“It says something about sentiment that some retail traders (erroneously) believe they have discovered a market loophole whereby philosophically the only limiting constraint on their success is the degree of their own conviction and willingness to act upon it (by buying calls.)” This was how Luke Kawa concluded his piece in Bloomberg’s “5 Things” newsletter on Tuesday and I believe it does a terrific job of encapsulating the zeitgeist in the stock market today.

Many have asked, ‘What in the world is driving stock prices higher today while earnings have been falling for the past year, stock buybacks are dwindling, signs of recession are popping up everywhere, an epidemic looks be evolving into a pandemic and the end of the Fed’s greatest liquidity injection of all time is in sight?’

The answer is the same thing that ends every speculative mania. A crescendo of euphoric buying by the uninitiated. By “euphoric buying” I simply mean leveraged speculation that will only pay off in the most extreme upward explosion and by “uninitiated” I am referring to those who have not experienced a crash in their adult lifetimes.

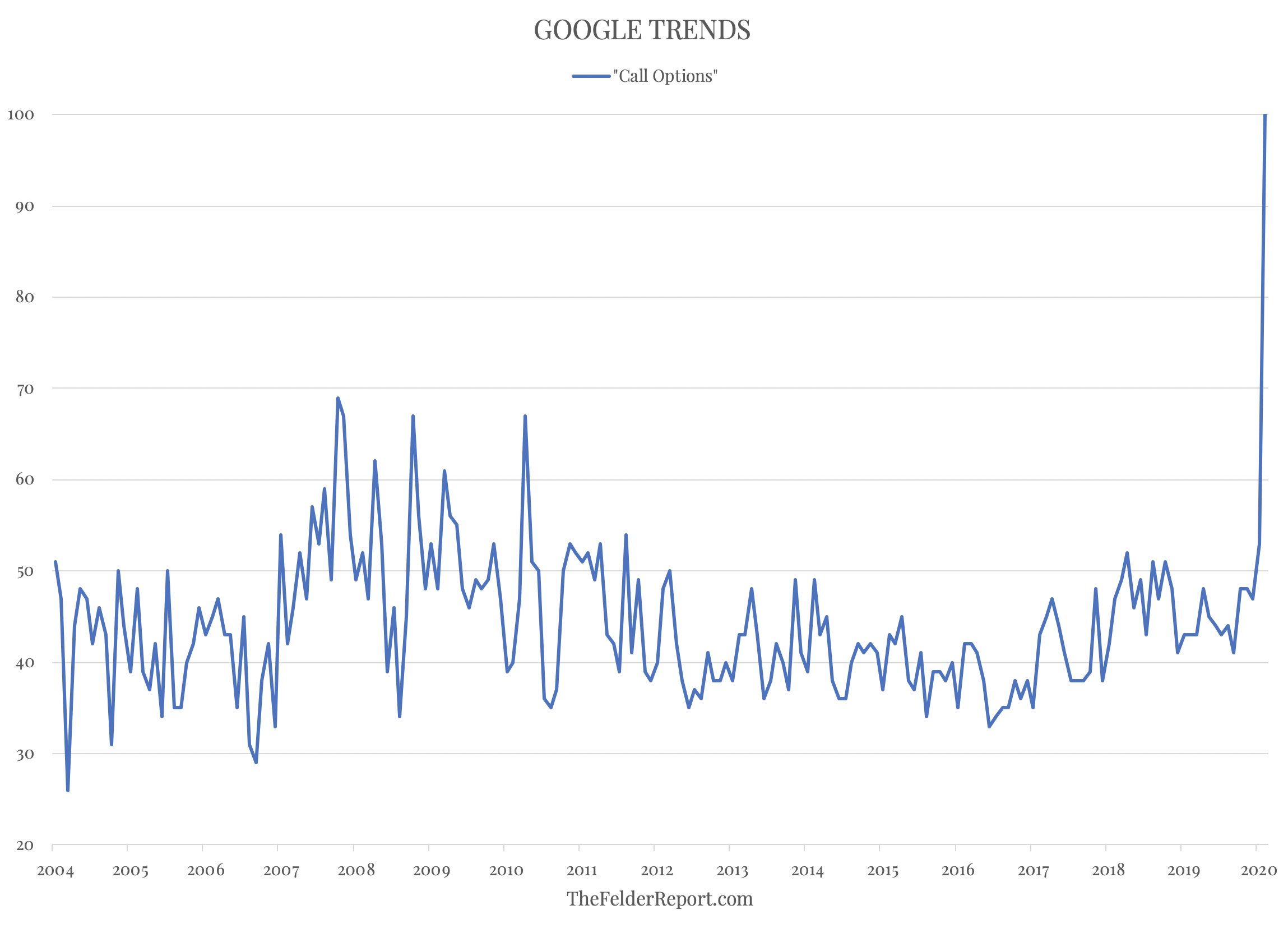

The evidence to the former is substantial. Google searches for the term “call options” are soaring to their highest levels on record dating back to 2004. The volume is roughly double any other peak we have seen over the past decade. Search “call options” on YouTube and the most popular video over the past week is a “how to” on buying Tesla call options, (hat tip, Grant Williams). The video’s creator divulges, “I recently, though, got into buying call options. I had no idea what these were until I had a few people on Twitter posting about them, a few people at work even.” This probably helps to explain all of the Google search activity. Clearly, retail traders like this gentleman have now “discovered a market loophole” and need Google to help them take advantage of it.

The evidence to the former is substantial. Google searches for the term “call options” are soaring to their highest levels on record dating back to 2004. The volume is roughly double any other peak we have seen over the past decade. Search “call options” on YouTube and the most popular video over the past week is a “how to” on buying Tesla call options, (hat tip, Grant Williams). The video’s creator divulges, “I recently, though, got into buying call options. I had no idea what these were until I had a few people on Twitter posting about them, a few people at work even.” This probably helps to explain all of the Google search activity. Clearly, retail traders like this gentleman have now “discovered a market loophole” and need Google to help them take advantage of it.

To understand the extent to which these call options trades are now moving the market, Goldman Sachs found, the notional volume of single stock options traded as a percent of the notional volume of shares traded recently rose to 91%, a new record high. In other words, the activity in call options now rivals the amount of trading in the actual stocks themselves. The difference here is that there is a market maker on the other side of an options trade who must hedge his exposure. Because he’s short a call he must go buy stock in the open market roughly equivalent to the notional value of the option.

Therefore, this leveraged speculation in options is allowing a group of traders with far less capital than would otherwise be required to move markets of this size to move the market. Why is Microsoft seeing its stock price go parabolic? Why is Tesla? Why is Shopify? In addition to record inflows into tech funds and their overweight exposure in uber-popular ESG funds, it is due to thousands of amateur options traders buying call options forcing market makers to buy the common. And as stock prices go up, market makers are forced to buy even more resulting in a virtuous cycle.

To further put an exclamation point on just how prevalent this speculative activity has become, Jason Goepfert, of SentimenTrader, last week noted that the explosion in activity among retail traders is totally unprecedented. eTrade DARTs, or Daily Active Revenue Trades, also just soared to new record highs, nearly 50% greater than the high we saw in early-2018 which led into the “volmageddon” mini-crash.

All of this panic buying among retail traders, especially concentrated in the options market, has helped to push the SKEW Index to its highest level since August of 2018, just prior to the waterfall decline in the broad stock market later that year. Known more familiarly as the “Black Swan Index”, SKEW is published by the CBOE as an indicator of “tail risk” in the market. The Wall Street Journal reported last week on the implications of such a high reading:

Far from indicating a widespread worry about a Black Swan event, she [Jessica Wachter, a finance professor at the Wharton School] says, it probably signified that the consensus among traders had become significantly more optimistic. The reason for this, Prof. Wachter says, is that a high SKEW reading in essence means that there is a significant pocket of aggressive bearishness that is far outside the range of opinions among everyone else. She points out that a rising SKEW reading therefore doesn’t automatically mean that any erstwhile bulls have become aggressively bearish. It instead could indicate that the mainstream consensus has become significantly more bullish.

This idea that the consensus has become significantly more bullish is validated not just by the rampant call activity noted above. It is also represented by the fact that the stock market is now only factoring in a 2% chance of recession this year even as most economists assess it to be 25% and a quantitative model developed by researchers at MIT and based on the trends in industrial production, non-farm payrolls, stock market returns and the slope of the yield curve puts it at 70%.

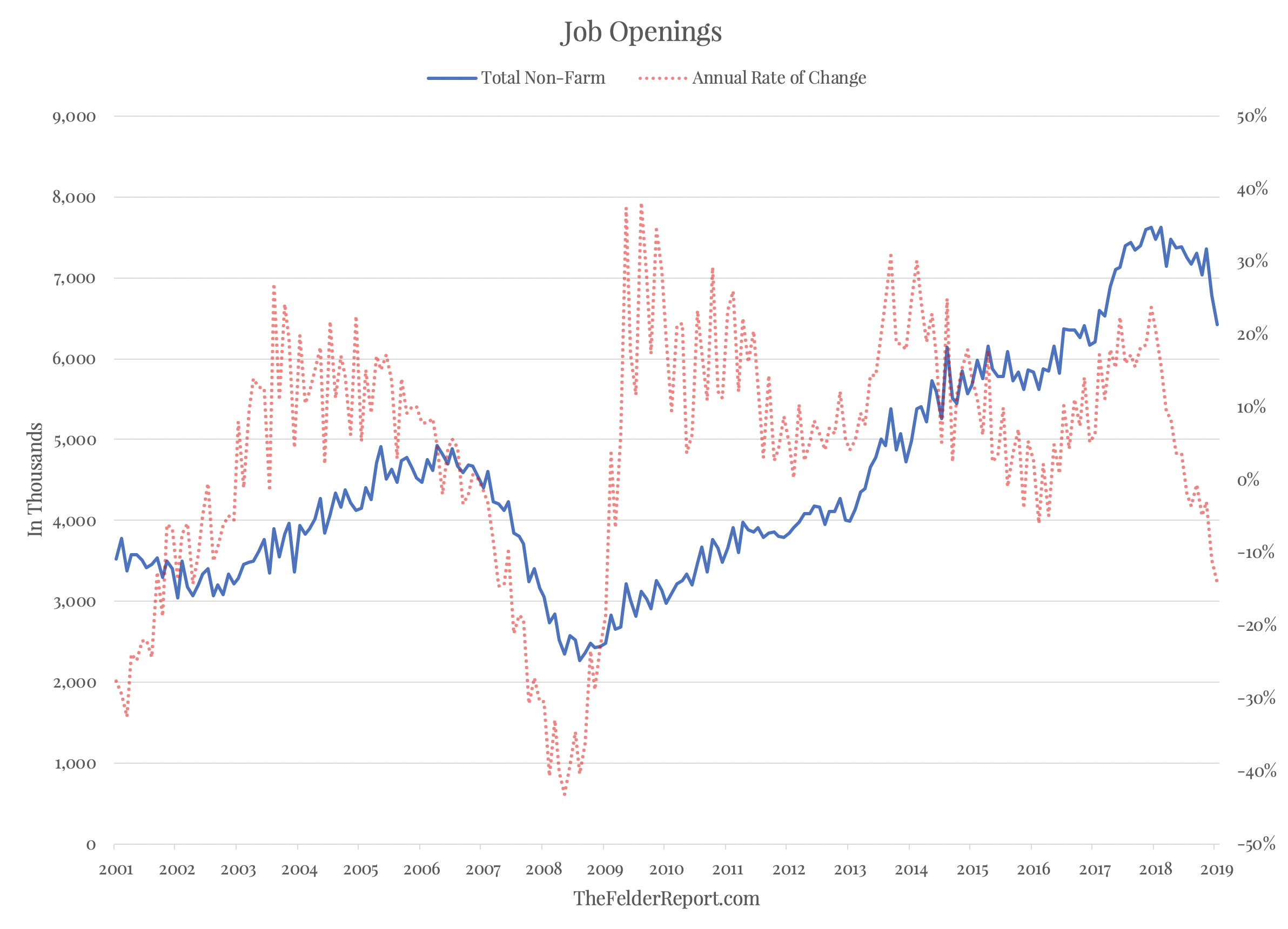

Confirming the more bearish reading from the guys and gals at MIT was the job openings number that was reported last week. December saw total non-farm job openings fall to 6,423,000 from 6,787,000 in November and 7,625,000 in December of 2018, amounting to an annual decline of 14%. As Julien Bittel pointed out on twitter, the last time this number fell by this amount year-over-year was 2008, when we were entering the throes of the Great Financial Crisis. Meanwhile, as Julien points out, the stock market is discounting a gain in job openings of more than 20%.

Confirming the more bearish reading from the guys and gals at MIT was the job openings number that was reported last week. December saw total non-farm job openings fall to 6,423,000 from 6,787,000 in November and 7,625,000 in December of 2018, amounting to an annual decline of 14%. As Julien Bittel pointed out on twitter, the last time this number fell by this amount year-over-year was 2008, when we were entering the throes of the Great Financial Crisis. Meanwhile, as Julien points out, the stock market is discounting a gain in job openings of more than 20%.

Remember that this is all before news of the Wu Flu, Coronavirus, Covid-19 or whatever you choose to call it really began to take off. As the New York Times put it, “Several key markets — like crude oil — had already been showing softness, suggesting that the global economy was weak even before the virus hit.” One of those key markets or indicators is the state of global commerce. The Wall Street Journal reported, “Growth in global trade sank to a meager 1% last year, down from 4% in 2018 and 6% in 2017. It was the fourth worst showing in 40 years, and the worst ever outside a period of recession, according to International Monetary Fund data.” Considering China is essentially closed for business right now, it’s hard to see how this already recessionary number will not deteriorate even further, possibly in dramatic fashion.

Still, the stock market is clearly operating under the assumption that any slowdown in the first quarter will be followed by a v-bottom and a rapid rebound in the second and third quarters. Analysts thus feel confident in “looking through” the weakness that might materialize as a result of the first epidemic in nearly two decades. But I would tend to agree with WSJ’s Justin Lahart who warned, “Beware of Wall Street’s Armchair Epidemiologists.” China has been reporting a steady rise in Wu Flu cases since it first was announced and it looks to some to be too steady. Ben Hunt wrote last week:

All epidemics – before they are brought under control – take the form of… an exponential function of some sort. It is impossible for them to take the form of… a quadratic or even cubic function of some sort. This is what the R-0 metric of basic reproduction rate means, and if – as the WHO has been telling us from the outset – the nCov2019 R-0 is >2, then the propagation rate must be described by a pretty steep exponential curve. As the kids would say, it’s just math.

China would have us believe the impossible. But even the White House is now calling the data into question. Edward Lawrence, Fox Business correspondent, tweeted, “Administration sources say they believe China is under reporting the number of Coronavirus cases by at least 100,000 in China. Also sources say the administration believes China is ‘severely’ under reporting the number of deaths from the virus.” A Nowcasting estimate published in The Lancet confirms these findings.

In stark contrast to Wall Street’s armchair epidemiologists, real ones are coming to a far bleaker conclusion. Marc Lipsitch, professor of epidemiology at the Harvard T.H. Chan School of Public Health and head of the School’s Center for Communicable Disease Dynamics, told the Harvard Gazette, that rather than seeing a peak in the number of new cases, “I think it’s more likely to be that it’s gathering steam.” He went on, “There’s likely to be a period of widespread transmission in the U.S…. I think we should be prepared for the equivalent of a very, very bad flu season, or maybe the worst-ever flu season in modern times.” Another expert with even more direct experience with the virus sees the situation as even more dire. Bloomberg reported:

In stark contrast to Wall Street’s armchair epidemiologists, real ones are coming to a far bleaker conclusion. Marc Lipsitch, professor of epidemiology at the Harvard T.H. Chan School of Public Health and head of the School’s Center for Communicable Disease Dynamics, told the Harvard Gazette, that rather than seeing a peak in the number of new cases, “I think it’s more likely to be that it’s gathering steam.” He went on, “There’s likely to be a period of widespread transmission in the U.S…. I think we should be prepared for the equivalent of a very, very bad flu season, or maybe the worst-ever flu season in modern times.” Another expert with even more direct experience with the virus sees the situation as even more dire. Bloomberg reported:

As the number of coronavirus cases jumps dramatically in China, a top infectious-disease scientist warns that things could get far worse: Two-thirds of the world’s population could catch it. So says Ira Longini, an adviser to the World Health Organization who tracked studies of the virus’s transmissibility in China. His estimate implies that there could eventually be billions more infections than the current official tally of about 60,000.

This stands in stark contrast to the assumptions being made by those whose livelihood depends on them not understanding it, to botch the Upton Sinclair quote. Stock prices at record highs and, more importantly, record high valuations have clearly embodied Alfred E. Neuman’s catch phrase, “What, me worry?” In the face of some the of the greatest risks to the economy and bull market we have seen in at least a decade and possibly ever, investors are reaching for risk in ways they have never done before. It is so dichotomous it’s almost impossible to believe. Truth is stranger than fiction, as they say.

As difficult as it may be to explain, Mark Spitznagel described it thus: “When the stock market is no longer tethered to fundamentals—that’s the distorted environment we live in, that’s just where we are—when that happens, any price can print. Any price can print. We shouldn’t be surprised by anything on the upside at this point because what’s tethering the markets?” What, indeed?

Then again, while the stock market may be a voting machine in the short run, it is, and will always be, a weighing machine in the long run, to paraphrase Ben Graham. And when the market is forced to weigh the risks that are already growing in both probability and severity the uninitiated will be initiated and a stock market crash will ensue. And while some now believe that day of reckoning will never come because the Fed is capable of forestalling recession indefinitely, they may soon be forced to ask whether the Fed can forestall an epidemic that could potentially rival the Spanish flu.

Jerome Powell recently admitted that the Fed’s tools in dealing with another recession are limited at best. Still, investors believe otherwise. But it’s hard to imagine the psychological jiu jitsu required to believe a room full of academics with expertise limited to the “dismal science” and tools relegated to the monetary system to solve a global health crisis. Yet, having witnessed the lengths to which the current euphoria has now extended, I wouldn’t put it past them.