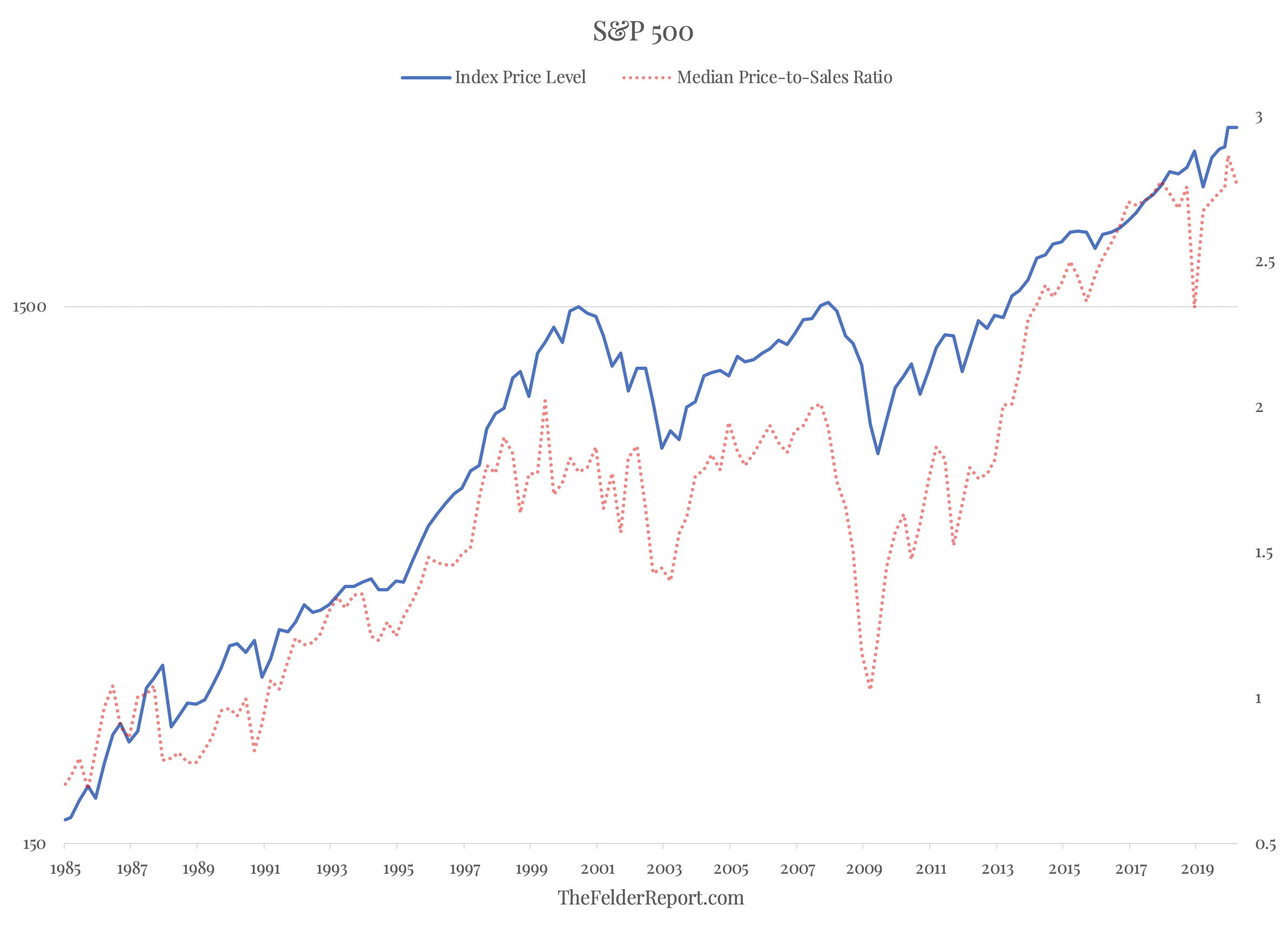

Stocks declined slightly for the month of January but valuations remain extremely stretched. In fact, based on the median price-to-sales ratio of the S&P 500 they are nearly 50% more overvalued than the were at the peak of the dotcom mania. In other words, this median stock could fall by a third overnight and stocks would still be as extremely overvalued as they were at the peak of the most overvalued market in modern history.

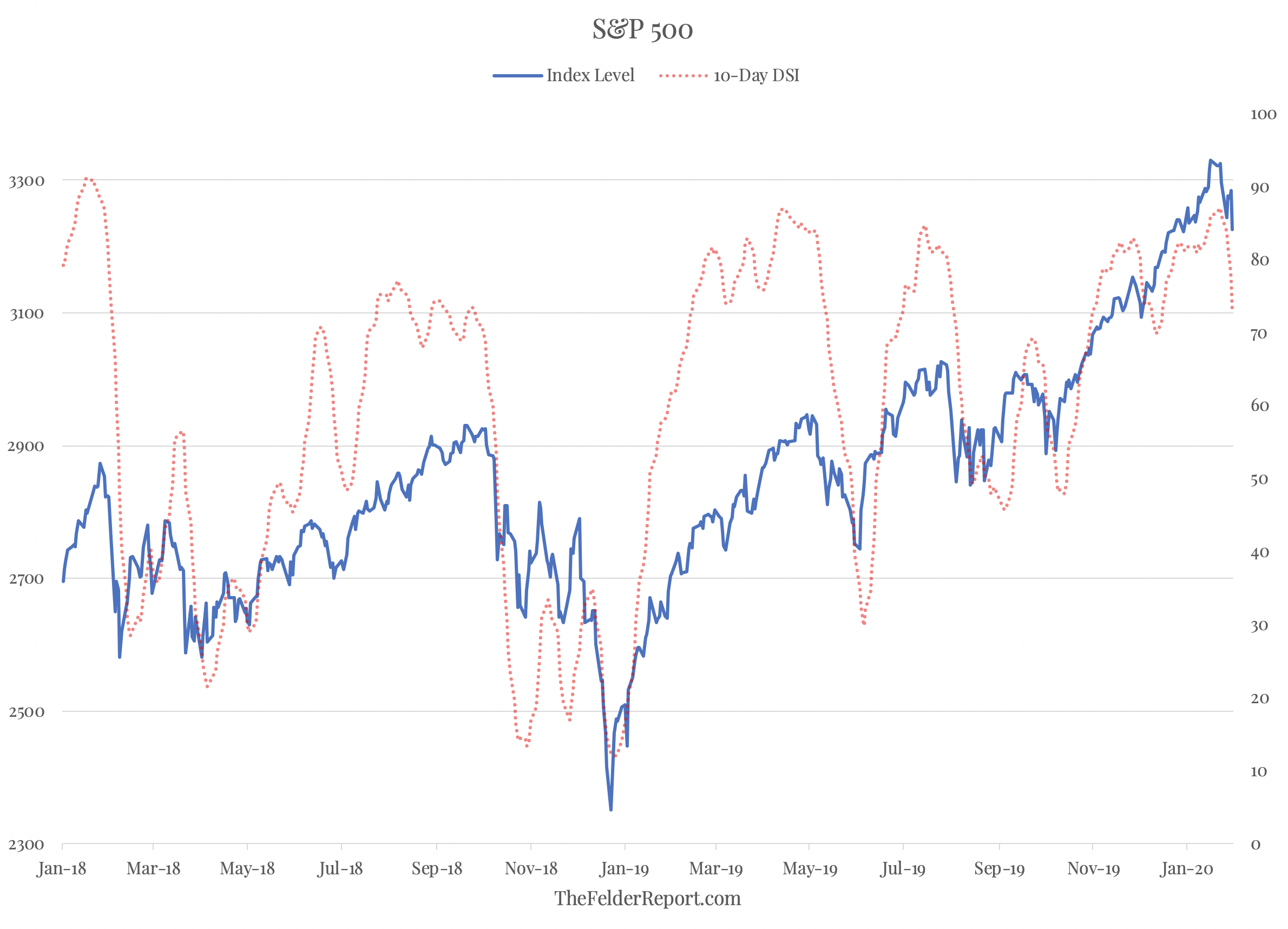

The rally over the past year or so has also seen short-term sentiment become very stretched once again. While margin debt, what I consider to be a good measure of long-term sentiment, has diverged from prices during the latest rally, the Daily Sentiment Index recently rose to its highest levels of the past few years. So not only are investors paying the highest prices on record, they have become very excited about doing so and their greed should make us fearful.

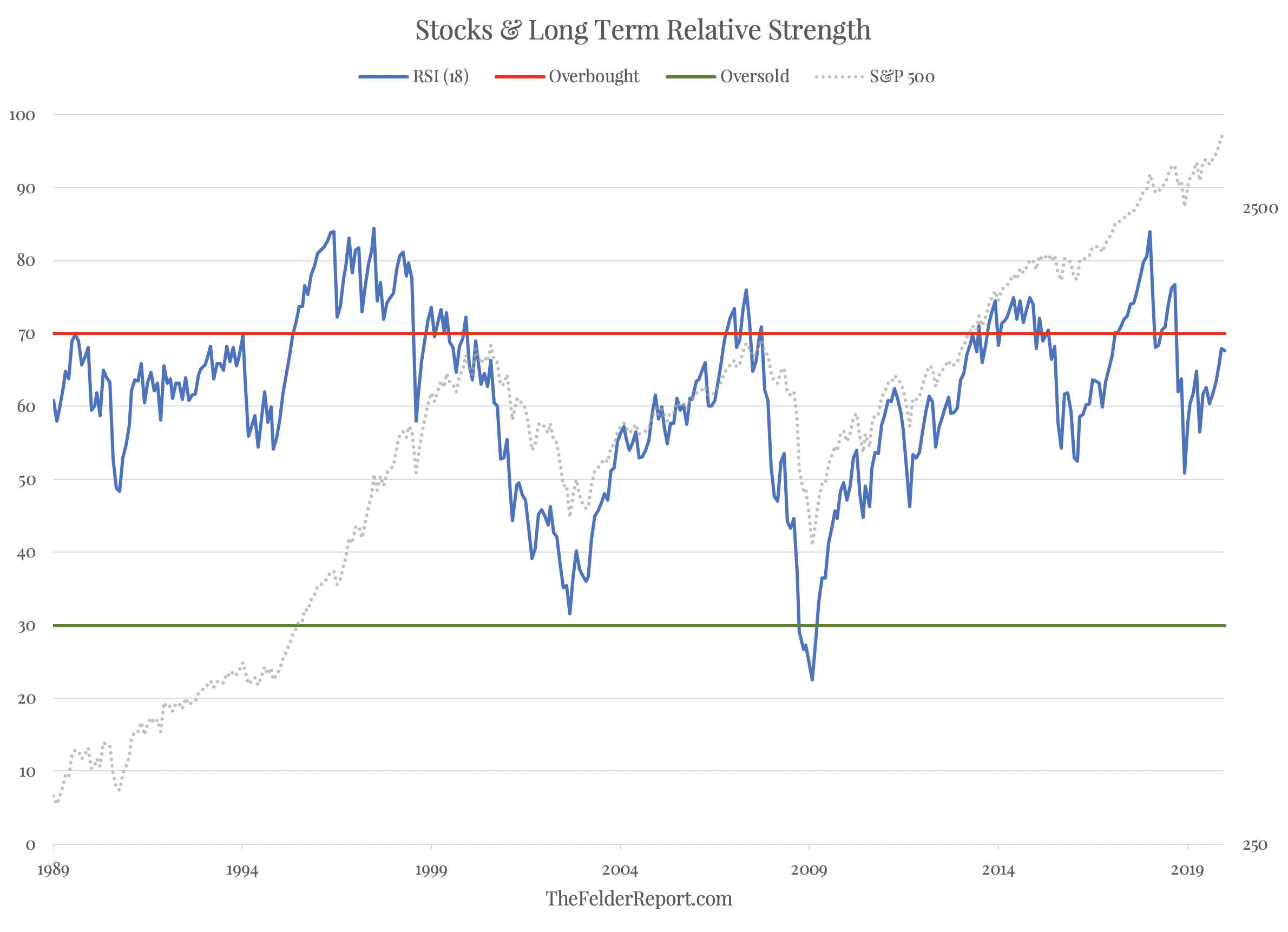

Finally, technicals show that 18-month RSI is nowhere near confirming the new highs in prices we have seen over the past few months. In fact, it peaked just about two years ago when DSI was at a similarly extreme reading. The pattern of new highs with diverging momentum is typical of major topping patterns.

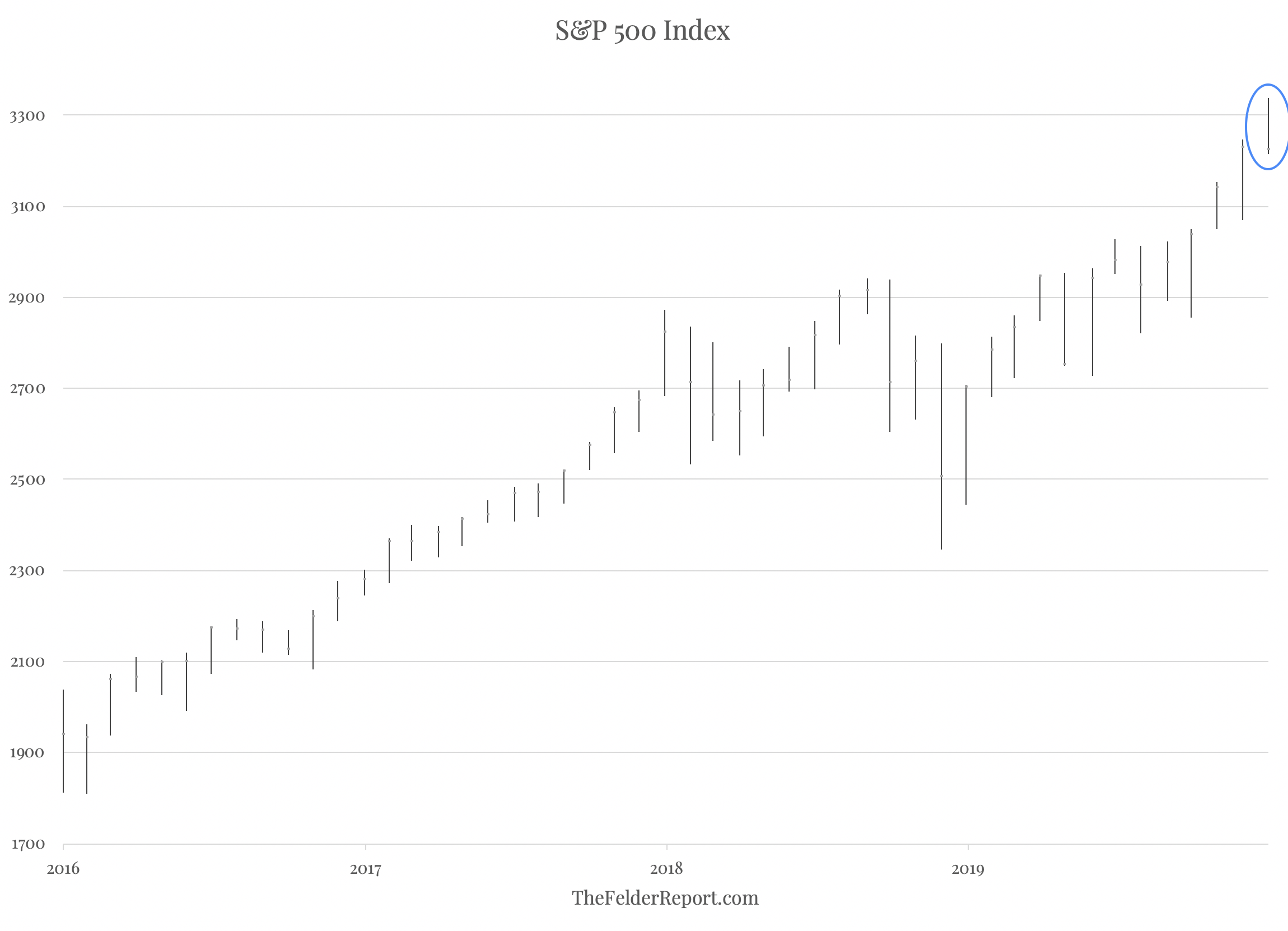

What’s more, January’s trading resulted in a “shooting star” candlestick, a bearish reversal pattern that results from the index trading significantly higher during the month only to fall back and close lower than its opening price, leaving a long wick above. This is a pattern commonly seen at price peaks and is essentially the opposite of a bullish hammer formation that can be found at many price bottoms.

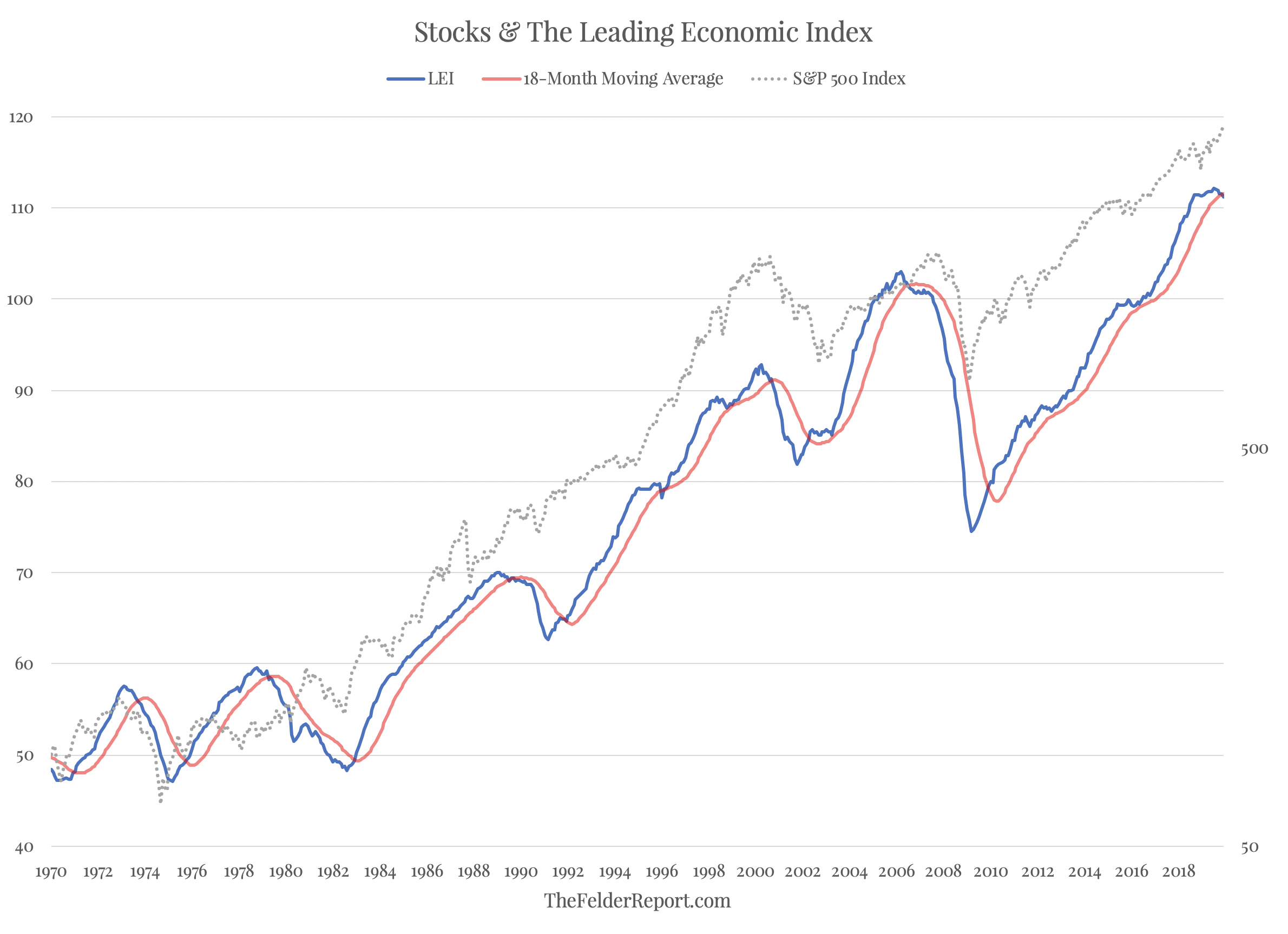

Finally, as noted in a recent market comment, the Conference Board’s Leading Economic Index crossed down below its 18-month moving average in December. In the past, this has proved to be a good early warning sign of impending recession. For this reason, it has also been a good sign of an impending bear market.

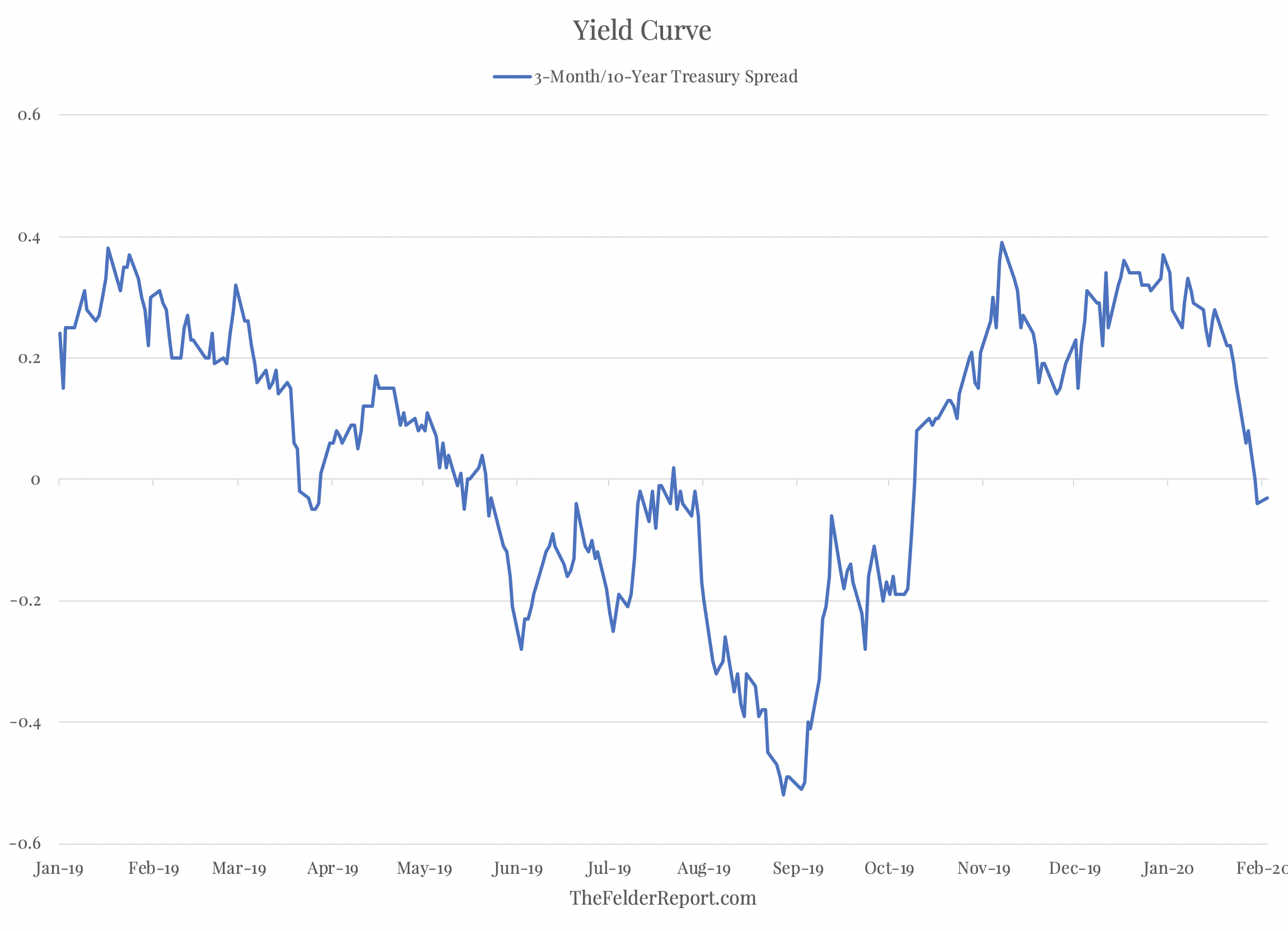

In all, the situation facing equity investors is as fraught with risk as ever. Valuations suggest the upside is limited and the downside is significant while sentiment points to a euphoric extreme and technicals show momentum waning and possibly even reversing lower. At the same time, the macroeconomic backdrop is no longer supportive of prices with leading indicators rolling over and the yield curve inverting once again.

As a result, prudent investors should look to limit their general market risk in a way that makes sense for them. This could be simply reducing exposure to equities by selling off some holdings or by implementing a “tail hedging” program as outlined here. In the Tactical ETF Portfolio, it simply means we have no exposure to an asset class that represents “reward-free risk.”

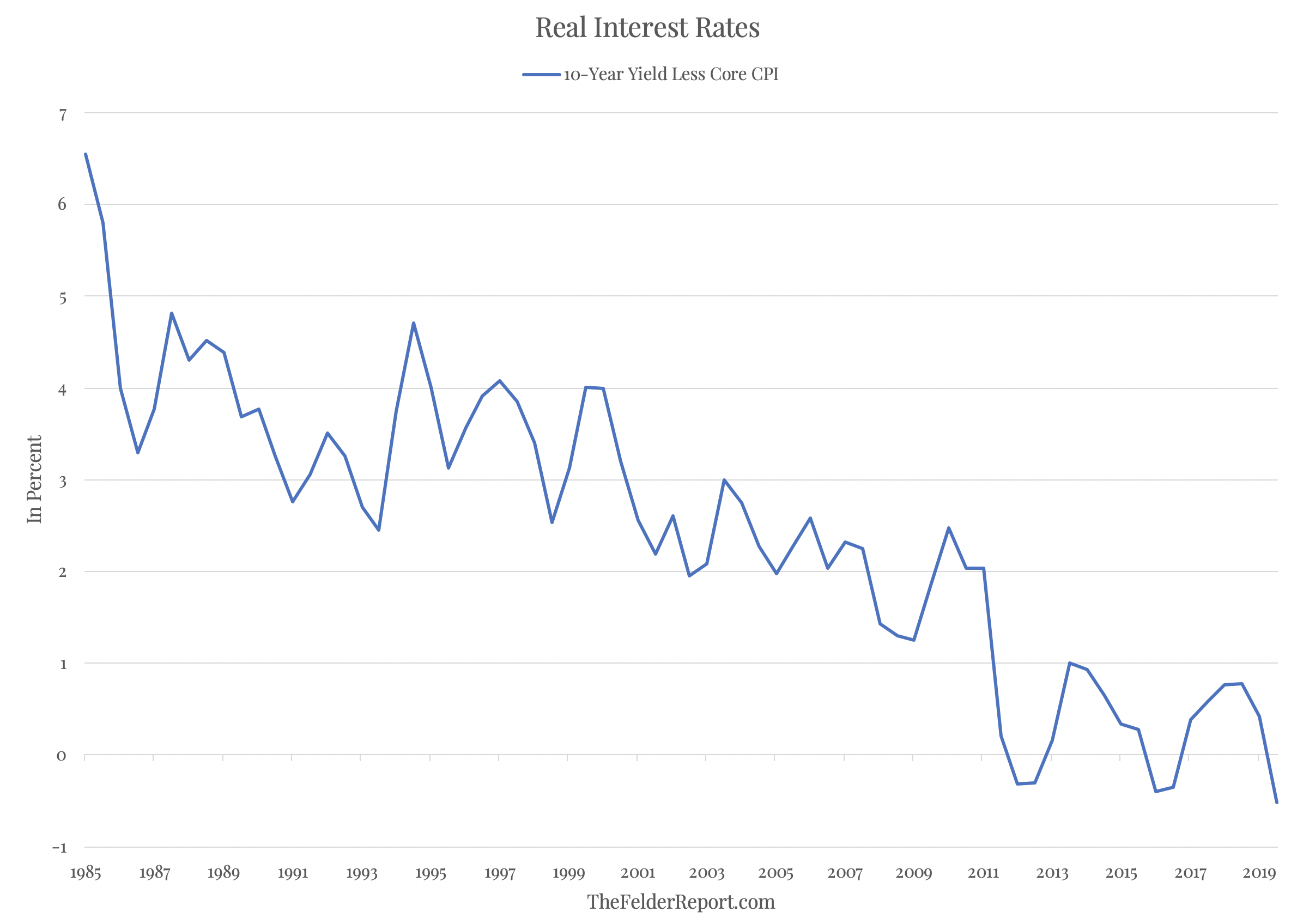

As for bonds, it’s hard to say they offer any better value than stocks when the real yield on the 10-year treasury note is more negative than it has been in decades. What this means is that investors are glad to tie money up right now for the next 10 years at a rate of return that nearly guarantees a loss of purchasing power and potentially a very significant loss (depending on what inflation does over that time).

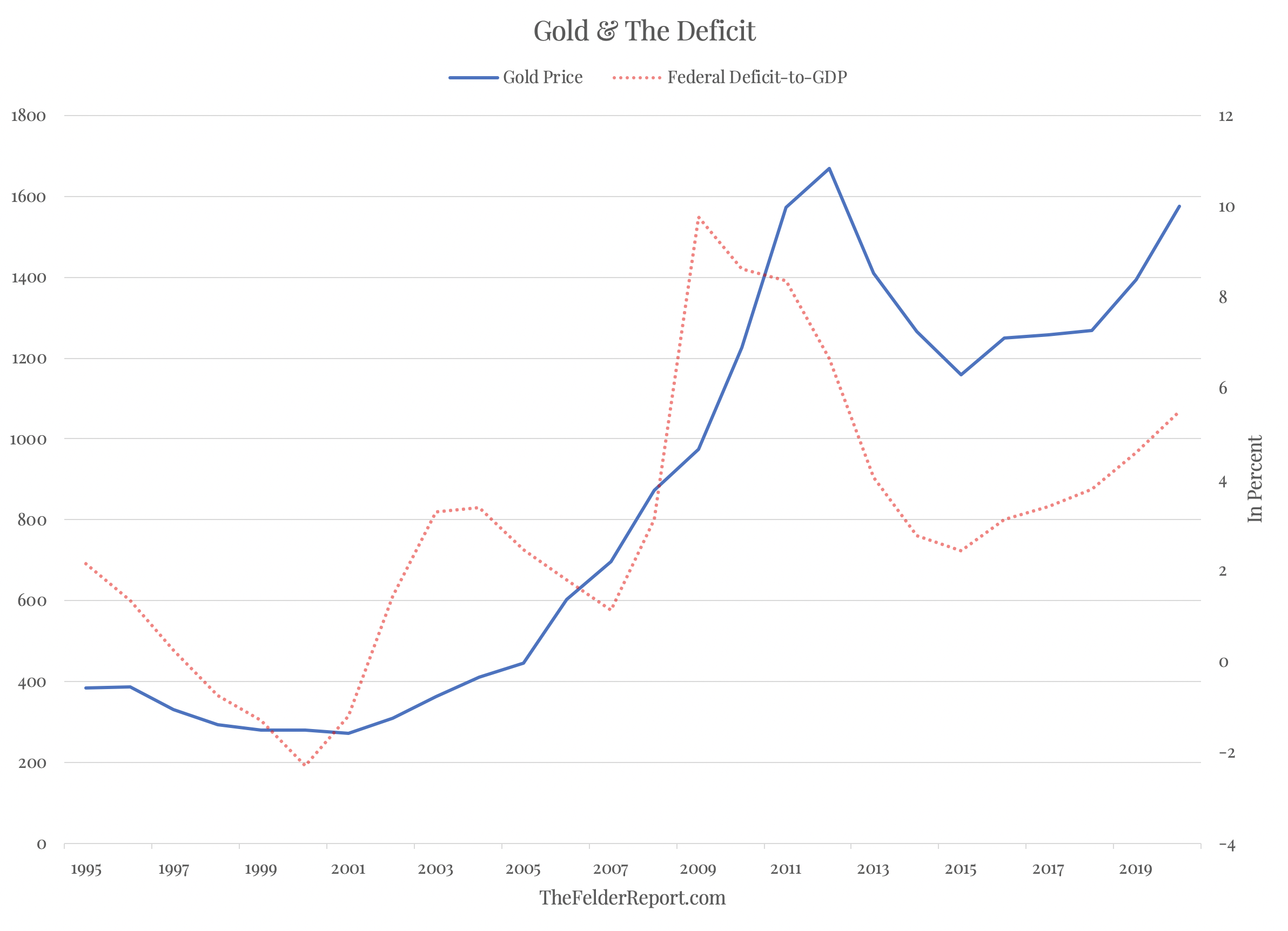

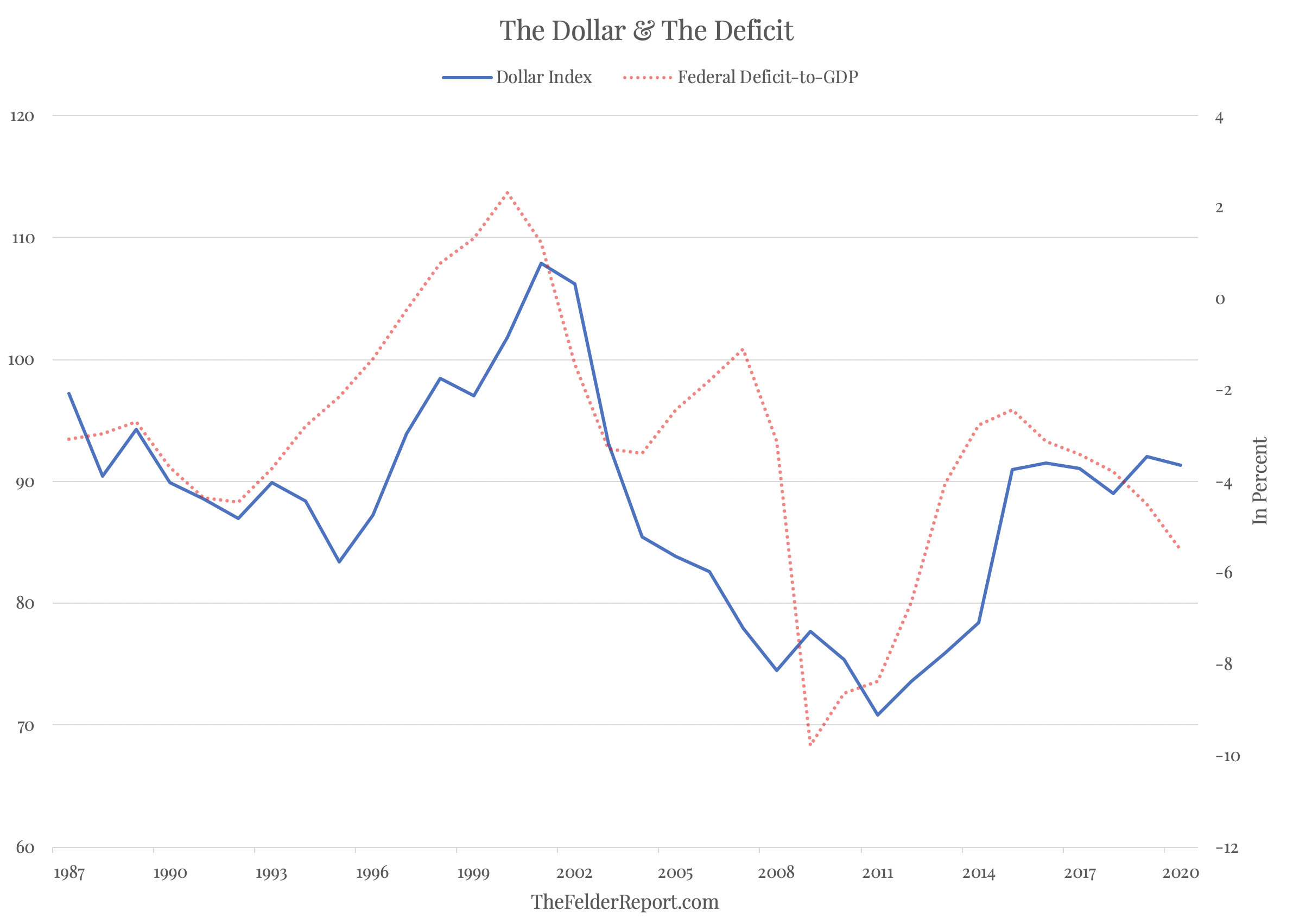

In such an environment, I would much prefer to own real assets to financial ones. Commodities make for an interesting investment case when money printing is the order of the day. When that money printing coincides with fiscal profligacy that case becomes even more attractive. I am especially interested in gold and oil today. The former because it serves as an effective alternative currency when the dollar is being explicitly devalued. If we are, in fact, headed for recession then the deficit could easily blow out to a new modern era high. In reaction, gold would likely break out to new record highs in price, as well.

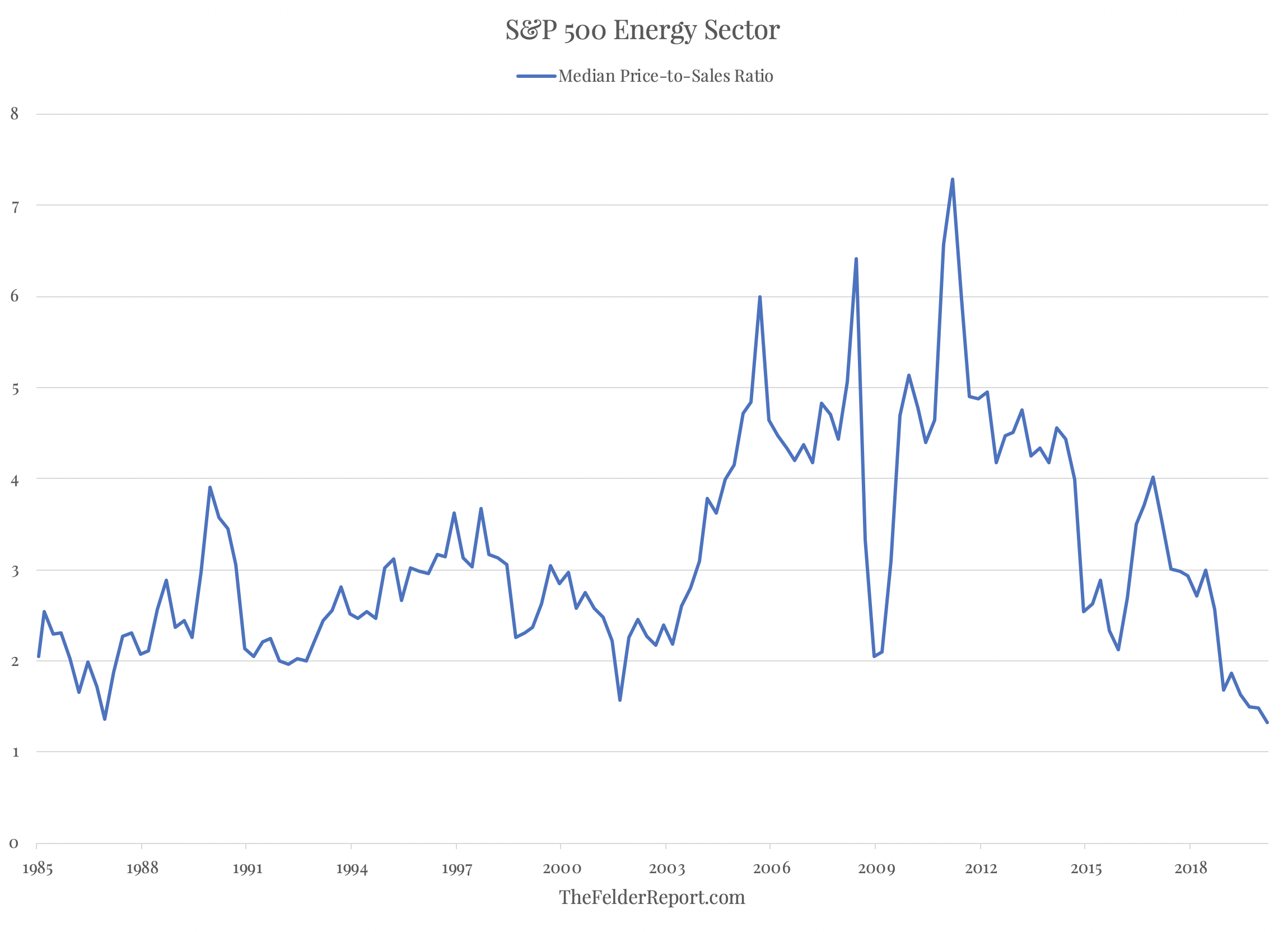

The oil sector, which now represents less than 4% of the S&P 500, may be the only truly attractive sector in the entire stock market from a value standpoint. While the broad S&P 500 trades at its highest median valuation in history, energy stocks trade at their cheapest median valuation in history. 1986 was the last time valuations were near current levels and over the following two years, Exxon Mobil doubled the price performance of the S&P 500.

And if the dollar is going to tank along with the federal deficit, as it is wont to do, it would be very bullish for oil prices (and bearish for the prices of financial assets). So there is a compelling case to be made for energy from both a fundamental and a macro perspective (not to mention the fact it is also the most contrarian thesis you might find right now).

From a big picture perspective then it appears wise to avoid financial assets at present in favor of focusing on real ones and for a number of reasons. There are a number of ways to express this in your portfolio but, for most investors, I would prefer to own gold directly (via CEF) and focus on the oil and gas exploration companies within the larger energy sector (via XOP). At the same time, limiting equity exposure is crucial and utilizing a value approach in that space (either quantitatively by way of a strategy such as that employed by FNDB or qualitatively by individual security analysis) for any remaining exposure seems more important than ever before.