It seems everyone is talking about the yield curve right now. It also seems most economists and investors are quick to dismiss what would typically signal a clear economic warning as nothing worth worrying about. But from where I sit it looks like this could be a red flag worth paying close attention to.

The reason is that the yield curve, or the spread between the yield on the 10-year treasury and the 2-year treasury, appears to lead corporate spreads by about 30 months. In the chart below you’ll notice the close relationship which suggests rising risk aversion among corporate bond investors lags a flattening of the yield curve fairly consistently.

This could simply be due to the fact that a flattening curve is typically the product of rising short term interest rates which put pressure on corporate balance sheets. Investors possibly respond to this pressure with a lag only after it becomes readily apparent in their financial statements. It also could simply be the product of rising risk-free rates creating greater competition for risk assets.

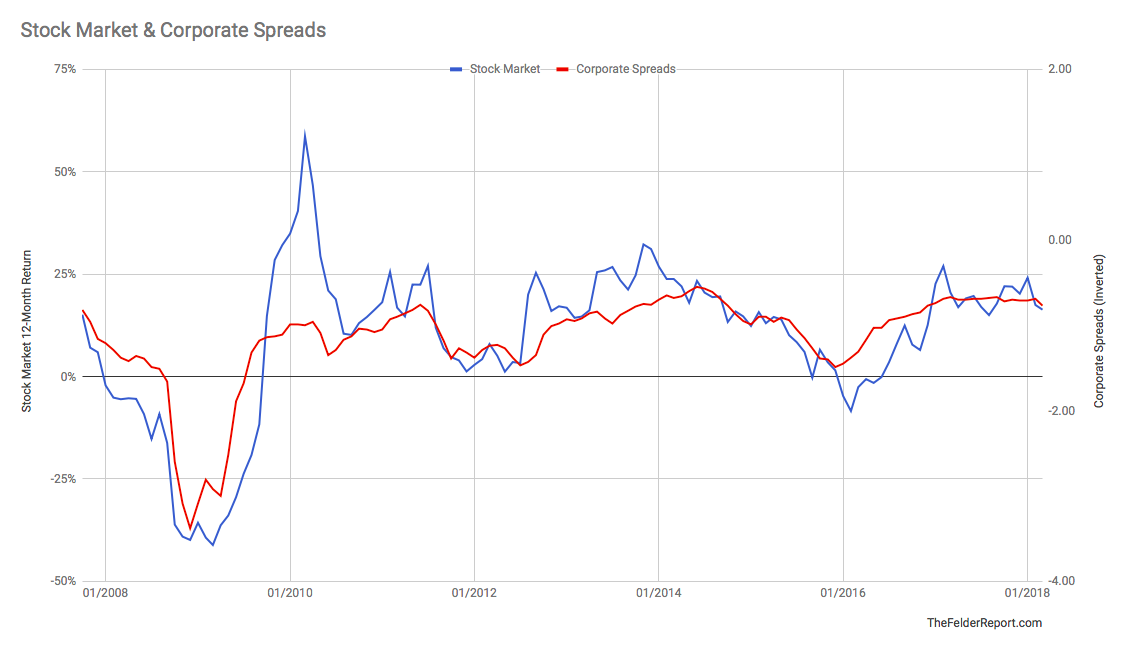

Either way, a flattening yield curve, especially when it comes by way of rapidly rising short term interest rates as it does now, creates a one-two punch for risk assets. This should be of concern not only to corporate bond investors but equity investors, as well, as there is a close relationship between risk appetites for both. Widening corporate spreads, especially over the past decade, have regularly been met with falling stock prices.

Because the degree of the recent flatting in the yield curve is the greatest we have seen since the financial crisis, it is reasonable to assume that over the next 30 months there is a risk for corporate spreads to widen to their greatest degree over that span, as well. If so, it’s hard to imagine it not coinciding with continued turbulence in the stock market if not a full-fledged bear market.