How The Short Vol Trade Will Call The Fed’s Bluff

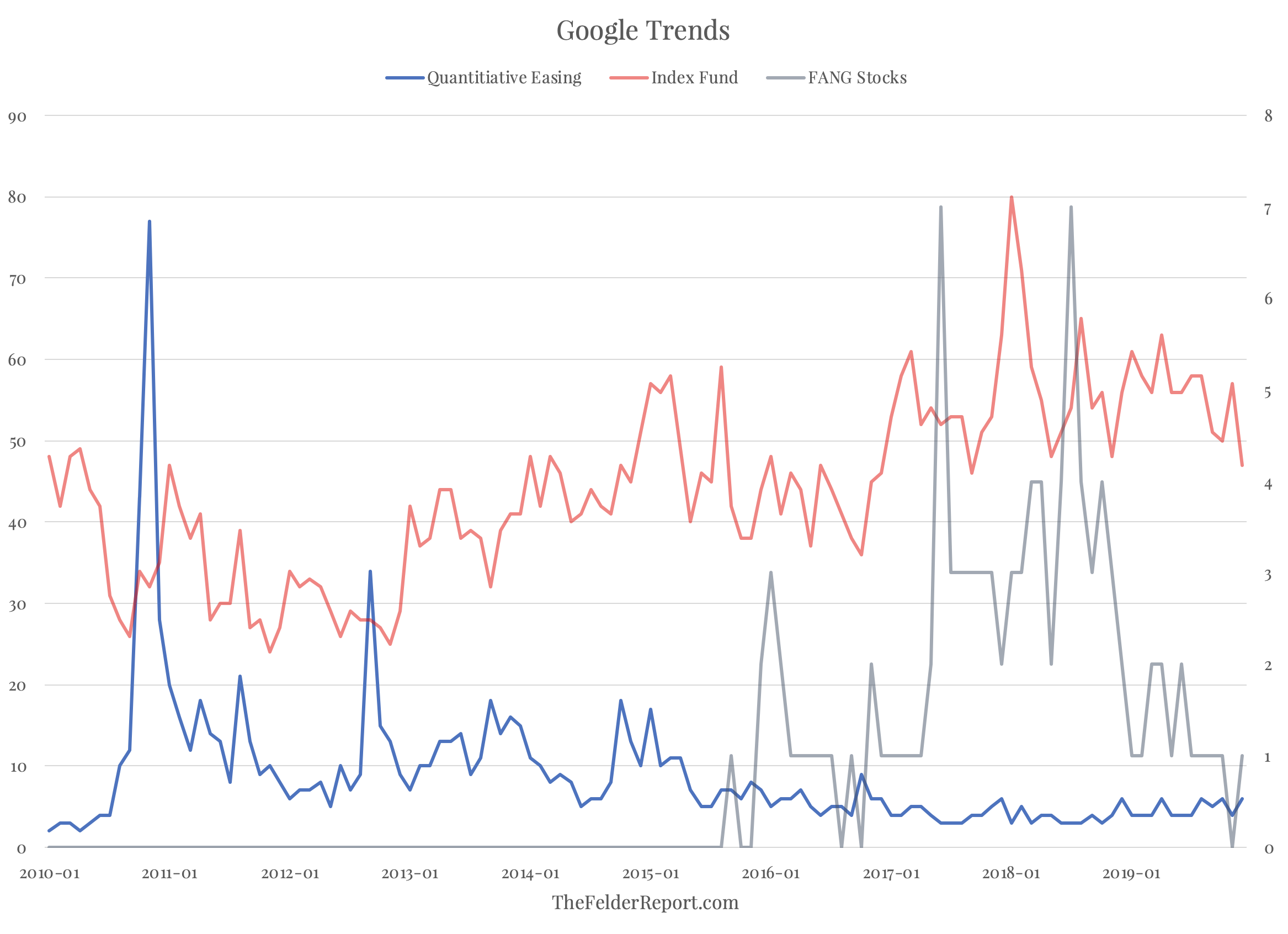

Over the past several years it seems the markets have been driven by a number of feedback loops that have grown in size and significance. I have written a fair amount here about the various narratives that I believe have driven the current mania. The growing belief that investing passively entitles an investor to historical rates of return regardless of the price paid is one. The infallibility of the FANG stocks is another. Last week, I focused on the belief that the Fed is propping up the markets through monetary policy.

Together, these individual narratives form a powerful story about the stock market that gives investors irrational confidence in it. And that confidence has grown so great that it has expanded from just buying stocks to buying on margin and even to selling naked put options and shorting volatility. And these manifestations of confidence serve to reinforce the narratives that are driving them.

For example, in the early days of this bull market a group of investors decided to buy into one or all of these narratives. As discussed last week, the QE narrative took off in the early part of this decade. The passive investing narrative matched up well with this one as the most efficient means of aligning investor portfolio with monetary policy which would lift all boats. Eventually, the FANG narrative joined the party as these stocks became some of the best-performing and largest holdings within the indexes.

For example, in the early days of this bull market a group of investors decided to buy into one or all of these narratives. As discussed last week, the QE narrative took off in the early part of this decade. The passive investing narrative matched up well with this one as the most efficient means of aligning investor portfolio with monetary policy which would lift all boats. Eventually, the FANG narrative joined the party as these stocks became some of the best-performing and largest holdings within the indexes.

The self-reinforcing nature of these narratives can’t be understated. When the QE narrative was validated by rising stock prices, it validated the belief in the passive narrative. And when the passive narrative was validated by one of the strongest bull markets in history, it validated FANG narrative. Each, in turn, inspired greater confidence on the part of investors to buy stocks which pushed prices higher thus inspiring even greater confidence and so on.

However, as mentioned earlier, investors did more than just buy stocks as a way to act on their confidence in these narratives. They went even further by leveraging up via margin debt. The greatest surge in leverage in the history of the stock market further pushed prices higher and made investors even more confident. Similarly, investors expanded their use of selling naked put options against the broad stock market, a leveraged bet on rising stock prices that lowers volatility and thus inspires greater confidence.

And for the first time in history, investors were able to go beyond these two leveraged trades and sell volatility directly. Whether selling VIX futures, buying short vol ETFs or shorting long vol ETFs this is a trade that we have never seen before and it has grown to massive proportions – so much so that it, too, has a significant, though hard to quantify, positive impact on the stock market itself.

'The current impact of ETP rebalancing is just smashing the VIX future. This creates a second-order signal to lever up/increase exposure for many volatility control, target volatility, Commodity Trading Advisers trend and risk-parity products.' https://t.co/lm6dniCkEJ

— Jesse Felder (@jessefelder) November 29, 2019

As I first wrote here a couple of years ago, the short vol trade is put on by speculators and is facilitated by market makers. These market makers end up long volatility. How do they hedge this? By buying equities in some form or another. Thus the short vol trade, when it is put on in size, represents a surge in demand for equities that depresses volatility and creates a positive feedback loop of its own. And when you figure in all of the volatility-targeting strategies out their like risk parity, the depressing of volatility through short selling can trigger a massive surge in equity demand all on its own.

This phenomenon has occurred on both a long-term time frame, i.e. over the past ten years or so, but it has also occurred in shorter cycles, as well. For example, the late-2017 rally in the stock market that went parabolic for a period of time was marked by a significant rise in volatility selling that saw the VIX fall under 10. The volatility selling during that time was clearly a positive feedback loop that went bad in early-2018 when volatility shot up, vol shorts were forced to cover and volatility-targeting strategies forced to sell which created a cascading decline in the stock market and saw the XIV, short vol ETF, eviscerated in after hours trading.

'Beyond expectations of a trade agreement, last month’s calm was created by a force that had nothing to do with the world getting better: swarms of investors betting against volatility itself.' https://t.co/DC83SQkVAx pic.twitter.com/doGKlBKdAP

— Jesse Felder (@jessefelder) December 4, 2019

The rally in the broad stock market this year has benefitted in similar ways to that earlier period and especially over the past few months. Volatility selling has once again become very popular, perhaps as part of the resurgence of the QE narrative, creating a positive feedback loop. This is really the only way to explain the fact that stocks have moved straight higher even as the repo markets signal problems in the country’s financial plumbing, earnings are in recession and the economy increasingly looks headed for recession, as well.

Volatility selling has grown to a new record over the past few weeks meaning this artificial equity demand from market makers and volatility targeting strategies has also grown to record levels further depressing volatility and inspiring even greater confidence in the short vol trade, itself. But there is a risk, now that the trade has gotten so large again, of this positive feedback loop reversing again into a vicious cycle.

'The Federal Reserve has been intervening more aggressively in money markets as it attempts to keep interest rates from rising around the end of the year.' https://t.co/ubD0orGN41

— Jesse Felder (@jessefelder) December 3, 2019

The catalyst for such a shift would be a shift in the bull market narratives which have recently begun to grow stale. The FANG stocks have gone nowhere for almost two years now calling into question their infallibility. The fact that the broad market gains over the past couple of years have also begun to fall below the average of the past decade is putting a dent in the passive investing narrative.

Most important, however, is the narrative that started it all: the story about the Fed and it’s ability to prop markets up via QE. First, there is the distinct possibility that the Fed decides to end its current money printing program after the year-end concerns are assuaged. If you remember back to the ends of QE 1 and QE 2, volatility lurched higher in their aftermaths.

"One of the things that we think is primarily responsible for buoying risk assets this year is the giant amount of liquidity that the Fed has injected into markets. The problem is what if they stop?" https://t.co/EsCa1h2Kec

— Jesse Felder (@jessefelder) December 5, 2019

And then there is the real possibility that something in the money markets has broken and the Fed simply doesn’t have the tools to fix it. Their current operations are nothing but a band-aid and aren’t sustainable. Should we get through year-end and the Fed be unable to end their current programs it’s hard to imagine the markets wouldn’t begin to sense that some sort of real trouble is brewing.

The Fed has actually made it very clear that their current operations aren’t QE, meaning they aren’t intend to try to boost the economy by creating a wealth effect. So far it seems market participants have refused to make the distinction. But if it becomes clear that the Fed is not pursuing policy at its discretion in order to boost the economy but because it is being forced to hold its finger in a leak in the dyke, confidence or complacency could quickly give way to panic.

"The big picture answer is that the repo market is broken. They are essentially medicating the market into submission. But this is not a long-term solution." –@biancoresearch https://t.co/SJMnKQv24x pic.twitter.com/ucUnfVs2r4

— Jesse Felder (@jessefelder) December 5, 2019

Finally, there is the issue of the unintended consequences of extreme, experimental monetary policy of the past decade. The build up of leverage across corporate America’s balance sheets is now well documented. In other words, it’s a narrative waiting for its tipping point. For now, investors are willing to dismiss the risks and all the warnings from pundits and central bankers alike.

However, there are signs that these latent risks could be in the process of becoming the problem so many have warned about. The lowest-rated junk bonds are seeing spreads begin to widen significantly. Trouble in leveraged loans is beginning to crop up, as well. Should the popular narrative evolve from the Fed propping up the markets to the Fed has created a systemic risk in doing so, investor confidence could swiftly evaporate.

"This is part of a much bigger issue: an increased amount of collateral damage and the unintended consequences of an excessive reliance on central bank liquidity." –@elerianm https://t.co/JrPL9HaOCE

— Jesse Felder (@jessefelder) November 30, 2019

Another rapid shift in investor confidence would see volatility rise at a time when all of the various short vol trades have become very crowded. The vicious cycle of buying volatility to cover, prompting volatility targeting strategies to sell equities pushing volatility even higher could do serious further damage to all of the narratives that have underpinned the current mania in the stock market.

Another steep selloff in stocks after the volmageddon of early-2018 and the waterfall decline late last year would do real damage to the idea that passive investors are entitled to historical rates of return and that the Fed has their backs. It might not take much more than that for the popular narrative of the financial crisis to make a comeback: the rampant greed encouraged by the monetary authorities is now facing its inevitable reckoning.

'A decade of easy money has left the world with a record $250 trillion of government, corporate and household debt. That’s almost three times global economic output and equates to about $32,500 for every man, woman and child on earth.' https://t.co/NV7tSD4D21 pic.twitter.com/f0CIyRPMgp

— Jesse Felder (@jessefelder) December 2, 2019

It certainly feels as if the overall market mood is ripe for a regime change in terms of the narratives underneath it all. The passive, FANG and QE narratives seem to ring hollow these days. That is, they just don’t seem to have the same appeal that they have had over the past few years. In fact, when you look at the Google Trends results in the chart at the top of this piece you’ll see they have all peaked and begun to rollover.

And, as Ned Davis pointed out last week, the recent market action certainly feels like a blow off top. Stocks have been “immune to negative headlines” and have gone straight up in a short period of time similar to the peaks in 2000 and 2007. In this case, it’s not fundamentals or even sentiment driving the rally anymore but the technical nature of the volatility feedback loop which can only last so long before it reverses into another vicious cycle.

'Given the high valuations I see, plus these divergences between many different indices, I am aware that many bull markets have ended with a rally similar to what we have seen since August.' –@NDR_Research https://t.co/yvqLSHZc3S pic.twitter.com/tXW7RNLQue

— Jesse Felder (@jessefelder) December 5, 2019

The vicious cycles of the past two years have been pretty short-lived as the larger narratives noted above were still very popular. But now that they are waning a new vicious cycle for volatility could be even more significant. It’s merely a question of whether investors still believe enough in them to dive back in and buy the dip in the event of another steep selloff. Of course, that goes for corporations and buybacks, too, but CEO confidence, as measured by the Conference Board, has already fallen to its lowest levels since the financial crisis.

If, indeed, the market narratives are shifting toward something less optimistic, then a new vicious cycle in volatility, a volmageddon part deux, could be the beginning of a much larger decline in stocks than anything we have seen over the past ten years. When extremes in investor sentiment paired with extreme valuations give way to a darker perception of reality it always coincides with a major decline in stock prices. And a blow up of the short vol trade could be the catalyst for just such a shift.

"What’s striking at present isn’t merely that the most reliable valuation measures now exceed the 1929 extremes but also that the psychology of investors so closely mirrors the 1929 view that these valuations represent a 'permanently high plateau.'" https://t.co/yNSlArMtDn pic.twitter.com/y0Y4rngZA2

— Jesse Felder (@jessefelder) December 4, 2019

Because if the short vol trade were to implode at a time when the Fed is already pumping tens of billions of dollars into the money markets it would call into question the Fed’s ability to support the markets at all. If $60 billion per month in treasury bill purchases and over $100 billion per day in overnight repo interventions isn’t enough to prop up stocks then what would it take? And can the Fed even afford to do that?

In all, it feels very much like we are nearing the end game for monetary policy and its perceived influence on the markets. The short vol trade represents the extreme leveraging of the Fed put and it’s gone so far that it may have outstripped the Fed’s ability to make good on it. Or perhaps, it has just stretched the credulity of the QE narrative too far. At some point, the idea that the Fed can prop up markets will seem hopelessly naive, as all bull market narratives do, well after the fact.

Don’t Fight The Fed: Buy Gold

The jobs report was released on Friday and the stock market celebrated the headline beat. Expectations were for 180,000 jobs to be created in the month of November while the actual number came in at 266,000. The unemployment rate fell to 3.5%, the lowest level since 1969.

The first thing to remember is that this is a lagging indicator of the economy that is regularly revised much lower only after a recession is identified, usually many months after it has already begun. The second thing to remember is that the headline usually obfuscates the underlying trends apparent only when you look below the surface.

A good looking jobs report, as yoy growth in education & health jobs rose to a 38-month high. The more cyclical component of nonfarm jobs growth – excluding those jobs – remains in a clear downswing, virtually unchanged from October’s 99-month low. pic.twitter.com/ivPIpu0raX

— Lakshman Achuthan (@businesscycle) December 6, 2019

As Lakshman points out above, the cyclical sectors of the economy are not doing so hot. In fact, a third of all the companies in the S&P 500 have reported earnings declines recently, a level only seen during recessions and bear markets.

'A third of S&P 500 companies have posted a yoy decline in earnings in 2019. The last times the share of companies posting contracting earnings was that high: 2009, 2008 and 2002, all periods when the broader economy plus the stock market were in decline.' https://t.co/amteVK8CJt

— Jesse Felder (@jessefelder) December 6, 2019

Most importantly, however, is the fact that with unemployment at its lowest levels in over half a century, the Fed is behaving as if we were already in the midst of the most painful recession in a generation.

The Fed hasn’t expanded its balance sheet at this rate since the financial crisis pic.twitter.com/R0zY5p9GKy

— THE LONG VIEW ⚫️ (@HayekAndKeynes) December 6, 2019

This is totally unprecedented and a clear sign that the Fed has chosen the “deep blue sea” (inflation) over the “devil” (an asset price bust). And, as discussed above, it may now get both.

'If the Fed adopts this so-called “make-up strategy”, it would mark the biggest shift in how it carries out its interest rate policy since it began to target 2 per cent inflation in 2012.' https://t.co/zNuNyNgkPo

— Jesse Felder (@jessefelder) December 2, 2019

As I’ve written for quite a while, there are all sorts of secular trends pointing to rising inflation going forward and extreme dovish Fed policy will only serve to exacerbate these.

"To say that we’ve not had inflation over the past decade is wrong, we just haven’t had inflation in places that are key components of the CPI basket. However, that may be changing." –@hkuppy https://t.co/jAiNINdq9c

— Jesse Felder (@jessefelder) December 5, 2019

I can’t emphasize enough the importance of the shift in perception, not just at the Fed but by pundits and politicians, that is leading people to believe that raising interest rates to head off inflation and reigning in deficits to preserve a sense of value for the currency is, “an extremely costly mistake.”

'As the economy continues to grow well above what once seemed like its potential, without inflation or other clear signs of overheating, it’s clearer that the old view of its potential was an extremely costly mistake.' https://t.co/4vYLMXNPdx pic.twitter.com/s2pnopz9nQ

— Jesse Felder (@jessefelder) December 6, 2019

In light of this, it would be reckless to assume we won’t see both rising inflation and rising deficits (thus a falling currency) going forward. There should be no question then as to why central banks around the world are buying the greatest share of gold production since the Nixon era.

Central banks have been buying nearly 20% of the world's gold supply, approaching the highest levels since the Nixon era, compared with being net sellers from 1971 through 2010: Bloomberg Intelligence's @mikemcglone11 pic.twitter.com/akT70puDRL

— Lisa Abramowicz (@lisaabramowicz1) December 6, 2019

This is the most important shift at the Fed since Paul Volcker was hell bent on breaking the back of inflation. Friday’s terrific headline jobs numbers, in the context of emergency monetary policy, only put an exclamation point on the fact that the Fed is now hell bent on stoking inflation. For this reason, the new “don’t fight the Fed” trade is not buying stocks or bonds or any other financial assets; it’s buying gold.