CF announced earnings last week and the stock rallied. This was more of a function of an improving outlook for the company than it’s actual first quarter earnings results. CEO, Tony Will, had this to say on the topic:

According to industry sources, Chinese urea exports were 1.2 million metric tons during the first quarter compared to 3 million metric tons during the first quarter of 2016. We continue to expect 5 million to 6 million metric tons of exports from China for the full year 2017, which is down significantly from recent years. At the same time, the number of new capacity expansion projects being initiated around the globe has slowed dramatically. We continue to project the rate of net new capacity growth after this year and for the foreseeable future to be well below the normal annual demand growth rate of 2%, as is illustrated on pages 15 through 18 of our materials. Therefore, we expect the global supply and demand balance to tighten over the next few years, leading to industry recovery.

The bottom line is CF has managed well through the downturn in the industry. It now looks like things are starting to improve from a supply/demand viewpoint. This is why the stock was upgraded on Friday by UBS:

CF Industries is upgraded to Buy from Neutral with a $33 price target at UBS, which views CF as a top pick to play the eventual agricultural recovery and with a secure dividend as cash flow improves. UBS sees 2017 as a transition year from a cash flow negative in 2016 to an estimated ~9% free cash flow yield in 2018, as U.S. natural gas prices should remain relatively low while oil prices rise over time, which should widen the cost advantage to CF. The firm thinks CF should be valued at a peak multiple of ~9.5x on its 2018 EBITDA estimate based on the longer term natural gas advantage and its belief that nitrogen fertilizer prices are bottoming.

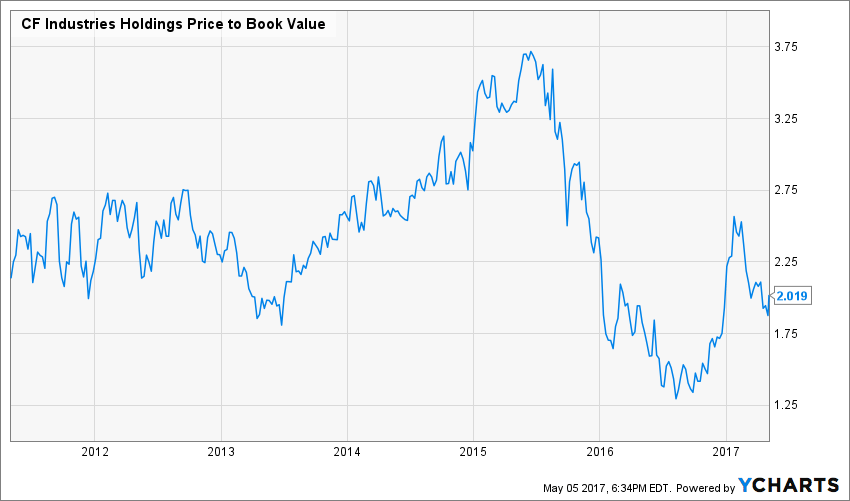

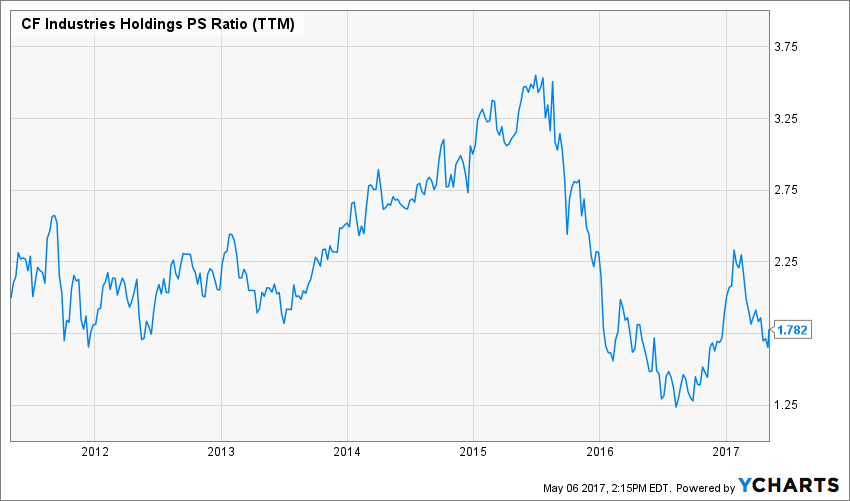

Personally, I think the stock today is worth at least $35 per share based on its historical valuations (price-to-book value and price-to-sales):

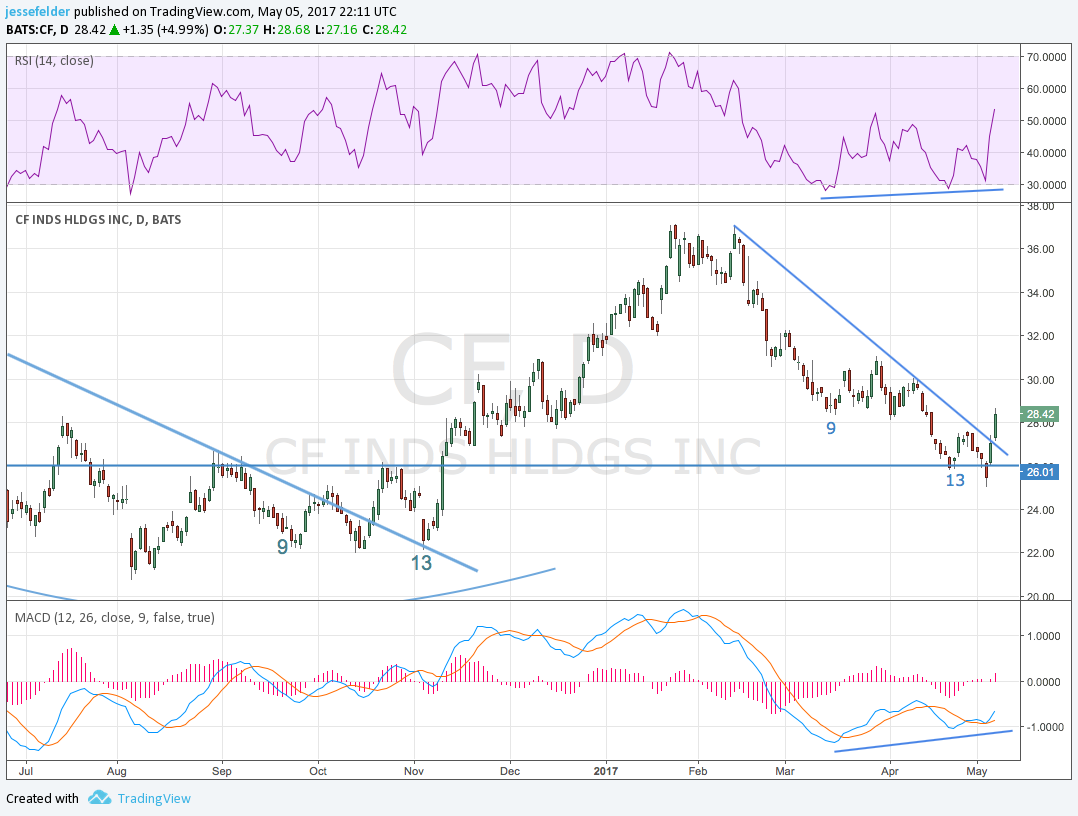

However, the upside could be much greater if pricing for the company’s products improves over the next year or two. And this is really what the technicals are saying right now. The stock bounced hard off of key support after completing a DeMark Sequential buy signal on the daily chart.

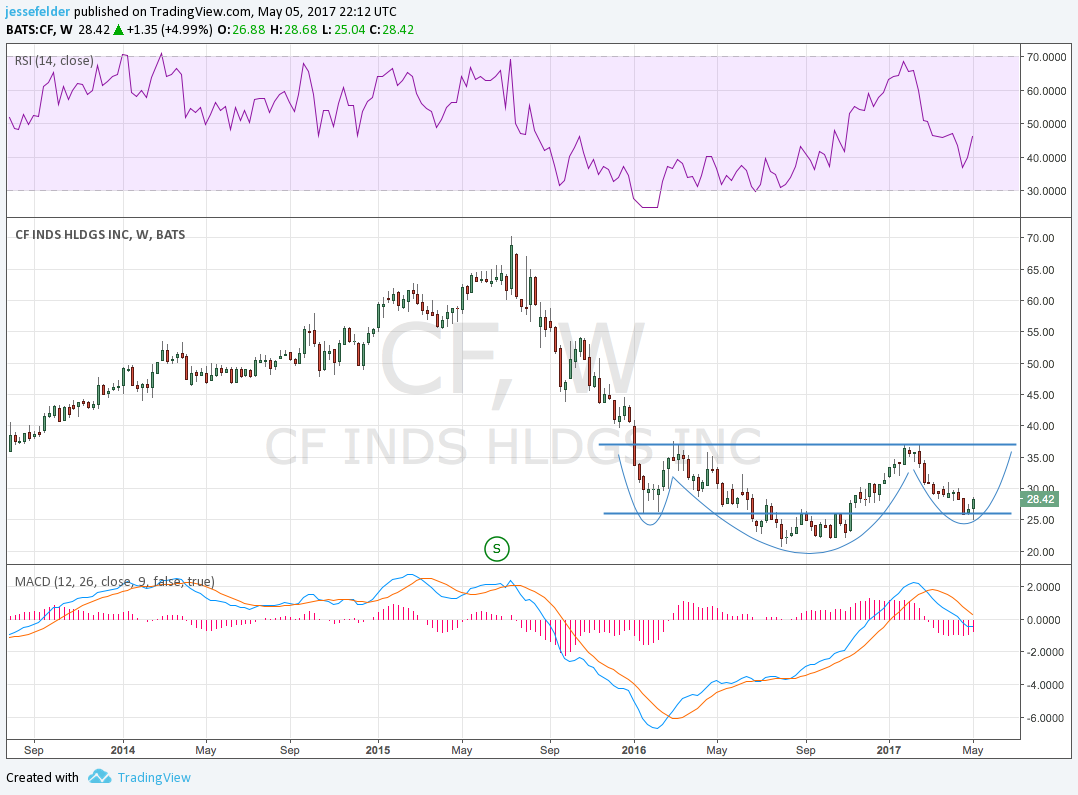

Longer-term the stock appears to be forming a textbook head and shoulders bottom pattern. If this plays out, it would setup a projection north of $50. And if the company can generate cash flows similar to what they did just a couple of years ago, this target may actually prove conservative. These are some big “ifs” but I believe the risk/reward equation here is still very favorable.

Insiders haven’t bought more stock after the flurry we saw about a year ago. Still, they are exercising options and holding onto those shares which is bullish in my view.

Ultimately, both the fundamentals and technicals are pointing higher for the stock right now. We’ll just have to see how things continue to develop over the next few quarters.