Millennial Markets

In a recent video interview Simon Sinek does a great job discussing the challenges facing Millennials in the workplace. Much of what he describes can be traced back to “failed parenting strategies.” Since listening to him I’ve thought a lot about it and it’s applications outside parenting.

Parenting might be the hardest job in the world. How do you raise someone who is confident but still humble? Curious but still prudent? Outgoing but not obnoxious. Creative but still truthful? True to themselves but not self-absorbed? Brave but not reckless? It’s a fine line to walk and a supreme challenge.

I’m currently parent to two teenagers who I love dearly so I have spent a great deal of time thinking about these things. Like all parents, I’ve also spent a great deal of time trying to understand and learn from the mistakes and the successes of parents I have known including, of course, my own.

I believe the “failed parenting strategies” Sinek is referring to are those that don’t even try to walk the line between instilling confidence and other virtues and still allowing for important failures. They simply do the former without the latter and to a fault. Overconfidence, recklessness, impatience and vanity are very easy traits to encourage but ultimately lead to self-loathing.

If I had to guess the one strategy most responsible for these results it would be “helicopter parenting.” This is the process of hovering over your child constantly, attending to their every need and micromanaging all of their formative experiences.

Helicopter parenting, by way of the constant attention and attentiveness, teaches a child they are the most important thing on the planet. It teaches them they deserve to be waited on hand and foot and engenders a powerful sense of entitlement.

How could anyone raised like this ever understand the value of humility? Or prudence? Or honesty? Or Patience? Or Selflessness? The value of all of these virtues is only learned through independent, and usually difficult, experience. One intentionally sheltered from these experiences is robbed of the gift of learning their benefits.

I don’t know if it is fair to say that there really is an entire generation affected in this way. I know Millennials who have certainly not been sheltered like this and it’s quickly apparent when you meet them. I also know a lot of people in my own generation (Gen X) and others who were clearly victims of precisely these “failed parenting strategies.” It couldn’t be more apparent when you meet them.

They are chronically unhappy people and their unhappiness directly stems from their failure to learn important life lessons early on in life. These lessons are the ones that allow to connect with other people on a deep level. They allow them to learn and be true to what it is you really value in life so that you can find some sort of fulfillment while you’re here.

Even worse, they have been taught that this unhappiness is not of their own making. It is the world that’s not treating them fairly, that doesn’t adequately appreciate their talents, that doesn’t cater to them the way they have become accustomed to.

I write about these folks not to shame them or criticize them even. The truth is I have a great deal of sympathy for them. I’m writing now because I think that “Helicopter Parenting” and “Helicopter Money” have much more in common than just the word “helicopter.”

The Fed over the past few decades is as guilty of these “failed parenting strategies” as the worst parental offender. Through its constant attention to the stock market it has created, for lack of a better term, a Millennial market that is plagued by all of the same challenges and short-comings children of these strategies face when they grow up.

The stock market, or at least the majority of its participants, have come believe they are entitled to sizable annual returns with the least amount of volatility simply due to the fact that they have decided to put their money there. The experience of the past few decades has taught them that overconfidence, impatience and recklessness will inevitably be rewarded by a doting and generous father-figure (or mother-figure now that Ms. Yellen is in charge).

The trouble is someday the stock market will grow up and the Fed will no longer be able to insulate it from the life lessons that it has been sheltered from for so long. We may actually see “helicopter money” before this happens but by then it might be like your mom going to have a chat with your boss to tell him she’s not happy with how hard he’s working you. It’s certainly well-meaning but likely does more harm than good.

Which reminds me of one of my favorite quotes that I think of mainly from a parenting perspective: “The worst thing you can do for those you love is the things they could and should do for themselves.” I like to think that Abraham Lincoln was also thinking about parenting when he wrote this. Doing so is essentially robbing someone of the rewards that accrue from hard work, independence, hard-earned experience and self-reliance.

At some point, I think these “failed parenting strategies” will lose favor in both our families and in our economy. Their results are too difficult to ignore. We will migrate back towards a sort of “tough love” that is not “tough” in the sense that it is in any way insensitive or uncaring. Just the opposite. It is “tough” in that it allows for short-term stumbles in order to prevent long-term suffering. In this way it is far more considerate and nurturing than its opposite.

To quote Sting, “if you love someone [or some economy and financial system], set them free [of your overbearing and selfish governance].” Only then can they find true happiness and fulfillment, in both an existential and financial sense.

Morning In Corporate America?

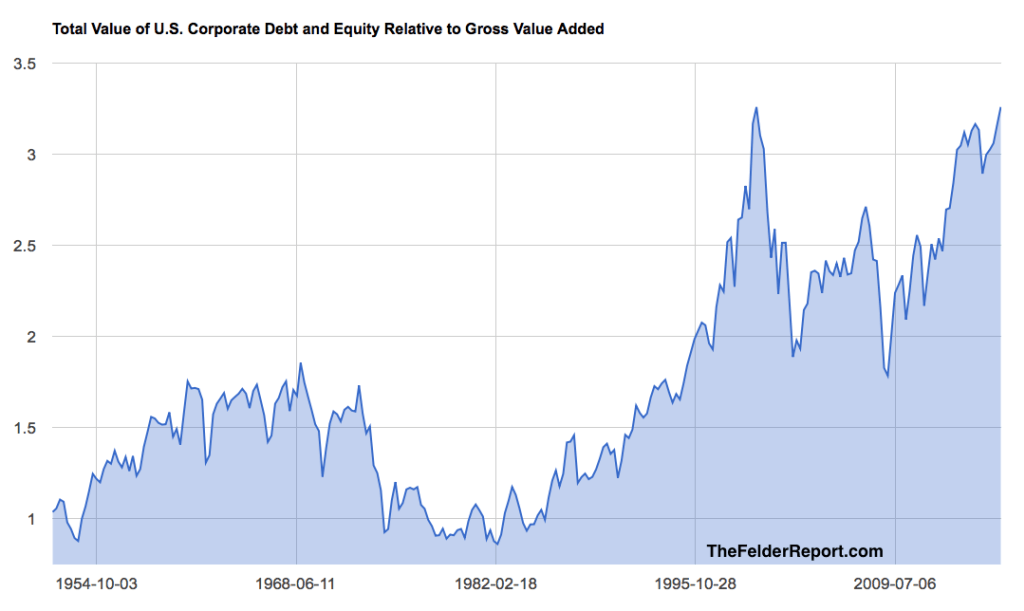

Valuations for all sorts of corporate securities are just off the charts today. The median stock has never been more overvalued on a price-to-sales basis than it is today. Junk bonds are also well into bubble territory, when defined as two-standard deviations above long-term averages. Put them together and you get the most pervasive bubble in financial assets we have ever seen.

On its face, this would seem to force only the most bearish conclusions. However, there is always the possibility that corporations could grow into these valuations and this would happen one of two ways: either through sales growth or expansion of profit margins. Based upon today’s extreme valuations corporations would probably have to do both and to a significant degree in order to justify the current pricing of their securities.

Sales growth would most likely come from an increase in demand. Yes, Trump has talked about fiscal stimulus and $500 billion in spending might do the trick here but it’s important to note that this is not a sustainable source of rising demand going forward. And, as Charles Gave recently pointed out, while increased government spending might provide a short-term economic boost it actually hurts the economy over a longer time period.

Sales growth can also come from inflation and this is another likely product of our new CEO of America. The trouble with inflation, though, is that it is not good for profit margins (or for valuations). More on this later.

A more natural or healthy source of demand would come from the consumer. As is often noted, consumers make up two-thirds of the economy. However, consumers have been taking advantage of super-low interest rates to load up on new cars, houses, clothes, etc. for eight years now. This expansion is getting pretty long in the tooth and consumer balance sheets are getting pretty stretched once again.

That strong upward rise in consumer leverage since 2009 is the product of zero-percent interest rates. Now that both long-term and short-term interest rates have reversed hard off of their lows can we reasonably expect this sort of credit-financed consumption to grow even faster than it has over the past eight years? When you also consider the squeeze being put on the average American by rising rents and healthcare costs the answer becomes a confident, “no.” Sales growth, at least the healthy kind, looks pretty hard to come by these days.

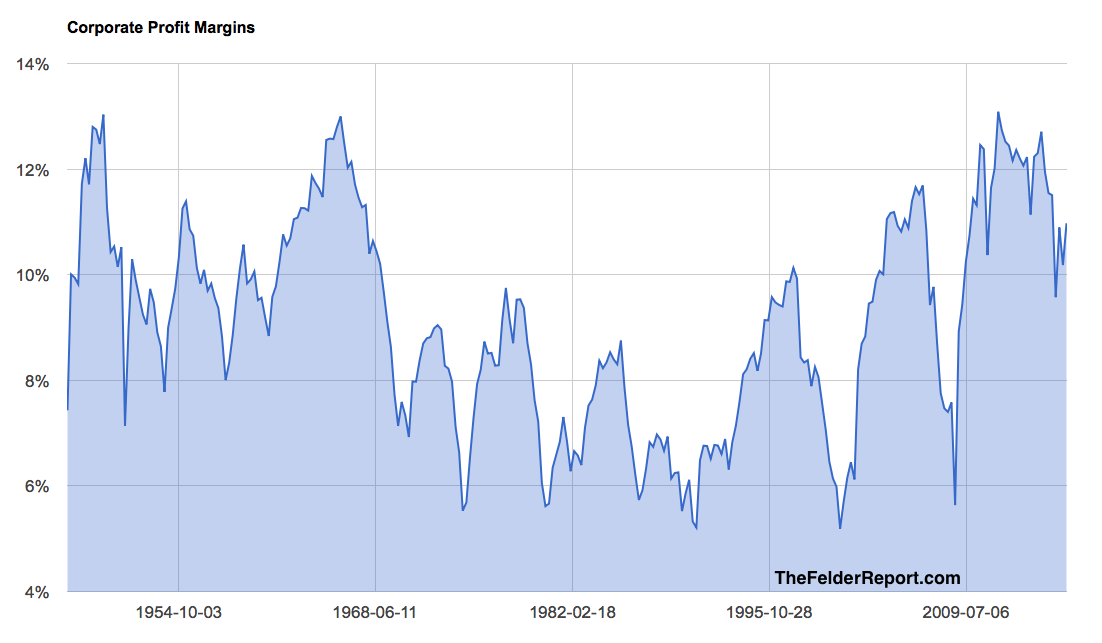

The other opportunity for corporations to try to grow into their extreme valuations is to expand their profit margins (though this would do nothing to ameliorate the record-high price-to-sales ratios in equities). To begin with, I’ll just note that margins have only recently begun to fall from record highs. Both Warren Buffett and Jeremy Grantham have noted in the past that this is probably, “the most mean-reverting series in finance.” And if mean-reversion has begun here margins not only have a long way to fall but also a potentially lot of time ahead to work off the extended period of elevated profits corporations have recently enjoyed.

I have written that I believe there are three major forces behind the boom in profit margin over the past few decades. These are interest rates, globalization and demographics. Falling interest rates have been a tailwind to profits lowering the cost of capital for corporate America for the past 35 years. That tailwind has now ended and could possibly turn into a headwind should interest rates continue their recent ascent.

As noted many times by our president elect recently, globalization has allowed American companies to reduce their labor and production costs through outsourcing and offshoring. If he is true to his word, this is another tailwind to costs that a president Trump could turn into a headwind for many companies.

Finally, in terms of demographics, the baby boom generation represented a massive influx of labor into the economy over the past 35 years. This increased competition for jobs pushing down labor costs. As these folks have been retiring in greater numbers, and smaller generations like my own have been unable to fill the void, the labor force has been shrinking. (The number of folks dropping out of the labor force is also due to other factors beyond the scope of this discussion.) This leads to less competition for jobs and thus higher labor costs for corporations.

All three of these powerful tailwinds to corporate profits have now abated. In fact, they may now be reversing in the other direction. Sure, a rebound in energy profits as a product of higher oil prices could affect these measures in the short-term. But, in terms of sustainable forces driving margins higher, I just don’t see any low-hanging fruit here. In fact, I see a secular shift toward rising costs.

So the prospects for corporate America to grow into the extreme valuations of their securities look very slim. What is far more likely, in my view, is that the forces above conspire to lead us into recession. I imagine this would be a recession the new administration would welcome as a chance to reset expectations and blame the massive challenges in front of them on their predecessors. As I wrote last week, this is right out of the American CEO handbook, something I’m sure Donald Trump is very familiar with.