Many people and pundits, including none other than Warren Buffett, continue to insist that stocks look fairly priced relative to interest rates. For the moment I will ignore the fact that Mr. Buffett has repeatedly called the bond market a massive bubble thus using it as a benchmark to determine prudent prices for other assets is problematic at best. There are some simple ways, however, using Mr. Buffett’s own techniques to prove or disprove his thesis.

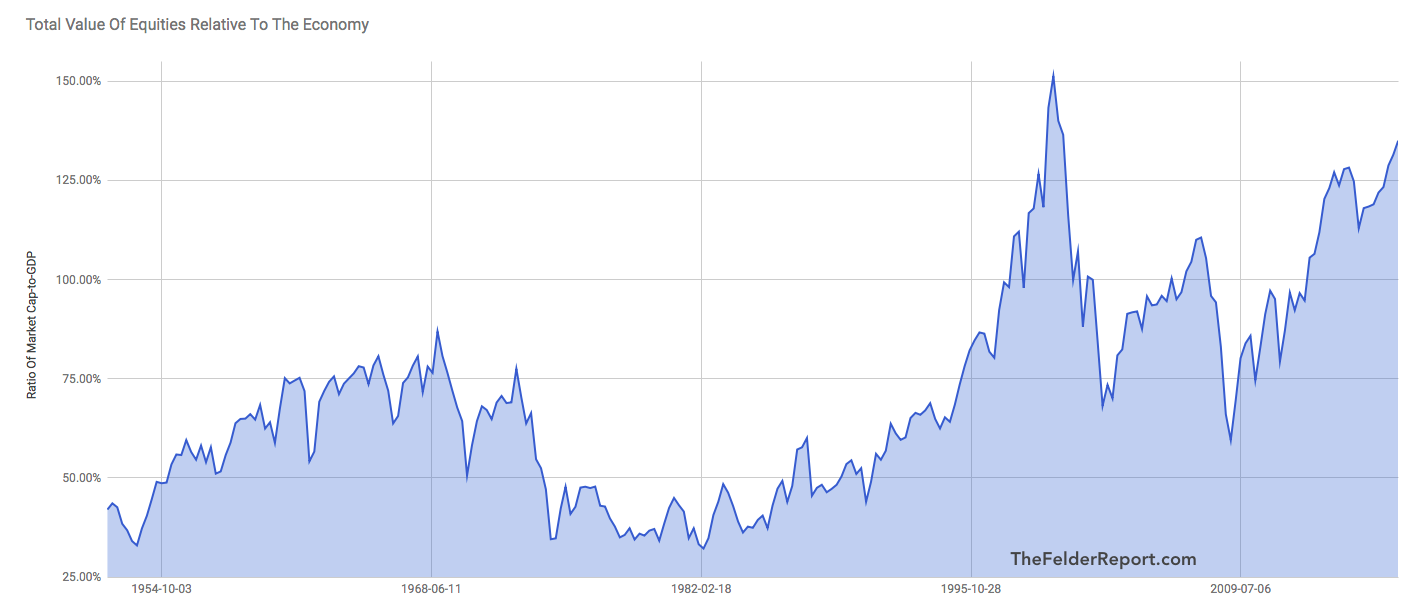

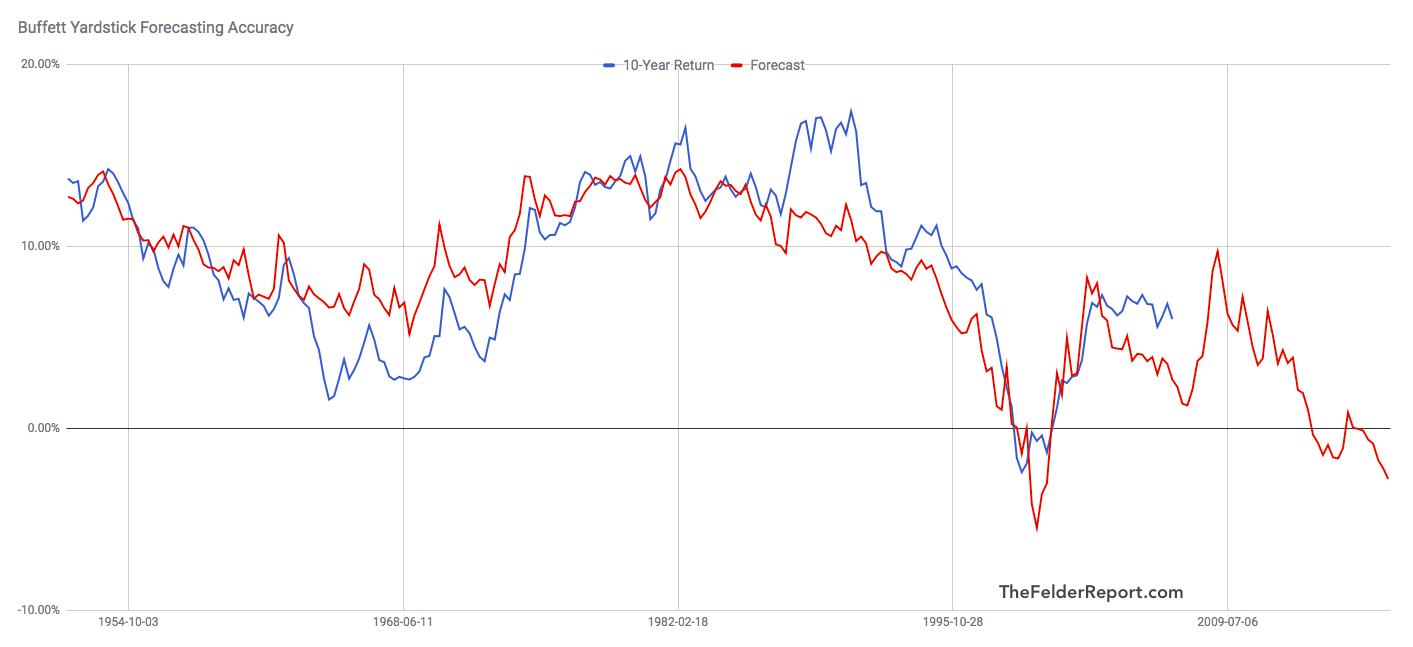

First, we must find a way to try to determine what sort of return stocks are likely to give us in the future. The Buffett Yardstick is not the best tool for forecasting future returns but it’s pretty good and since it’s Mr. Buffett’s thesis we’re testing we’ll use his measure. Currently, this valuation indicator sits just below the peak set during the dotcom bubble.

As Mr. Buffett has famously said, “the price you pay determines your rate of return.” Because investors are paying one of the highest prices in history, according to this measure, they are likely to experience some of the lowest future returns on record. In fact, this measure now suggests they will experience an average annual loss of 2.8% per year over the coming decade.

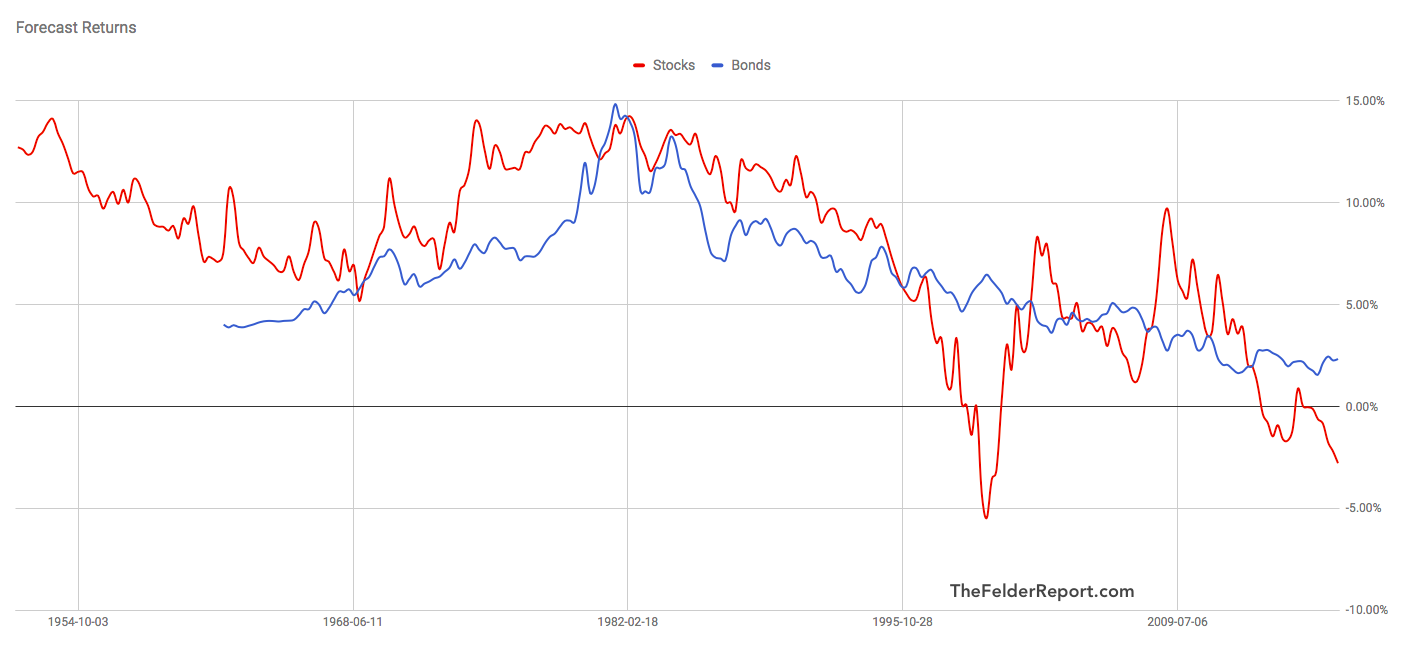

Now that we have an idea of what to expect from stocks we can compare it to the 10-year return offered by treasury bonds. The chart below shows the 10-year return forecast offered by stocks according to Mr. Buffett’s model against the 10-year treasury yield. With stocks offering a negative 2.8% annual returns and bonds yielding a positive 2.3%, the latter currently offer more than 5% greater prospective return. Only at the very peak of the dotcom bubble was this spread wider than it is today.

This comparative process is actually something Mr. Buffett has specifically recommended to investors in the past:

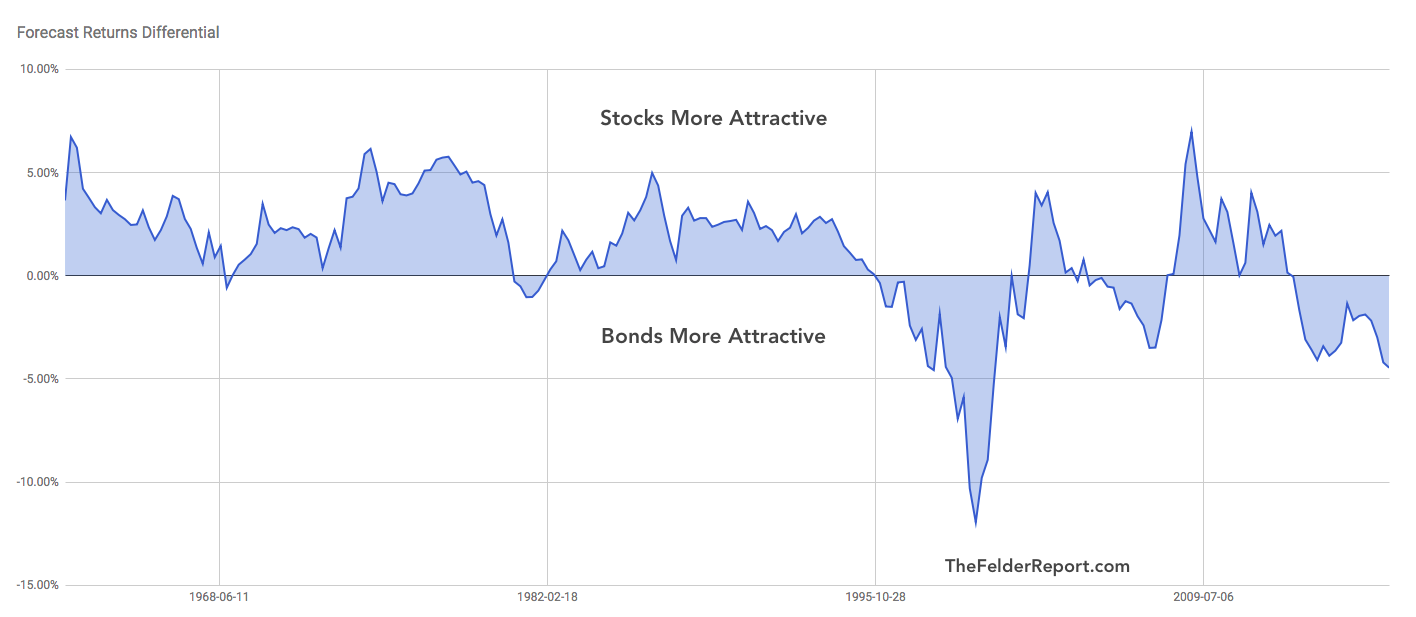

Though the value equation has usually shown equities to be cheaper than bonds, that result is not inevitable: When bonds are calculated to be the more attractive investment, they should be bought. -Warren Buffett, 1992 Berkshire Hathaway Chairman’s Letter

And here he’s right. For a very long time stocks were typically the more attractive investment. However, since he wrote this, the relationship has flipped and bonds have spent at least as much time on the attractive side of the ledger as stocks have.

And if you had shifted out of stocks and simply bought long bonds the last time this measure suggested they were as relatively attractive as they are today, I daresay you would have been very happy with the results. The chart below (created at portfoliovisualizer.com) tracks the performance $10,000 invested in the stock market versus the same amount put into long-term bonds on January 1, 2000:

So investors can continue to believe the fairy tale that stocks are attractive relative to bonds but they should know that’s what it is: a fairy tale. The truth is these are lowest interest rates in 5,000 years of financial history and even in comparison to that incredible statistic, stocks are extremely expensive. It could turn out that bonds fare poorly over the coming decade but, either way, stocks look very likely to fare even worse.