I used to love to read Richard Russell. In fact, he was one of the main inspirations for me in starting The Felder Report. He just had so much experience to draw upon that gave him an invaluable perspective towards the markets and he generously and voluminously shared those in The Dow Theory Letters, which he started in 1958 and published until he passed away just a few short years ago at the age of 91.

This is only the fifth year of existence for TFR but it feels much longer than that. Sometimes I think us market junkies age in dog years rather than human ones. I’ve been investing in the markets for over 25 years now (or 175 years in canine time). And I’m exactly halfway to 91 years of age so I barely have half the experience Russell did. Still, there are things in addition to the markets that at times make me feel old.

Having two adult children is one of those (and I guess Russell, who flew as a combat bombardier on a B-25 in World War II, would probably be proud of my son who enlisted in the Air Force a year ago). Another is just watching my favorite sport and seeing some of the kids of the players I used to idolize now taking over the NHL. My back also goes out from time to time these days; I broke several vertebrae in college and they never healed right. Sadly, mine is not quite as prescient as George Soros’ whose back pain has famously called several major turning points.

Recently, though, I was listening to a podcast with two of my friends that made me feel old. Toby Carlisle recently interviewed Eric Cinnamond; it’s a great discussion you should check out if you have the chance. Eric started talking about his memories from the peak of the dotcom mania and Toby wanted to dig into that because, as he said, there just aren’t many investors active today who were around back then.

That surprised me at first but after thinking about it must be true. When you consider how few of the hedge fund and mutual fund managers around back then are still active today and just how much money has shifted into passive products you realize that the markets are now being driven largely by managers and machines with no memory of that time. Those of us who do have a clear memory of it are in a distinct minority.

I remember it like it was yesterday. I was pretty green at the time, having only just started my professional career in early-1997, but I was instinctively cautious about joining the bandwagon focused on money-losing, high-flying internet stocks. It reminded me of a time in college when a few of my roommates got caught up in a pyramid scheme started by a small group of stars on the soccer team. The greed and excitement I saw during the mania reminded me of the very same greed and excitement my peers felt at school when they first put up $100 so they could recruit another dozen students to give them $100 each.

I remember it like it was yesterday. I was pretty green at the time, having only just started my professional career in early-1997, but I was instinctively cautious about joining the bandwagon focused on money-losing, high-flying internet stocks. It reminded me of a time in college when a few of my roommates got caught up in a pyramid scheme started by a small group of stars on the soccer team. The greed and excitement I saw during the mania reminded me of the very same greed and excitement my peers felt at school when they first put up $100 so they could recruit another dozen students to give them $100 each.

And while I don’t recognize that same sort of greed or excitement today there are just so many other things that feel so familiar right now and that hark back to that time. The prevalence of money-losing business plans was no greater then than it is today. The only difference is these companies have been funded by venture capital for far longer than they were back then. However, they are all now coming to market as venture investors get tired of funding massive cash burn.

WeWork, perhaps the poster child of the most recent rise in cash burning businesses, announced last week it was stepping up its IPO date to September. Like Uber, which came public earlier this year, it burns about $2 billion a year in a business model that is not profitable on an individual transaction level much less at scale. What’s more, its CEO and largest shareholder, decided to recently cash out to the tune of $700 million before the company even launches its IPO.

Looking just at the number of these sorts of companies, it’s very hard to decide whether there has been more misallocation of capital during the current cycle or during that previous one. But when you further consider the number of zombies that have been sustained by zero-percent interest rates and the amount of debt-financed buybacks enabled by the same and at the highest equity valuations in history its really no comparison. The malinvestment of the current cycle dwarfs anything we’ve ever seen before.

Maybe the most poignant of parallels between now and then, however, is the divergence between growth and value stocks. Investors back then were obviously smitten by the tech darlings of the day but in the process they left a number of terrific, old economy stocks for dead. There is not the extreme value that was available back then but because the over-valuation is so extreme and pervasive today, the relative undervaluation of certain sectors and styles is just as extreme as it was in 2000.

Ball Corp. was one of those bricks and mortar-type companies nobody wanted to own two decades ago. A maker of glass jars and aluminum cans was certainly not sexy enough to compete with pets.com and eToys.com. Ironically, the stock has risen almost 40-fold since then while both of those other companies are now long defunct. I don’t think I can come up with a better example of just how badly investors err when greed overcomes good sense.

Similarly, investors today paying 10-times sales or more for companies that have not yet been in existence for a decade are likely to discover that “investing” is far more complicated than paying any price whatsoever for something with good top line growth at the top of the cycle. On the flip side, those sectors and styles now out of favor likely offer some of the best opportunities to profit over the coming decade (real assets and equities tied to them).

I also distinctly remember buying Washington Mutual stock at a price-to-earnings multiple of five. A dowdy thrift whose profits were being squeezed by a flattened yield curve was just not appealing at all to any but the most die hard, contrarian investor at that time. Once again, the yield curve has flattened out completely creating opportunities in the financial sector. Like today, it was also dismissed at the time as an irrelevant economic signal.

Other signals, like the subtle widening of BBB spreads over the past 18 months or the divergence in the VIX discussed here in a blog post last week or the growing number of Hindenburg omens and the dramatic under-performance of small caps, are also being dismissed as irrelevant. Back then the argument was that the miracle of the internet meant these old signals didn’t mean much anymore. Today, the argument is the miracle of ultra-dovish monetary policy means they no longer hold any significance.

Other signals, like the subtle widening of BBB spreads over the past 18 months or the divergence in the VIX discussed here in a blog post last week or the growing number of Hindenburg omens and the dramatic under-performance of small caps, are also being dismissed as irrelevant. Back then the argument was that the miracle of the internet meant these old signals didn’t mean much anymore. Today, the argument is the miracle of ultra-dovish monetary policy means they no longer hold any significance.

Speaking of monetary policy, it is also interesting to note that from early-1997 to early-1999 oil prices fell from $25 to $10 a barrel, as a result of a rising dollar and the Asian economic crisis, putting a damper on headline inflation and allowing the Fed to maintain a relatively dovish policy. Oil prices then rebounded in 1999, almost quadrupling by late-2000. During that time, CPI ran from 1.5% in 1998 to 3.5% in 2000 forcing the Fed to tighten.

Our recent experience also echoes that earlier pattern. With oil prices crashing in 2014 and 2015, as a result of a surging dollar and rising supply created by fracking, the Fed was able to maintain its dovish policy under the cover of low inflationary pressures. Then, when oil prices rebounded from $26 a barrel in 2016 to $76 in 2018, inflation rose from 0% to 3% forcing the Fed to end its quantitative easing program and start raising interest rates.

These rate hike cycles, coming on the heels of a massive mis-allocation of capital driven by ultra-low interest rates, inevitably lead to a bursting of the asset bubble they engendered in the first place. By the time the Fed started cutting interest rates in early-2001 the bear market was already underway and there was little the Fed could do to reverse the shift in risk appetites. Once it becomes obvious to all that the jig is up it doesn’t matter if the band decides to play even louder. Nobody’s going to get back out on the dance floor again once they have already decided they’re exhausted and it’s time to go home.

Finally, the dovish policy adopted by the Fed starting in 2001 led to a breakout higher in the gold price that would go on to see the precious metal rise nearly seven-fold over the coming decade. Gold prices today have recently broken out of a long-term bottom once again as the central bank shifts from a tightening to a loosening of monetary policy.

As deficits widened during the recession of 2001-2002 to roughly 3.5% of GDP the dollar eventually rolled over into a deep bear market that provided additional fuel for precious metals prices. Today, we have only begun to sniff the possibility of recession and the federal deficit is already running at an annual rate of over 5% of GDP. A recession could easily see this number doubled. In this case, the bear market for the dollar that began in early-2017 would be renewed and could easily match the 30% decline in the greenback from 2001-2004.

The only glaring difference between then and now really is in the level investor euphoria. Or perhaps not the level so much as the form it has taken during the recent cycle. Back then there was a sense of a new gold rush, of a once-in-a-lifetime opportunity to get rich quick. Today, it’s very hard to argue this is the case. There’s just not that same level of greed and enthusiasm was saw back then. Those sorts of manias really only come around once in a half-century or so.

Then again, the Bitcoin bubble was clearly a euphoric, mass delusion very similar to the dotcom mania. And the fact that trillions of dollars of debt around the world trade at negative yields is another sort of euphoria. It’s a greater fool game at least on par with that of the internet bubble.

And, of course, there is another mass delusion at work right now. Trillions of dollars have flown into asset markets via passive products in a the firm belief that “the price you pay determines your rate of return” just doesn’t apply to them anymore. Investors clearly believe it doesn’t matter how high a price I pay, I should be entitled to the historic rate of return from owning these asset classes. This belief, despite all the evidence to the contrary, is proof of a suspension of rational thought in favor of following the crowd because, as JP Morgan so famously said, “Nothing obscures your financial judgment on investments more than the site of your neighbor getting rich.”

And this is really the true source of any speculative mania. It’s the inability of folks to sit it out and trust the very same common sense they use when buying a car or clothes or groceries while everyone else is joining the party and having such a good time in the process. In this way, the mania today is no different at all from that earlier one. In both cases it’s herding behavior and only from outside of the herd can you see the cliff up ahead. Those in the midst of it have only their neighbors’ blind optimism to guide them. Just because it’s ETFs rather than dotcom stocks doesn’t make it any more rational.

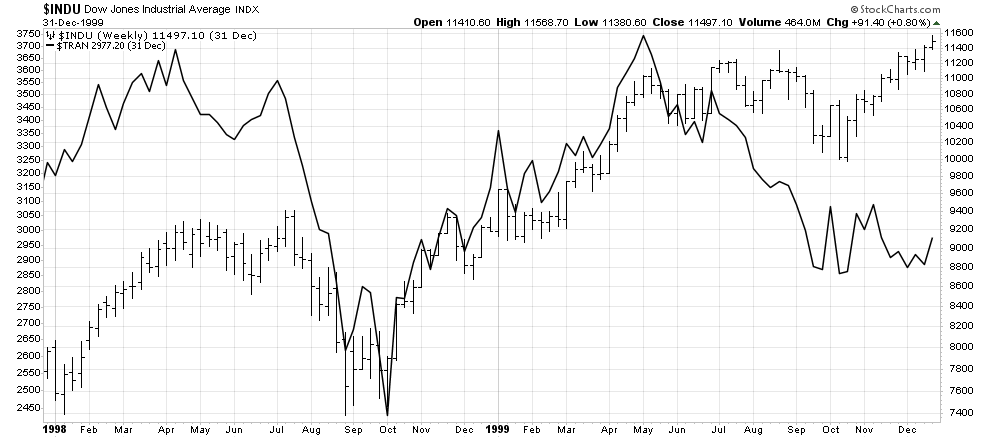

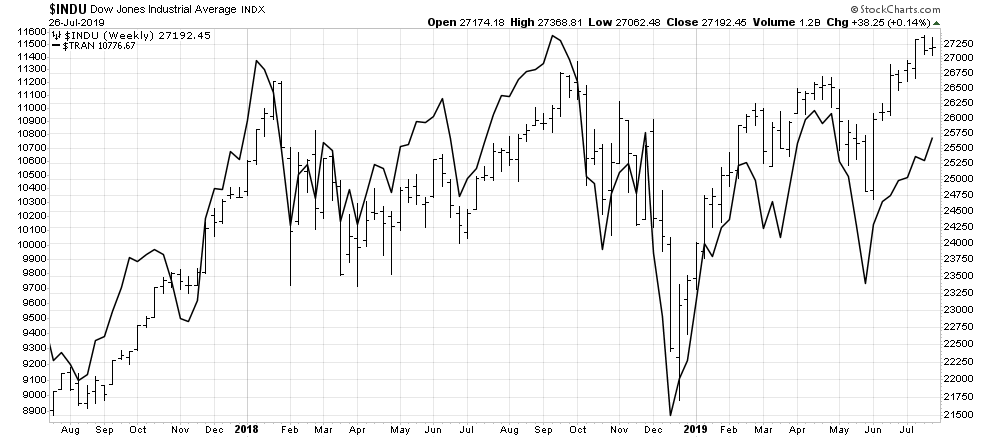

Obviously, I can’t speak for Richard Russell but it’s not hard to imagine what he would think of the current environment. The Dow Theory non-confirmation and its similarity to the one we saw back in January of 2000 is as plain as day to anyone who still pays attention to that sort of stuff (see the charts above). And the value of his perspective was not only in his intellect, humility and generosity but, most importantly, in his appreciation of market history.

When you have little experience it’s easy for some to believe the four most dangerous words in investing, according to Sir John Templeton: “this time is different.” However, when you see this mindset play out en masse several times in your career you begin to believe just the opposite and that, as Jesse Livermore said, “History repeats all the time in Wall Street.” This time is not different at all. In fact, in many ways it is a carbon copy of what we saw play out in the stock market 20 years ago. It’s just a shame that there are so few of us around to recognize it.