This post is based on excerpts from recent reports published at TFR Premium.

A couple of weeks ago, I wrote about how extreme valuations can be explained by extreme sentiment or euphoria. This week, I’d like to discuss the sort of euphoria we are witnessing in regards to owning equities today because it’s certainly very different than the sort of euphoria we saw at the peak of the dotcom mania, the last time valuations were as high as they are today. Back then, investors were making heroic assumptions about the prospects for growth in corporate sales and earnings. Today, they are making heroic assumptions about the sustainability of corporate profit margins and valuations, even if they’re not conscious of doing so.

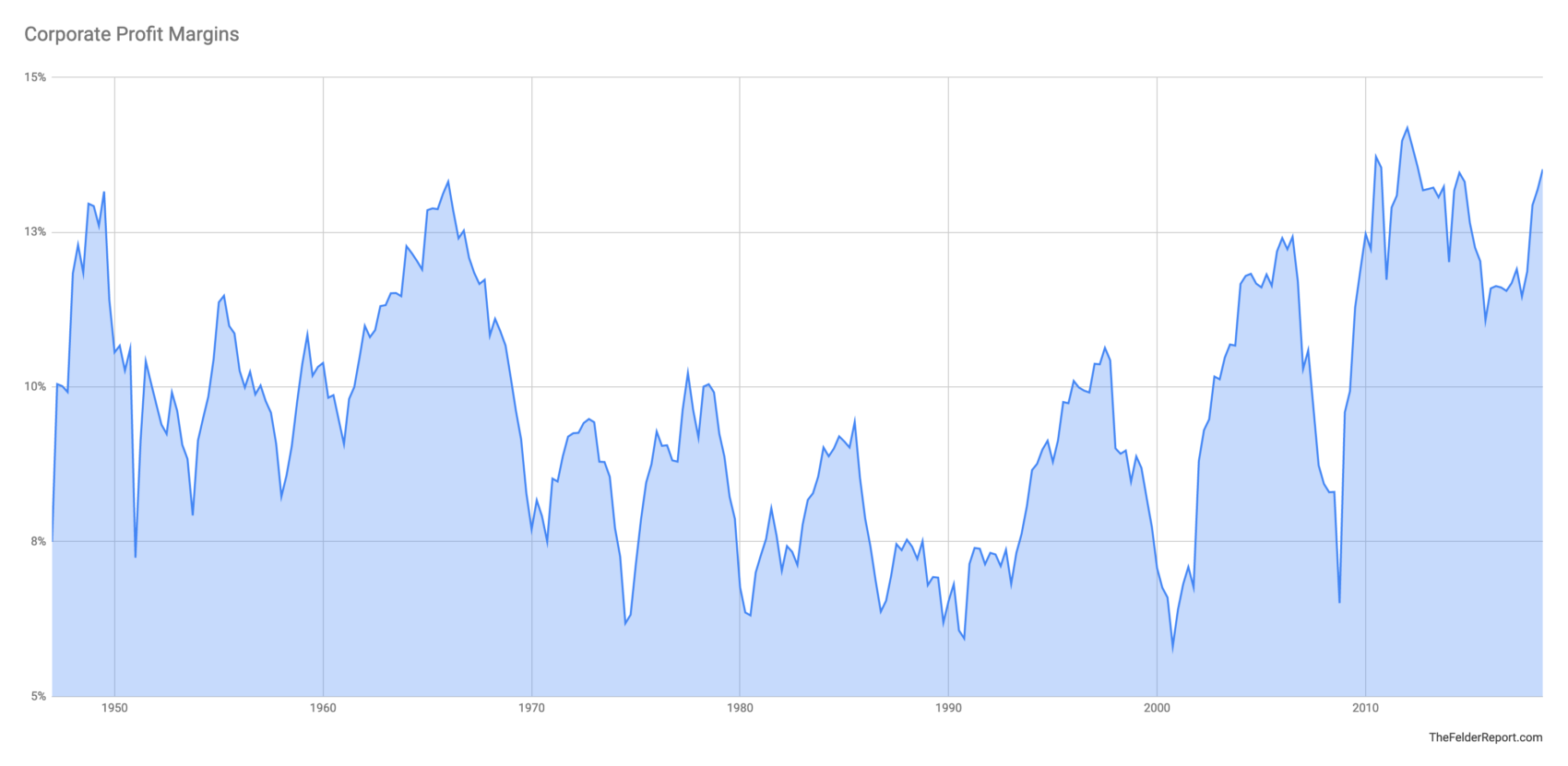

As noted in my last post, the Buffett Yardstick is near all-time highs. However, while earnings based measures still show the stock market to be expensive they suggest the over-valuation is less extreme. The difference is the former is not affected by profit margins and the later is entirely dependent upon them. Thus investors leaning on earnings-based measures like the price-to-earnings ratio are making the assumption that margins will at least maintain at their current record highs indefinitely, as euphoric a premise as I’ve ever seen.

This issue of profit margins is so critical because if earnings-based valuations were to simply return to their historical averages it would mean a substantial decline in prices. But if profit margins were to revert at the same time, it would mean a far more substantial decline. It works like this: trailing earnings for the S&P 500 are currently $130. Put a 15x multiple on that, the long-term historical average, and you get a price of 1,950 for the index, or 30% below the index’s current level. That would hurt but it really would not be so bad relative to the bear markets of the recent past. However, if profit margins were to fall from 13.5% today to 8% tomorrow earnings would fall to just $78. Put a 15x multiple on that and you’re looking at 1,170 on the index, roughly 60% below its current level. Ouch.

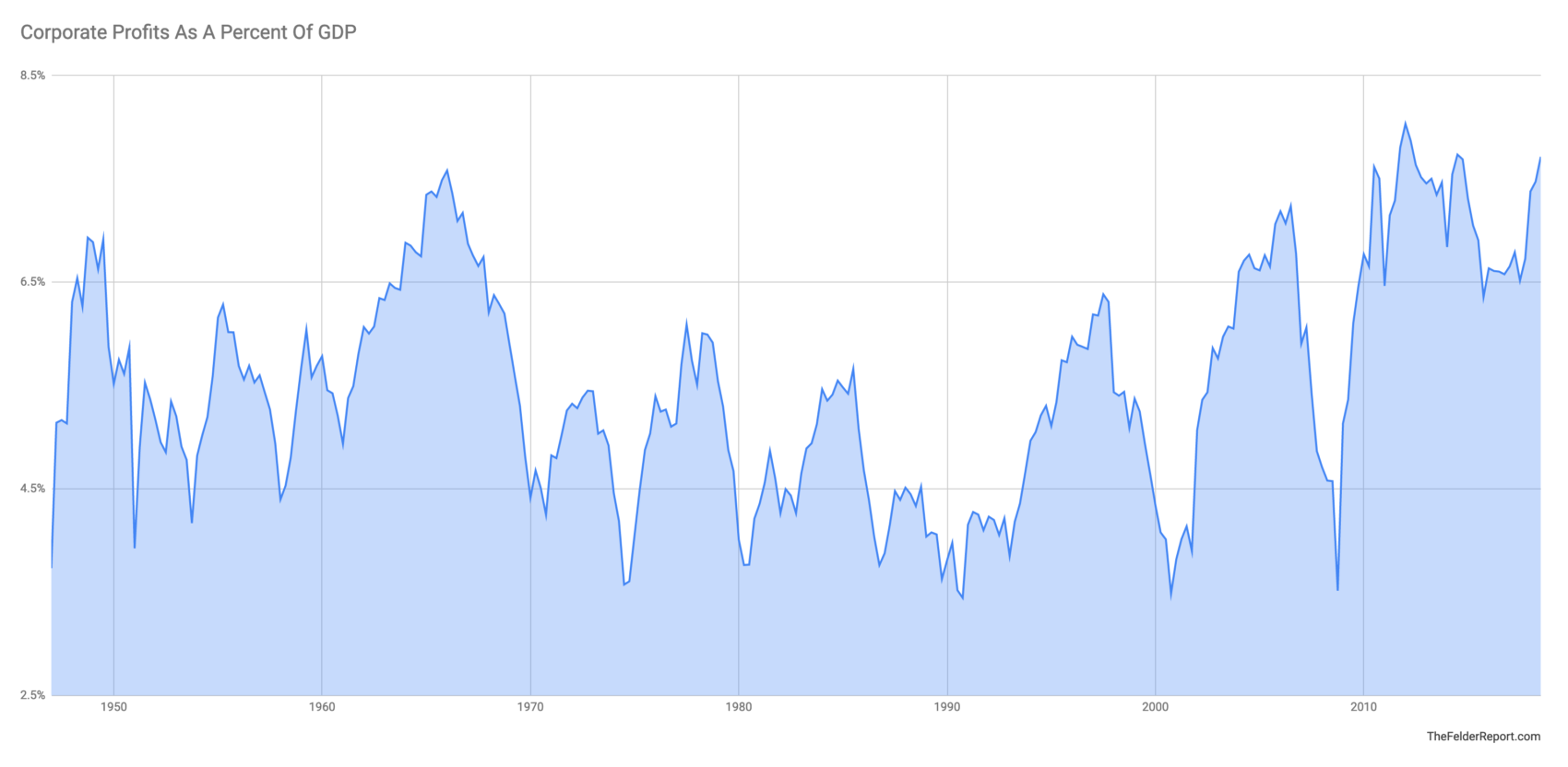

Recently, Ray Dalio came out and told CNBC that, ‘ignoring historical cycles is the No. 1 miscalculation many investors make.’ In other words, this embedded assumption regarding profit margins, that they are not cyclical on any time frame, is quite possibly the most dangerous mistake investors could make. What’s more, in Davos, Bob Prince, Dalio’s partner at Bridgewater, told Business Insider, “You’ve got a whole series of forces that are turning against corporations and profit margins. So your bigger risk is actually probably in the financial markets, rather than in the real economy.” What he’s referring to is something Warren Buffett wrote about 20 years ago:

In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems—and in my view a major reslicing of the pie just isn’t going to happen.

Clearly, Buffett was wrong and there was a major reslicing of the pie over the past couple of decades. He was right, however, in anticipating the political problems that would inevitably rise out of such an outcome and these are precisely what we are witnessing right now, not just here at home but around the world. As they continue to grow, these “political problems” represent a direct assault on profit margins and the euphoria that is responsible for the extreme valuations we are witnessing today. Investors would be wise to take notice.