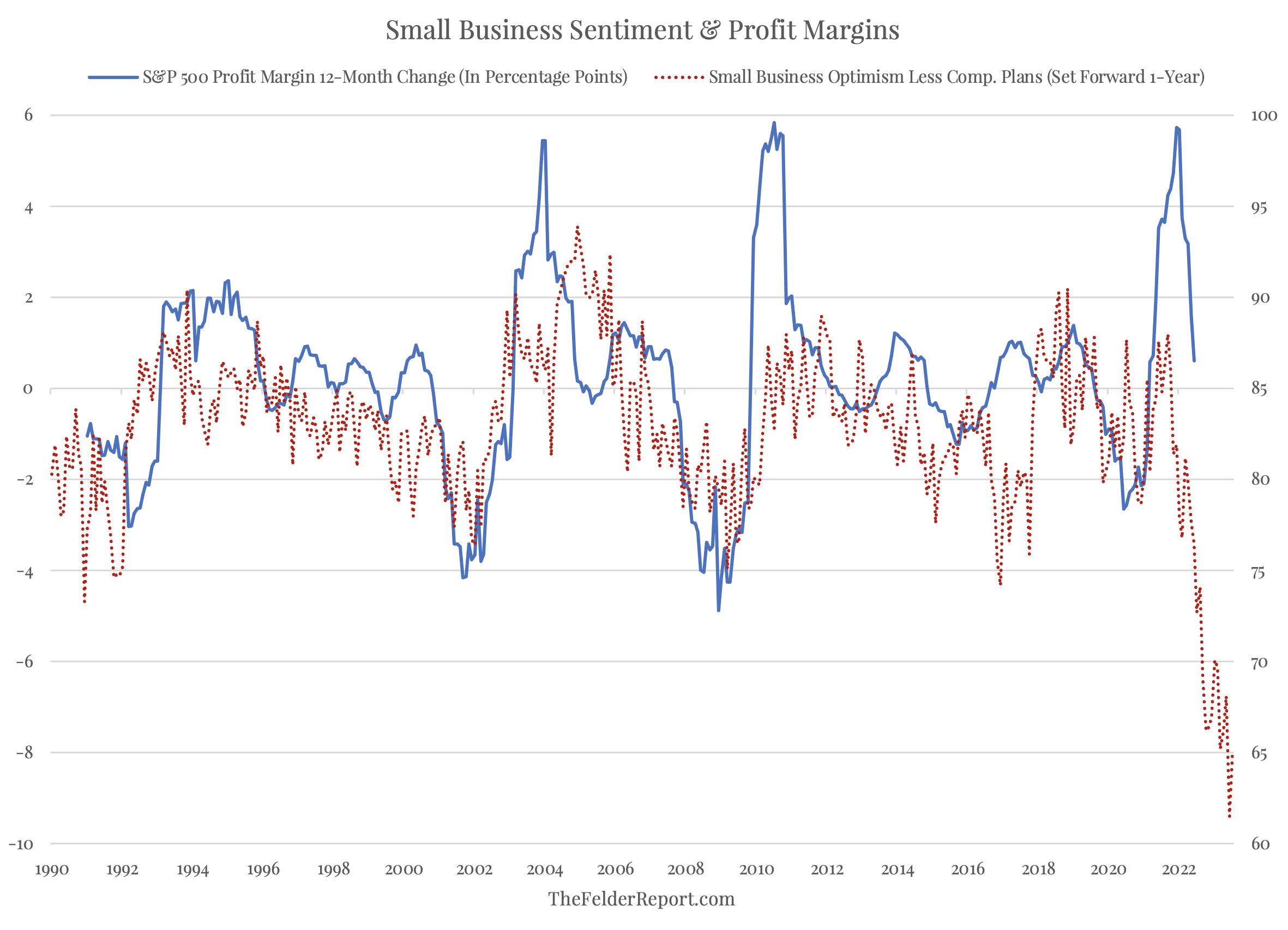

What may be precipitating this relative moderation in price pressures, however, is a slowdown in demand as indicated by falling optimism (and sales expectations) in the survey. At the same time, compensation plans remain elevated due to a persistently tight labor market. The result is that the recent reversal in the growth of profit margins is likely only getting started. In fact, this indicator suggests the decline in corporate profitability as a result of stagflationary pressures over the next few quarters could be historically deep.

So while equity investors may be correct in their assessment of the cyclical trend in inflation, they may not want to celebrate it in such ebullient fashion. Because any moderation in inflationary pressures is unlikely to be driven by the sort of benign economic factors that would support equity prices. On the contrary, the risk of the current slowdown in the economy, which has enabled inflationary pressures to abate even to a small degree, evolving into a full-blown recession ahead appears significant.