“Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” -John Templeton

‘If John Templeton is right, what is “euphoria” and how do we know when it has taken hold of investors?’ This is a very good question a reader asked me this week though I think it’s not very difficult to answer for those of us who have now seen several bubbles over the past couple of decades.

For me, personally, the first thing that comes to mind when I think of the word “euphoria” the local record store when I was a kid. I don’t know how much conscious thought they actually put into naming the place when the first opened it but it was appropriately done. It was decorated with tie-dyed t-shirts and perpetually had incense burning. It was a haven for psychedelia in the mid-1980’s after pop culture had passed it by.

The idea of psychedelia really gets to what euphoria is really all about: an altered state of consciousness marked by elevated mood. Now, I’m sure there of those out there who would be eager to argue that psychedelics actually help us see reality as it is and that our normal state of consciousness is less real than we believe it to be. I’m not going to debate this point. I just want to point out that euphoria is essentially the goal of psychedelic activities.

Psychologists define euphoria in similar fashion: “Euphoria is an elevated state of mood and happiness not reflecting the reality of the situation.”

And here is where we can start to imagine the term “euphoria” in a financial sense. When investors begin to feel optimism that is far beyond that which is justified by reality they have technically become euphoric. It was witnessing this very dynamic during the dotcom bubble that I believe inspired Warren Buffett to deliver his now-famous warning in 1999:

Today, staring fixedly back at the road they just traveled, most investors have rosy expectations. A Paine Webber and Gallup Organization survey released in July shows that the least experienced investors–those who have invested for less than five years–expect annual returns over the next ten years of 22.6%. Even those who have invested for more than 20 years are expecting 12.9%.

Now, I’d like to argue that we can’t come even remotely close to that 12.9%, and make my case by examining the key value-determining factors. Today, if an investor is to achieve juicy profits in the market over ten years or 17 or 20, one or more of three things must happen. I’ll delay talking about the last of them for a bit, but here are the first two:

(1) Interest rates must fall further. If government interest rates, now at a level of about 6%, were to fall to 3%, that factor alone would come close to doubling the value of common stocks. Incidentally, if you think interest rates are going to do that–or fall to the 1% that Japan has experienced–you should head for where you can really make a bundle: bond options.

(2) Corporate profitability in relation to GDP must rise. You know, someone once told me that New York has more lawyers than people. I think that’s the same fellow who thinks profits will become larger than GDP. When you begin to expect the growth of a component factor to forever outpace that of the aggregate, you get into certain mathematical problems. In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems–and in my view a major reslicing of the pie just isn’t going to happen.

So where do some reasonable assumptions lead us? Let’s say that GDP grows at an average 5% a year–3% real growth, which is pretty darn good, plus 2% inflation. If GDP grows at 5%, and you don’t have some help from interest rates, the aggregate value of equities is not going to grow a whole lot more. Yes, you can add on a bit of return from dividends. But with stocks selling where they are today, the importance of dividends to total return is way down from what it used to be. Nor can investors expect to score because companies are busy boosting their per-share earnings by buying in their stock. The offset here is that the companies are just about as busy issuing new stock, both through primary offerings and those ever present stock options.

So I come back to my postulation of 5% growth in GDP and remind you that it is a limiting factor in the returns you’re going to get: You cannot expect to forever realize a 12% annual increase–much less 22%–in the valuation of American business if its profitability is growing only at 5%. The inescapable fact is that the value of an asset, whatever its character, cannot over the long term grow faster than its earnings do.

The two things that are different today than they were when Buffett wrote the piece above are: interest rates now are much lower and the expectation of 5% GDP growth is far more optimistic than it was back then. In other words, the factors that might help investors achieve these higher returns, falling interest rates or rising economic growth, are even more skewed negatively then they were 17 years ago.

What remains the same today is corporate profitability is at least as elevated as it was back then as are valuations. For these reasons, the best investors can expect to earn is the rate of earnings growth. I believe Mr. Buffett was actually pretty optimistic in assuming this should match GDP growth, however. And the 10-year return subsequent to his writing bares this out. Stocks did nowhere near 5% per year from November 1999 to November 2009.

As I wrote recently, the long-term compound annual growth rate of corporate earnings is 3.78%, according to Robert Shiller’s data. Compare this to CAGR of 6.43% in GDP and you’re left with a massive gap. Earnings just don’t keep pace with the overall economy. Rob Arnott discussed this in a paper titled, “What risk premium is ‘normal’?“:

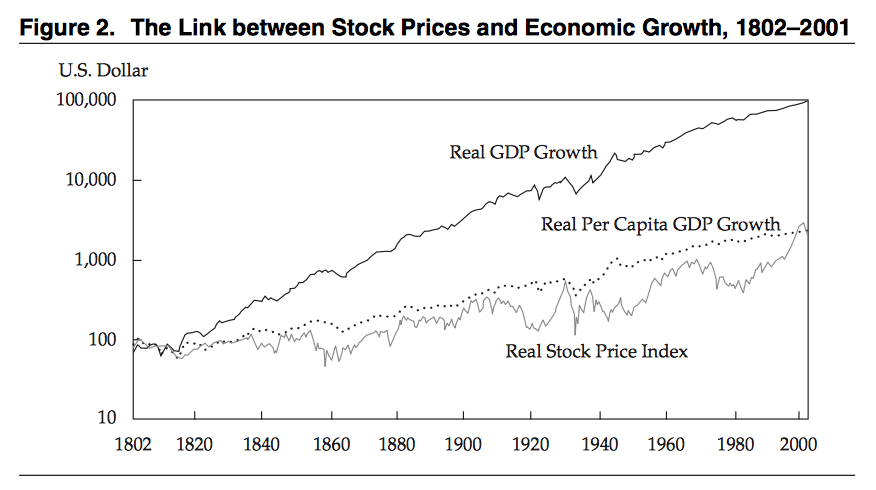

Figure 2 allows a closer look at the link between equity price appreciation and economic growth. It shows that the growth in share prices is much more closely tied to the growth in real per capita GDP (or GNP) than to growth in real GDP per se. The solid line shows that, compounding at about 4 percent in the 1800s and 3 percent in the 1900s, the economy itself delivered an impressive 1,000-fold growth. But net of inflation and dividend distributions, stock prices (the same “Real Stock Price Index” line in Figure 1) fell far behind, with cumulative real price appreciation barely 1/50 as large as the real growth in the economy itself.

Over the past 70 years real GDP per capita has grown at a compound average growth rate of 1.9%. Over the past decade it’s managed just 0.5%. Take your pick of either number and this is the most investors should realistically expect stocks to generate over the coming decade.

Furthermore, this expectation includes several important assumptions, as Mr. Buffett points out. First, interest rates must remain at their lowest levels in 5,000 years or move even lower. Next, corporate profit margins must remain near record high levels in relation to GDP. Finally, valuations must have found a new, permanently high plateau. In my view, each one of these assumptions is dangerous in its own way.

As I have written many times before, valuations alone provide a very good idea of what we can expect from stocks over the coming decade. Buffett wrote about this a couple of years after his original piece:

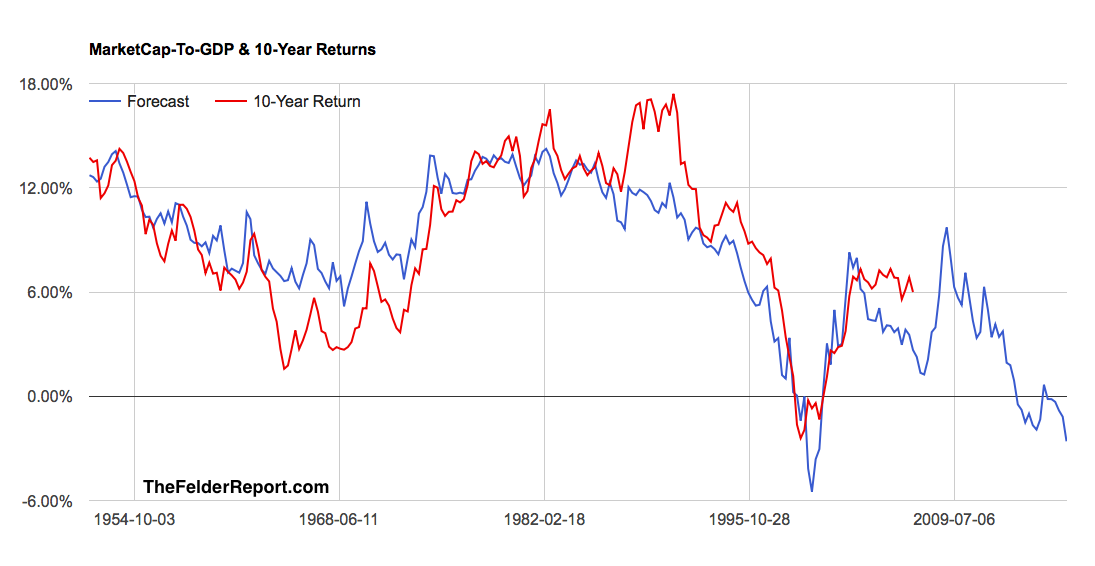

On a macro basis, quantification doesn’t have to be complicated at all. Below is a chart, starting almost 80 years ago and really quite fundamental in what it says. The chart shows the market value of all publicly traded securities as a percentage of the country’s business–that is, as a percentage of GNP. The ratio has certain limitations in telling you what you need to know. Still, it is probably the best single measure of where valuations stand at any given moment.

The chart above is my own and I have added the forward 10-year returns for stocks on top of the market cap-to-GDP ratio Buffett refers to. Today, this chart suggests the average annual return over the next decade is very likely to be negative. Note that this is total return, including dividends, not just change in principal.

Now compare how this 2% best case scenario and the perhaps more likely negative 2% scenario compares to current expectations. Like 1999, investors once again expect returns that are far beyond what is justified by history let alone that which can be reasonably extrapolated from valuations. The most recent poll from Natixis shows investors expect to achieve 8.5% per year after fees and inflation from a diversified portfolio over the next decade. As Jason Zweig notes, this would require stocks to do at least 15% per year.

Millenial investors have even more outrageous expectations. They believe they will capture 13.7% per year (11.7% after 2% inflation) from a diversified portfolio that includes an allocation to equities of just 30% and a whopping cash position of 25% (with the balance in bonds and alternatives)! Go figure what the implied returns from equities must be in that case to achieve 13.7% on the overall portfolio. I can tell you it’s far north of 22.6% per year. And when asked if this sounds reasonable some reply in the affirmative without batting an eye.

“Euphoria” in today’s market, then, is very similar to that which we saw during the height of the dotcom mania. It’s simply a function of investor expectations that are wildly more optimistic than can be justified by any rational analysis. Because interest rates and potential GDP are so much lower today than they were back then it’s not hard to argue that the euphoria among investors might even be greater today.

Many claim that we have not reached the point of euphoria yet in the asset markets because investors aren’t frothing at the mouth for dotcom stocks or residential real estate like they were during those previous bubbles. I would simply suggest in reply that history does not repeat. Investors have learned their lesson about individual asset classes and have responded by embracing a diversified portfolio of financial assets.

History, however, does rhyme. The promise of passive investing is that investors are entitled to historical rates of return regardless of valuations or economic fundamentals. Belief in this promise requires exceptionally euphoric thinking today. When the 10-year treasury bond yields 2% and that’s about the most any reasonable investor could also expect from stocks the reality in the financial markets becomes very clear. Investors, however, have a much altered sense of reality, influenced to a large extent by psychedelic monetary policy around the globe. But that’s a topic for another time.

Jimi Hendrix painting by VOKA