“Even the most circumspect friend of the market would concede that the volume of brokers’ loans—of loans collateraled by the securities purchased on margin—is a good index of the volume of speculation.” -John Kenneth Galbraith, The Great Crash, 1929

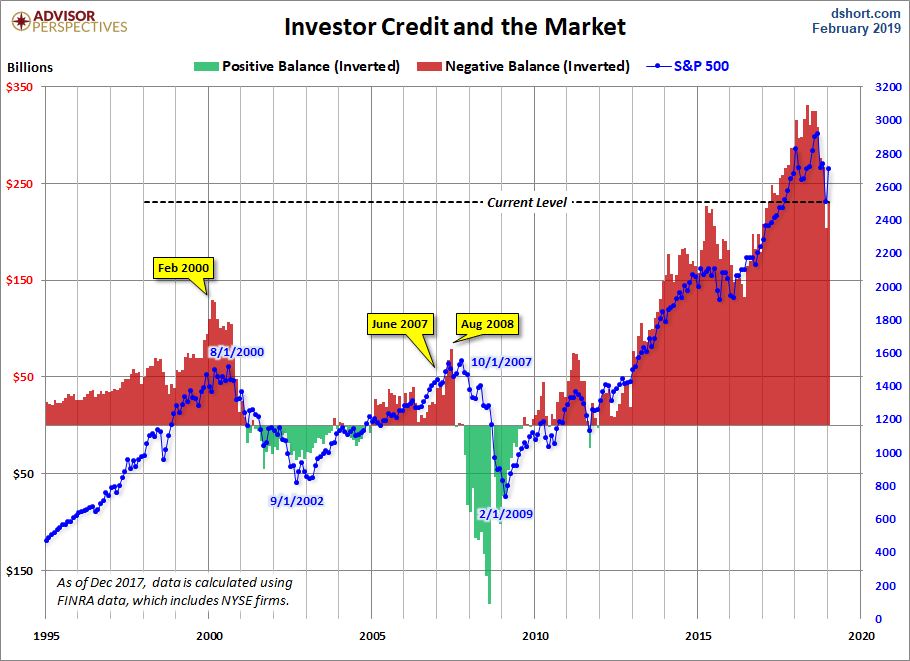

January margin debt figures were recently released (chart below via dshort.com) and almost immediately prominent pundits jumped to allay the natural concerns regarding the sheer amount of leveraged speculation in the market at present. Their common refrain has been to suggest that it’s not the amount that is important but its size in relation to the overall size of the market.

This sounds reassuring on its surface but, logically, it should be entirely unconvincing. Suggesting margin debt figures should only be compared to market capitalization is akin to suggesting a smoking habit should only be compared to body weight. In this case, the larger the human being, the less risk he or she would be taking in smoking three packs a day. A patient heeding this advice would then come to the conclusion that in order to ameliorate his smoking habit he should gain as much weight as possible. Of course, this is absurd.

“In accordance with the cultural practice, as the summer passed, the sound and responsible spokesmen decried not the increase in brokers’ loans, but those who insisted on attaching significance to this trend.” -John Kenneth Galbraith, The Great Crash, 1929

Just as absurd is to suggest that well over half-a-trillion-dollars in market leverage is less dangerous than it might appear due to the fact that the market itself is so highly valued. Along this line of thinking, the greater the bubble in equity valuations, the less problematic margin debt becomes. Like our smoker in the analogy above, investors believing this relationship should take more comfort in ever greater valuation extremes as it would mean less risk posed by financial leverage. Of course, this makes no sense at all.

Thus, what the rationalizing of margin debt in this way truly represents is the desire on behalf of those doing the rationalizing to find excuses for dismissing the rising risks posed by record leverage in the market, a psychological phenomenon as old as humans have been making markets.

“The time had come, as in all periods of speculation, when men sought not to be persuaded of the reality of things but to find excuses for escaping into the new world of fantasy.” -John Kenneth Galbraith, The Great Crash, 1929

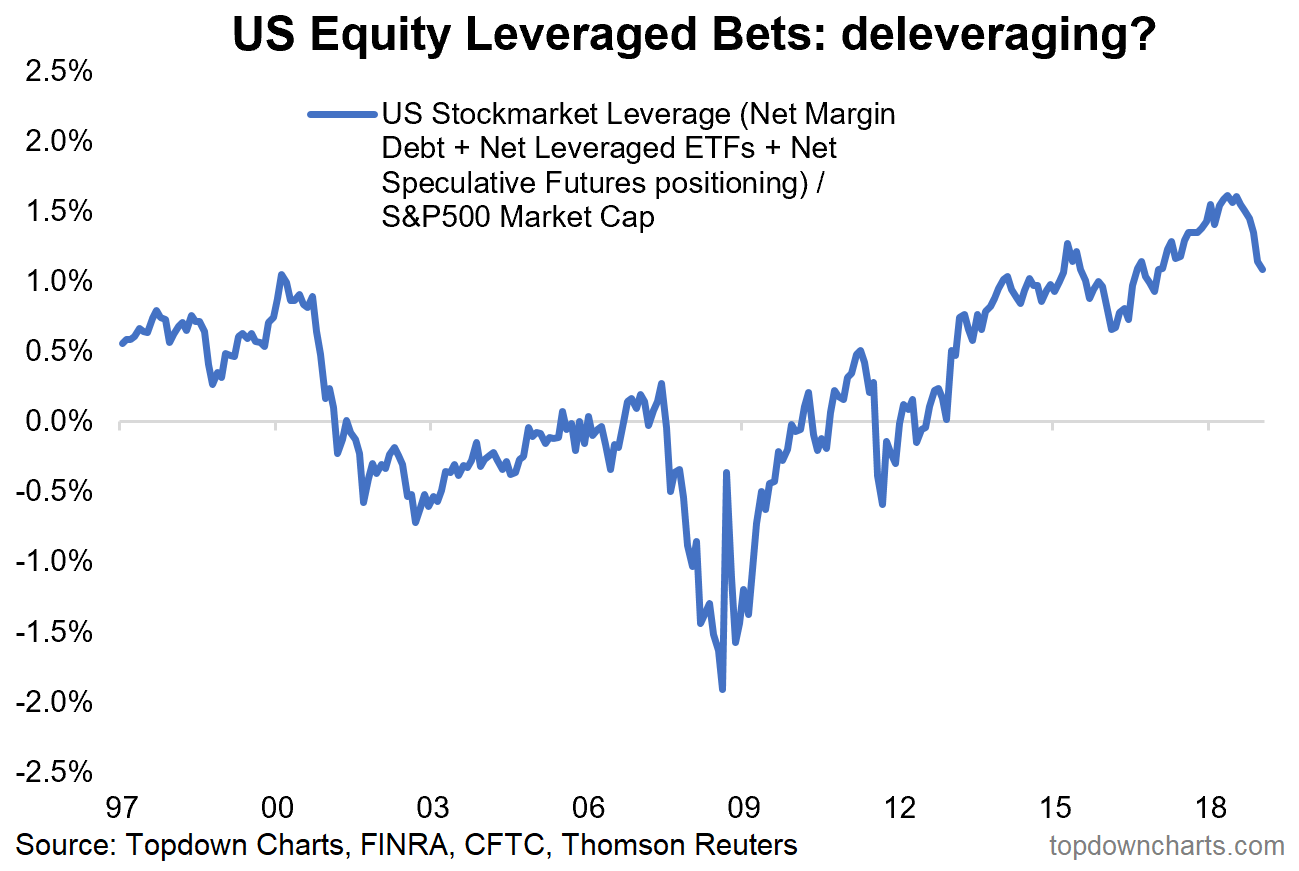

Still, for those who insist on relying on this patently illogical method, Top Down Charts has put together a composite of equity leverage in the market currently. As there are more leveraged vehicles in the market today than ever before, margin debt only provides one part of the whole. And even adjusted for the current extreme in market cap, total leverage is presently higher than it was a peak of the dotcom mania and far higher than where it stood leading into the financial crisis.

Unadjusted by market cap, it’s easy to see that total stock market leverage was recently about four times higher than that seen at the peak of the dotcom mania. To the extent this represents the volume of speculation, it’s hard to suggest investors have not become exceedingly euphoric about the prospects for equity prices and exceedingly dismissive of the risks.

As I have written many times, leverage simply represents the amount of potential supply to come into the markets should they fall far enough to trigger margin calls. History shows that excess leverage is always unwound in this way once prices stop rising.

“When prices stopped rising—when the supply of people who were buying for an increase was exhausted—then ownership on margin would become meaningless and everyone would want to sell. The market wouldn’t level out; it would fall precipitately.” -John Kenneth Galbraith, The Great Crash, 1929.

Right now, this potential supply, that would come to market by way of forced selling, is unprecedented. All told, the current state of stock market leverage, adjusted for inflation or the size of the economy, is unmatched since the Great Crash. And it doesn’t include asset-backed loans made by brokers, naked put selling strategies or the selling of volatility, all of which should be added to the leverage tally.

For these reasons, the volatility event a year ago and the precipitous decline of last December were very likely just a prelude of what’s to come when all these leveraged trades are inevitably forced to unwind. Furthermore, the current extreme in market cap, in relation to the size of the economy even greater than that seen at the peak in 1929, does nothing to ameliorate the risks posed by excessive leverage. Just the opposite.