I recently came across another cluster of insider selling that looked intriguing. Many of the top executives at Peleton, including the President, CFO and Head of Product Development, just unloaded a sizable chunk of stock. In total, they have sold over $88 million in stock since May, with over $60 million of that coming just in the month of September. What’s more, in many cases these sales represent their entire stake in the company (not including unexercised options).

| Trade Date | Name | Title | Price | Shares | Owned | Change | Value |

|

9/17/20

|

Draft Howard C. | Dir | $83.06 | -20,000 | 324,586 | -6% | -$1,661,264.00 |

|

9/14/20

|

Kushi Hisao | GC | $80.83 | -132,890 | 1,724 | -99% | -$10,742,117.00 |

|

9/14/20

|

Lynch William | Pres | $80.88 | -313,500 | 0 | -100% | -$25,355,692.00 |

|

9/14/20

|

Cortese Thomas | COO | $80.83 | -300,000 | 413 | -100% | -$24,249,660.00 |

|

9/3/20

|

Garavaglia Mariana | CBOO | $83.18 | -5,209 | 1,101 | -83% | -$433,276.00 |

|

7/1/20

|

Woodworth Jill | CFO | $60.02 | -49,900 | 0 | -100% | -$2,995,203.00 |

|

6/26/20

|

Woodworth Jill | CFO | $60.00 | -100 | 0 | -100% | -$6,000.00 |

|

6/22/20

|

Woodworth Jill | CFO | $55.00 | -45,000 | 0 | -100% | -$2,475,000.00 |

|

6/15/20

|

Woodworth Jill | CFO | $50.07 | -40,000 | 0 | -100% | -$2,002,788.00 |

|

5/12/20

|

Lynch William | Pres | $45.36 | -147,132 | 1,724 | -99% | -$6,674,346.00 |

|

5/12/20

|

Woodworth Jill | CFO | $45.24 | -35,000 | 0 | -100% | -$1,583,229.00 |

|

5/8/20

|

Woodworth Jill | CFO | $42.46 | -130,000 | 0 | -100% | -$5,520,229.00 |

|

5/7/20

|

Lynch William | Pres | $45.17 | -100,000 | 1,724 | -98% | -$4,516,680.00 |

Data via OpenInsider.com

You may already know Peleton from their many television ads, one of which became a brief internet sensation over the holidays. But since the pandemic hit, Peleton has become popular not just for its main product, which has tapped into the incredible demand for home workout equipment, but for its stock, which has appealed to all those new day traders looking for sardines.

Since the beginning of the year, Peleton’s sales have surged 170% and its stock price has surpassed even that, rising over 250%. This stellar stock price performance has taken its price-to-sales ratio to 11.5, totally unheard of for an exercise equipment company, especially one that has not yet become profitable. However, bulls might argue, the company is not so much an equipment company as it is a SaaS one, the hottest segment of the stock market today.

SaaS, for those unaware, stands for, “software as a service,” and SaaS companies make their money by signing up subscribers for a recurring payment in exchange for some sort of service. In this case, the service is a virtual workout class. So while an exercise fitness company like Nautilus, which has also done very well as a byproduct of the pandemic (with sales rising 93%), trades at a mere 1.3 times sales, Peleton is given a valuation in line with the software sector.

To give you a better understanding of the valuation here, Peleton now carries a market cap of over $27 billion (on $1.8 billion in sales and -$80 billion in EBIT). This puts it ahead of a number of other names, probably even more familiar to you – and certainly more profitable.

| Numbers in millions | Free Cash Flow | |||

| Symbol | Name | Market Cap | Revenue | (Less SBC) |

| PTON | Peloton Interactive Inc | $ 27,483 | $ 1,800 | $ 131 |

| BBY | Best Buy Co Inc | $ 27,441 | $ 43,430 | $ 4,896 |

| PAYX | Paychex Inc | $ 27,383 | $ 4,040 | $ 1,267 |

| TRV | The Travelers Companies Inc | $ 27,218 | $ 31,380 | $ 5,705 |

| YUM | Yum Brands Inc | $ 27,045 | $ 5,494 | $ 972 |

| CLX | Clorox Co | $ 26,880 | $ 6,721 | $ 1,242 |

| F | Ford Motor Co | $ 26,417 | $ 130,400 | $ 9,074 |

| AZO | AutoZone Inc | $ 26,373 | $ 12,630 | $ 1,657 |

| DHI | D.R. Horton Inc | $ 26,005 | $ 18,950 | $ 1,233 |

| KR | The Kroger Co | $ 25,777 | $ 128,900 | $ 3,729 |

So it appears Peleton has some significant growth and profitability goals to live up to. At the current valuation, investors are already pricing in a terrific improvement in the company’s sales and profitability, above what the company has already seen so far in 2020. The question then becomes, how sustainable is the company’s recent growth? And how likely is it the company can increase its profitability?

First, it’s hard to imagine a more bullish scenario for the company than the current pandemic. The vast majority of people are now avoiding crowded public places like gyms and so they look to alternatives they can use at home. It is the perfect environment for a company like Peleton. But what happens when the pandemic is over and gyms open back up and people are tired being stuck at home? Of course, the answer is Peleton’s sales growth drops dramatically and the stock, which is priced for perfection, is also forced to price in an environment that is no longer perfect.

Furthermore, the company was profitable in its fiscal fourth quarter ending June 30 only because it dramatically reduced marketing spend during the quarter. The pandemic is essentially marketing the company’s products for it. So, here too, it’s very difficult to extrapolate that profitability beyond the duration of the pandemic. When it’s gone, how much marketing will Peleton need to do? Of course, the answer is far more than they’re doing now if they want to maintain anything close to their current growth rate.

In contrast to Peleton’s current market reality, I would be inclined to argue that it probably deserves a discounted valuation based on the extraordinary circumstances we find ourselves in today that are temporarily boosting demand. So let’s just be generous and assume the company can make $90 million per quarter (what it made in the fourth) every quarter. That’s $360 million annualized. Let’s also be generous and put a price-to-earnings ratio of 25 on that number. That leaves a $9 billion valuation, or roughly a third of today’s market cap. It’s hard to justify anything more than that in my book and, at the same time, it wouldn’t be surprising to see it fall much further than that.

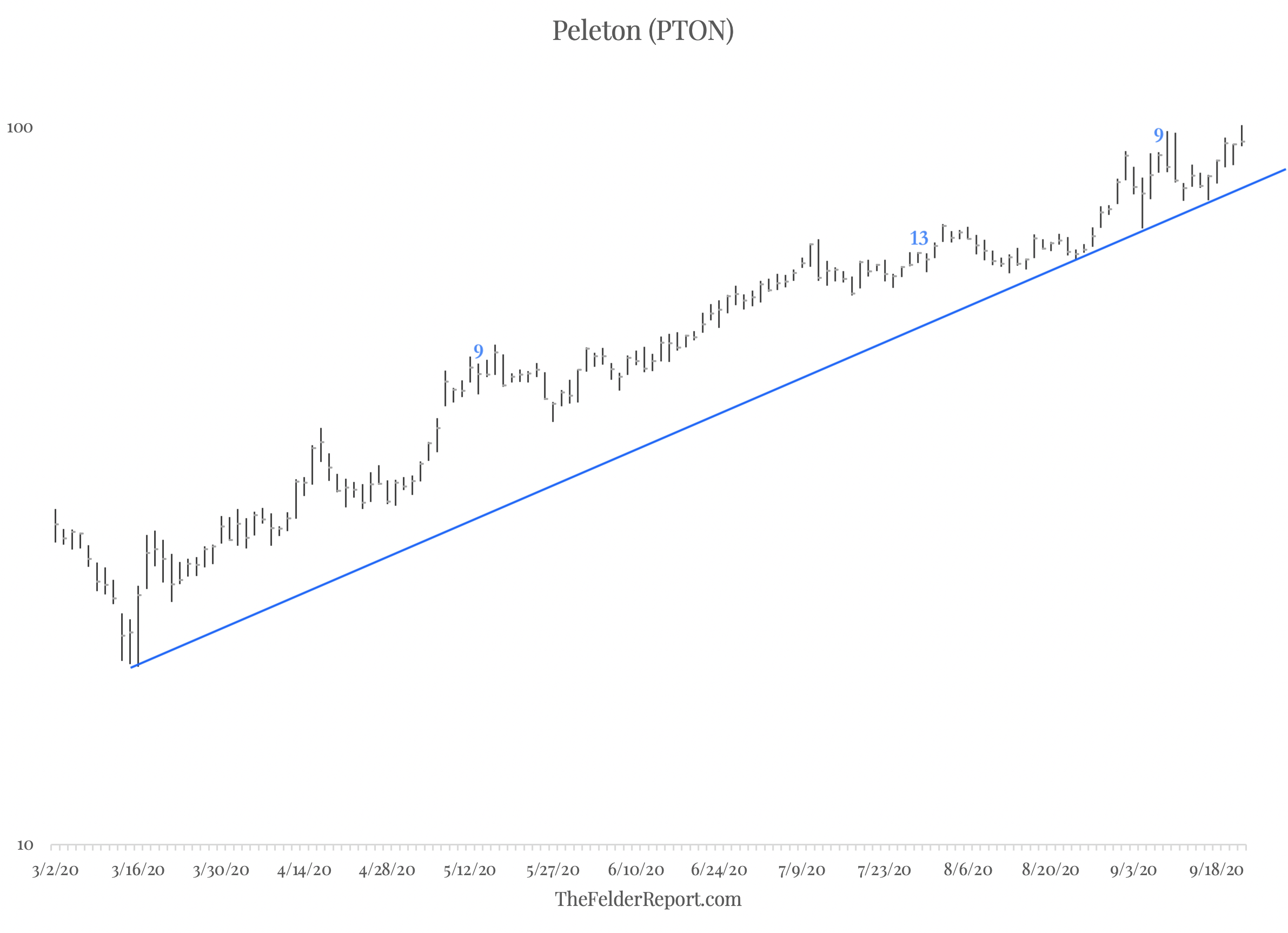

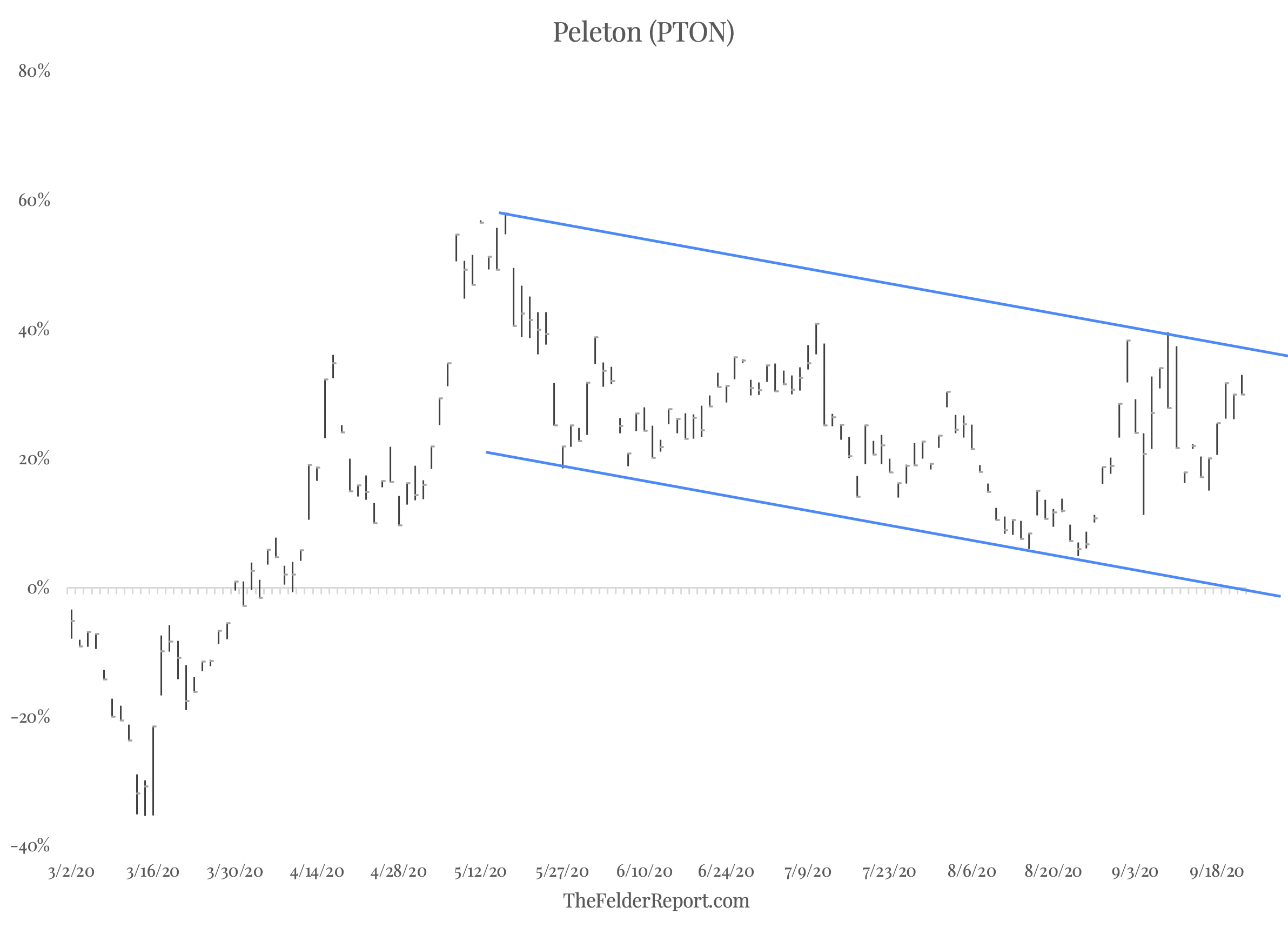

Technically, the stock has been in a strong uptrend since the March lows. However, it recently completed a daily DeMark Sequential 9-13-9 sell signal. Today, it appears to have possibly put in a false breakout, leaving a shooting star candlestick. What’s more, momentum (as measured by price relative to the 50-day moving average) peaked way back in May and has been waning since. Together, these signal suggest a change in the short-term trend could be underway.

In all, Peleton looks like an interesting opportunity on the short side. The valuation is extreme and built upon an environment that is uniquely unsustainable. Upward momentum appears to be close to exhaustion and insiders are selling like there’s no tomorrow. Perhaps, for Peleton, there is no tomorrow that will ever present as good an opportunity to sell as today does.