“Half of the people can be part right all of the time

And some of the people can be all right part of the time

But all of the people can’t be all right all of the time.”

I think Abraham Lincoln said that.

“I’ll let you be in my dream if I can be in yours”

I said that.-Bob Dylan, Talkin’ World War III Blues

Futures positioning can be very informative at times. Not only does it represent sentiment for a given market, it shows actual positioning which can be much more valuable than the stuff of mere surveys. That said, I think we need to be very careful in how we use this stuff. Like everything else in the markets it requires second-level thinking.

For those in need of a refresher course, second-level thinking was summed up by Howard Marks in his book The Most Important Thing by saying, and I’m paraphrasing here, ‘to be successful you must hold nonconsensus views and you have to be right.’ Or, as I quoted in my report over the weekend, ‘it requires playing the player rather than playing the cards.’

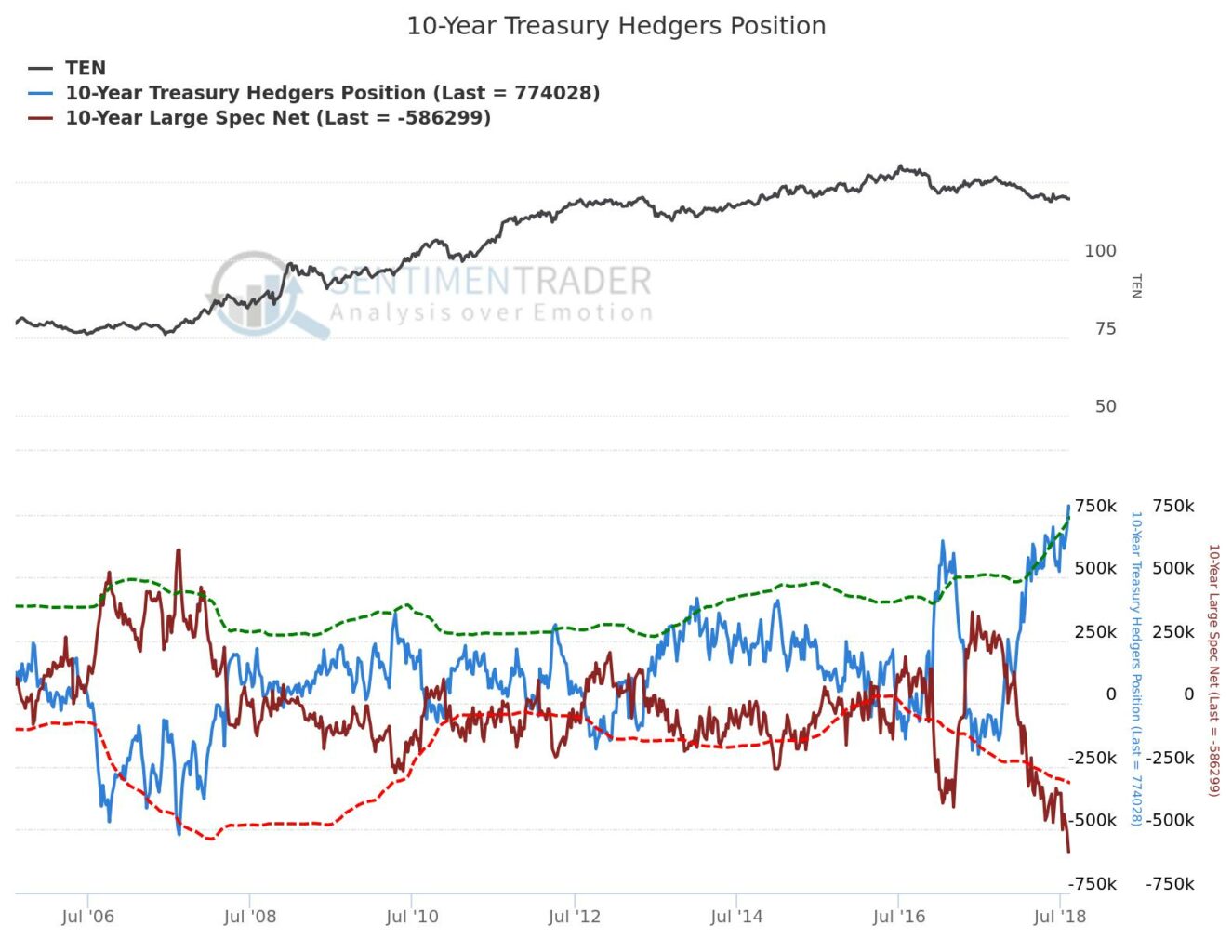

It is in this light that we should view futures positioning. Currently, there is much discussion regarding the massive net short position on the part of speculators in 10-year treasury futures. This would suggest that sentiment and positioning have become too bearish and that a large short squeeze could materialize. While this is possible I am surprised to see very little talk of the last time positioning was so extreme in the other direction.

Look back to the summer of 2007 and you’ll see speculators here got heavily long the 10-year treasury note via the futures market. That time they couldn’t have been more right and this proved to be a fantastic trade. The 10-year note rallied hard over the next couple of years kicking off a strong uptrend that really lasted until 2013. Who’s to say these traders, who were so prescient back then, won’t be proven right again this time on the short side?

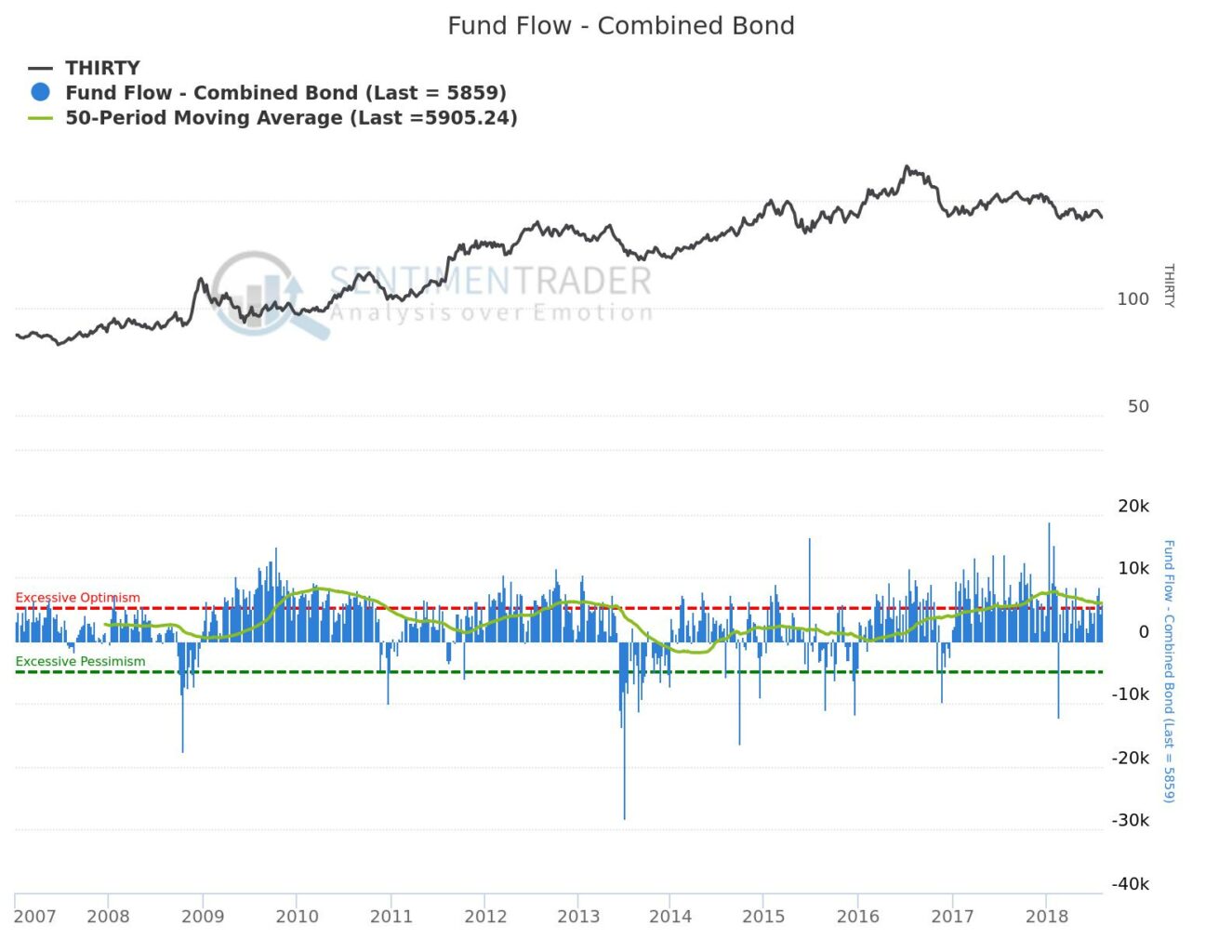

Really what we should be asking ourselves is this: Is short treasuries really the consensus trade so that long treasuries is the nonconsensus trade AND what are the fundamental signs that suggest treasuries should rally? The massive short position on the part of speculators in the 10-year treasury note futures market would suggest bond bearishness is the consensus but when we look at other indicators like fund flows in the bond market they just don’t jibe. In fact, there has been a tremendous inflow into bonds over the past 12 months which would suggest investors are bullish not bearish.

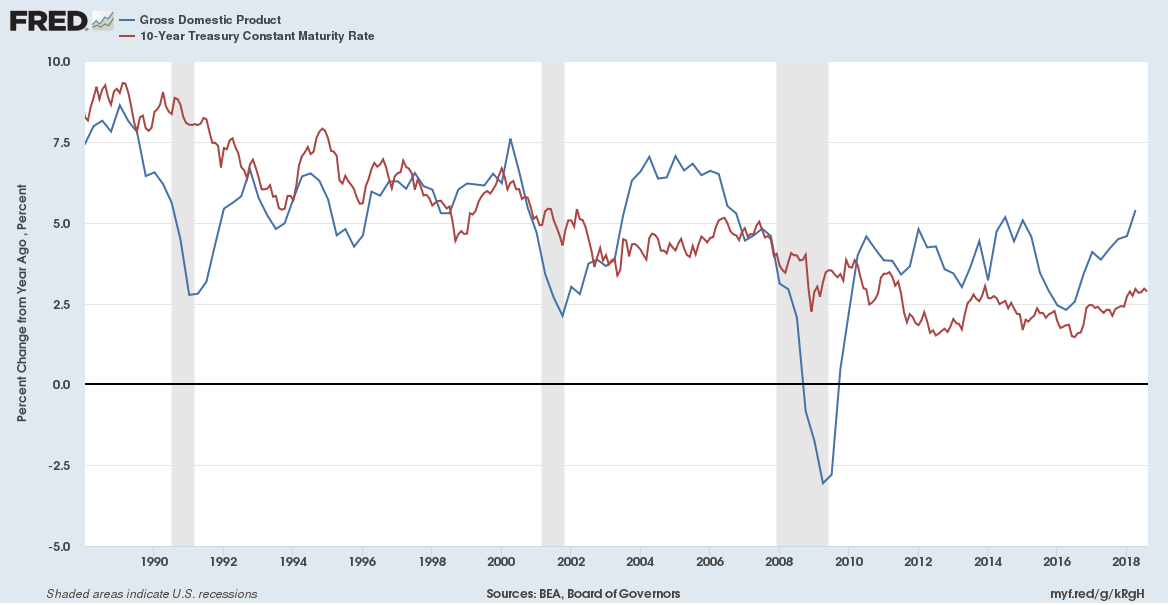

From a fundamental standpoint, the current run rate in nominal GDP would also suggest that the 10-year treasury note is significantly overvalued (the yield is unjustifiably low). In fact, with the highest nominal GDP print in a decade, we should probably be seeing the rate on the 10-yaer note somewhere around 4% if not 5% as Jamie Dimon suggested was possible last week.

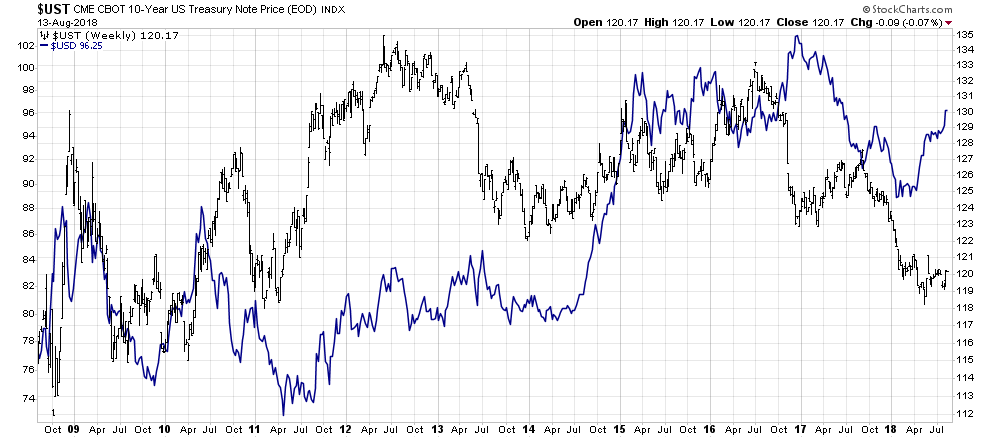

Finally, from a technical standpoint, it looks to me like bonds are in a long-term topping process. Of course, they could rally as part of a flight to safety should risk assets sell off but looking at the bigger picture, any rally that remains below 123 is clearly corrective. Even then any rally that stops short of 128 would be a lower low and do nothing to avert the current downtrend.

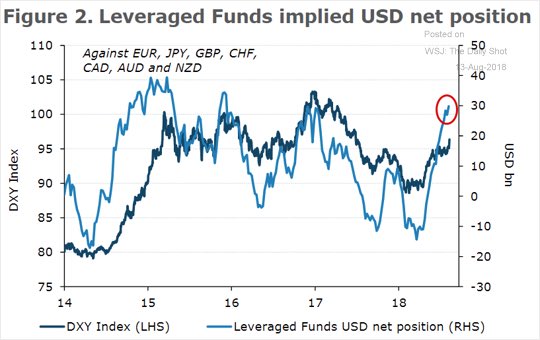

Really, it’s hard to evaluate the path of treasuries without viewing the asset class in the context of the dollar. These two typically move together with few exceptions. We had one major exception back in late-2106 after the election when the dollar strengthened and the t-note sold off. This resolved with the dollar playing catch down to the t-note. A similar situation is playing out currently and I expect a similar result.

The reason I think the dollar will fall back to meet bonds more than the other way around is that dollar positioning has become extreme again. In other words, the bullish dollar thesis has become consensus. When looking at positioning across all the major foreign currencies there have only been a handful of times over the past few years when traders have become so aggressively positioned for a higher dollar. Every time this has happened the dollar has reversed lower over the coming months.

At the same time, the long-term fundamentals point to a lower dollar. The widening fiscal deficit, projected to top $1 trillion next year, is very bearish for the greenback and if we enter recession at some point over the next year or two, as many anticipate, this will only worsen. We also have the massive disparity in central bank policy that has driven the dollar higher in recent years potentially reversing. Should the Fed be forced to even slow down the pace of its tightening campaign relative to the ECB and BOJ who will soon begin their own it would represent a massive one-two punch to the dollar, as well.

Technically, if I were a dollar bull I would be very worried about the fact that sentiment has become so extremely bullish despite worsening fundamentals and as the greenback has only been able to retrace 50% of losses over the past 18 months. Dollar bulls seem to be celebrating as if its just broke out to new highs when it is far from doing so.

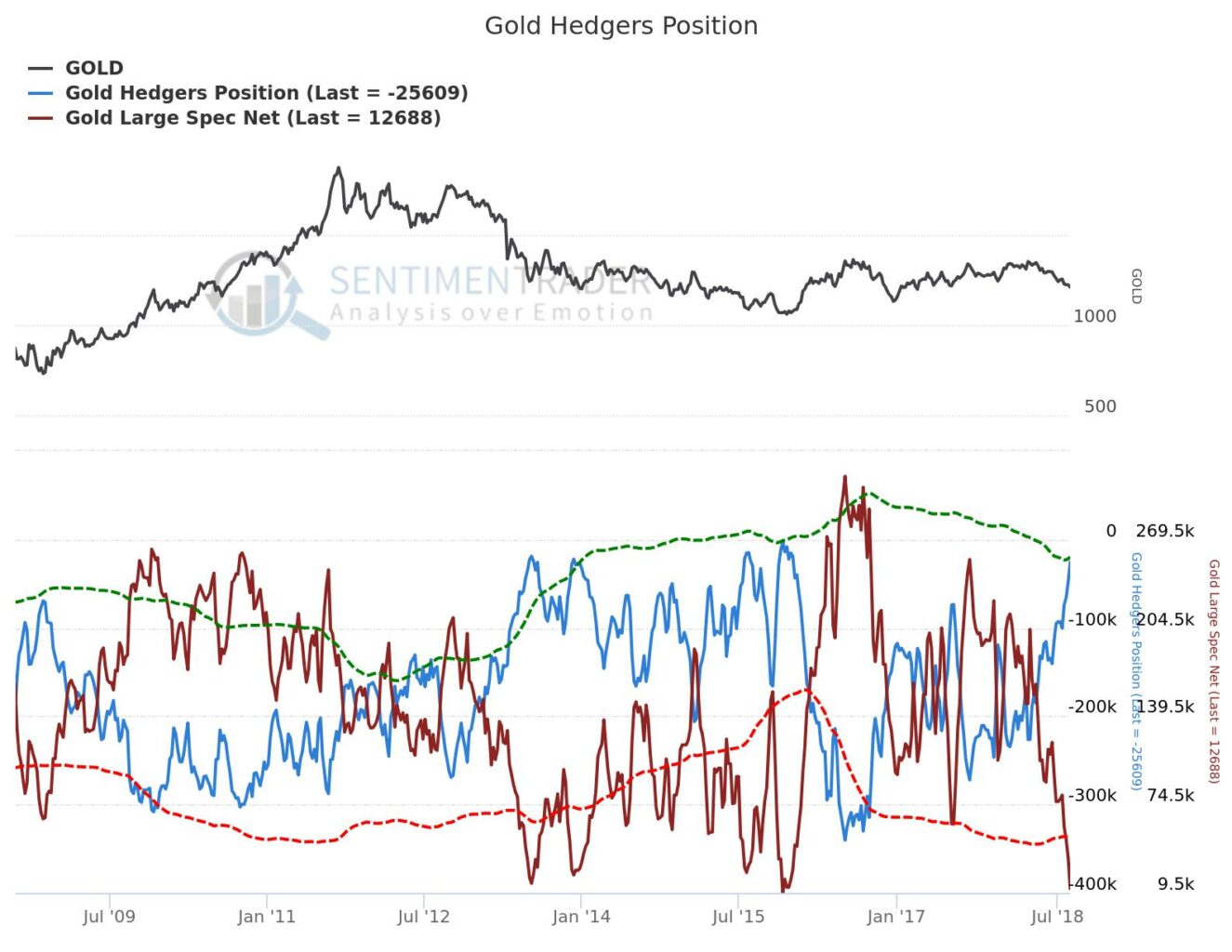

This brings me to one final related asset class: gold. Just like treasury notes, here speculators have built up the largest net short position in history. In this case, however, I believe there is, indeed, potential for a massive short squeeze.

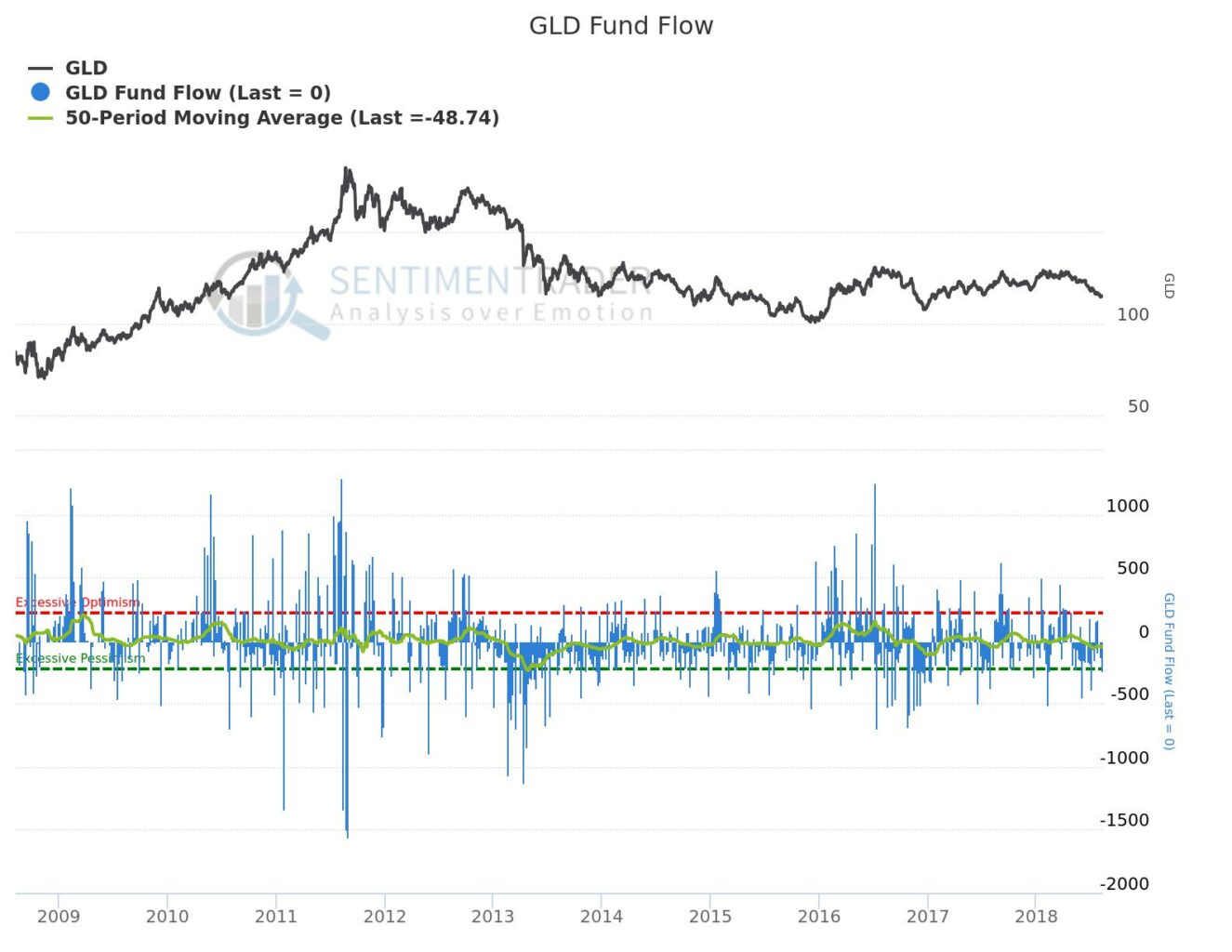

When we look at flows into the GLD ETF we can see that the message here actually does jibe with the message from the commitment of traders report. Unlike bonds, which have seen massive inflows lately, this ETF has seen steady outflows this year. Investors in both the futures and in the ETF are jumping ship and betting on lower prices pointing to a clear consensus trade.

Fundamentally, gold has become significantly undervalued over the past six months or so. As inflation has risen this year bond yields have not, a situation that should be very bullish for the gold price. Fundamentals like this don’t matter much in the short-term but should eventually lead to an explosive rally for gold, especially if inflation continues to rise as the Fed’s underlying inflation gauge suggests it will.

From a technical standpoint gold looks just the opposite of bonds, forming a rounding bottom as the latter forms a rounding top. In contrast to the situation in the dollar, it should be very encouraging to gold bulls that sentiment has become so bearish towards the precious metal even as it has only retraced 50% of its uptrend since the late-2015 low.

To recap, I don’t buy the idea that the true consensus is bearish bonds currently nor do I view the fundamentals there as being very bullish. To me, the consensus is complacency towards bonds and bullishness towards the dollar, a combination that could lead to a proving out of the bearish fundamentals for both. Conversely, the bearish consensus towards gold currently is a valuable contrarian indicator for an asset that appears undervalued amid a long-term bottoming process. At least this is my effort to play the player rather than the cards.