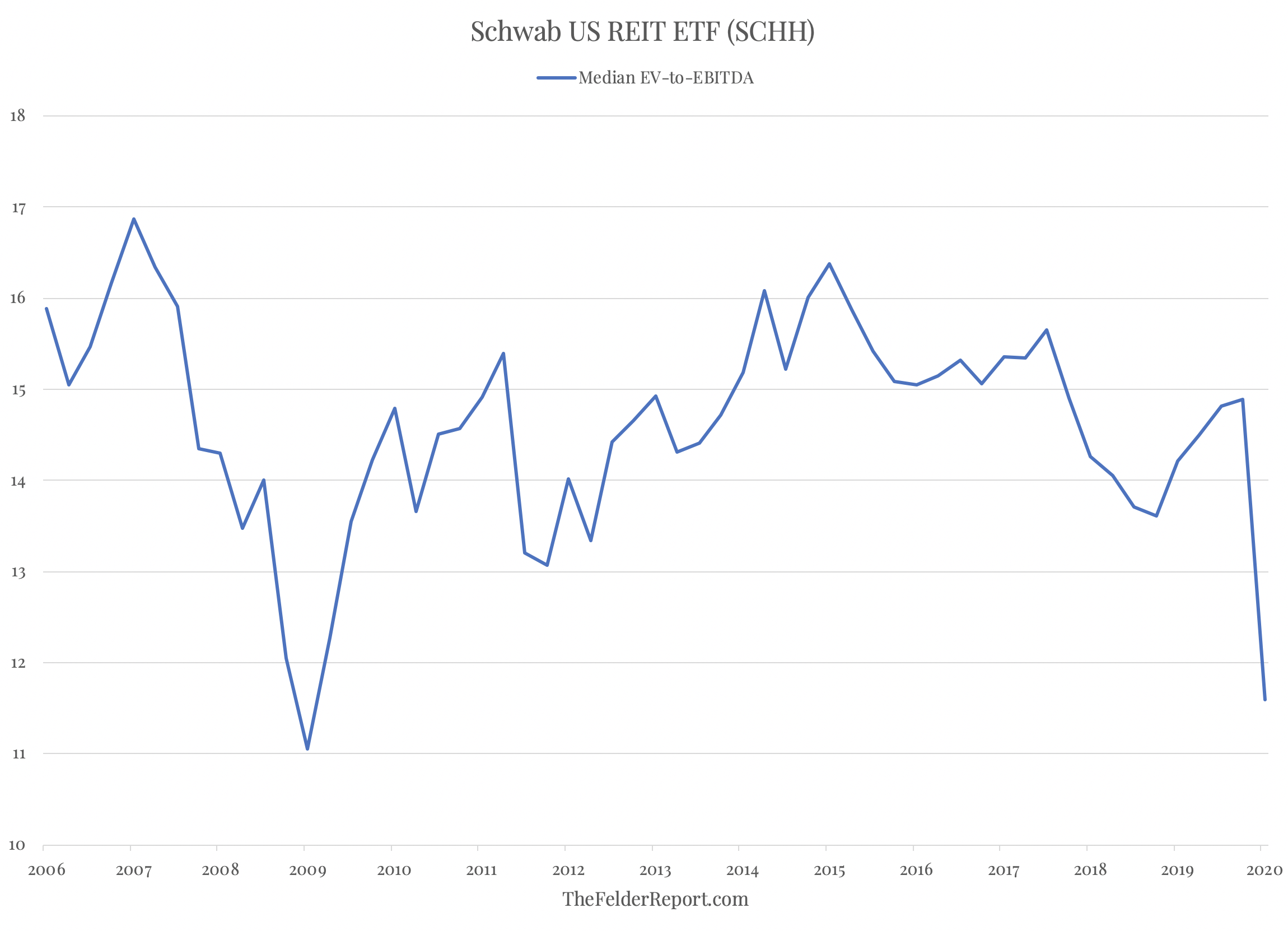

REITs have been one of the hardest hit sectors since the stock market crash began about a month ago, falling nearly 50% compared to the roughly 35% decline in the S&P 500. As a group, they now represent good value. The median enterprise value-to-EBITDA has fallen to about 11.5, the lowest level since the 11 reading at the bottom of the Great Financial Crisis.

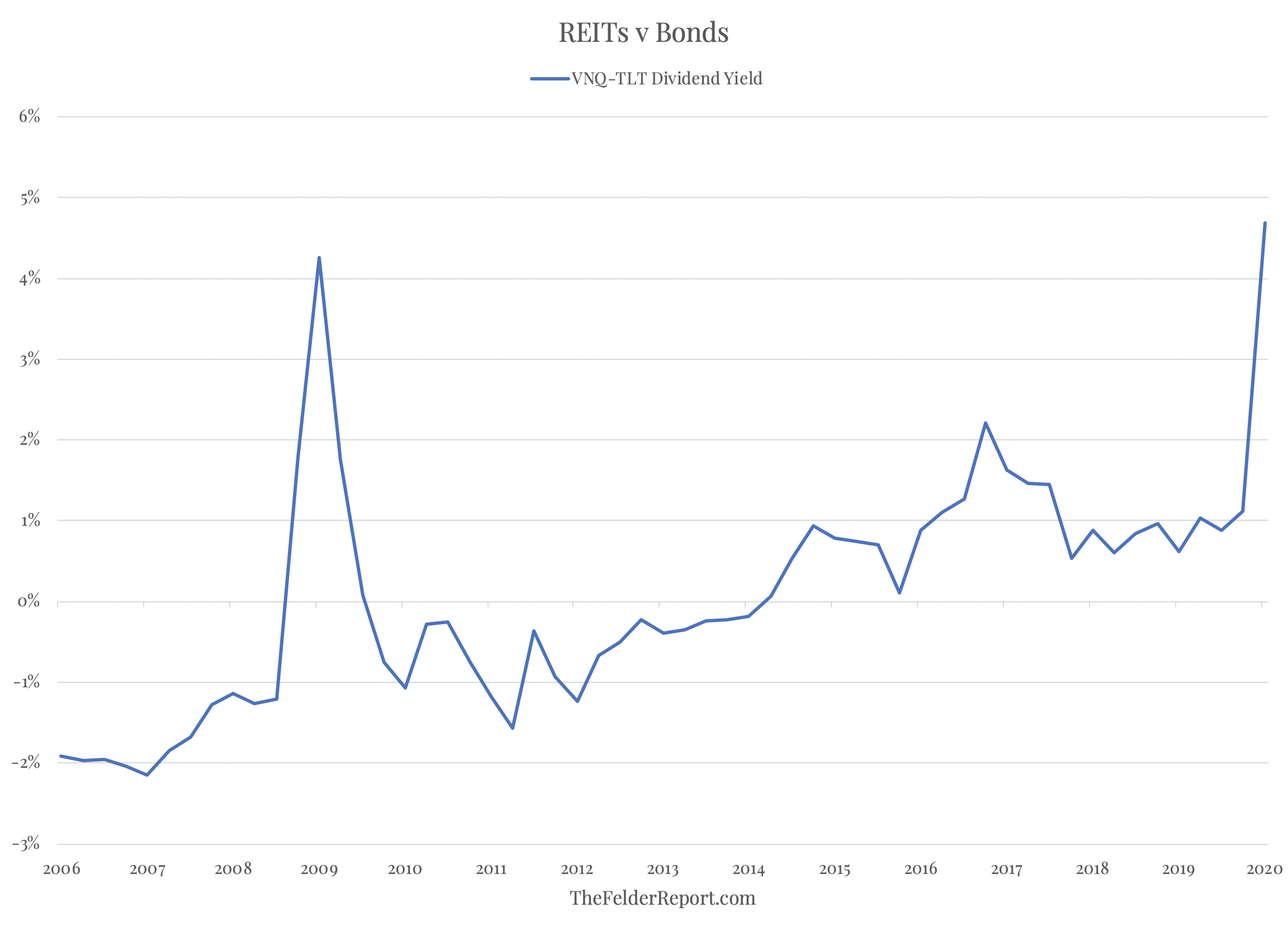

The major difference today is that “risk-free” rates were much higher back then than they are today. In terms of relative value, REITs may have never been cheaper than they are right now.

This is probably why REITs are one area where recent insider buying has clustered. For these reasons, I am taking this allocation back to neutral from underweight. Our tactical ETF portfolio now reflects this change.