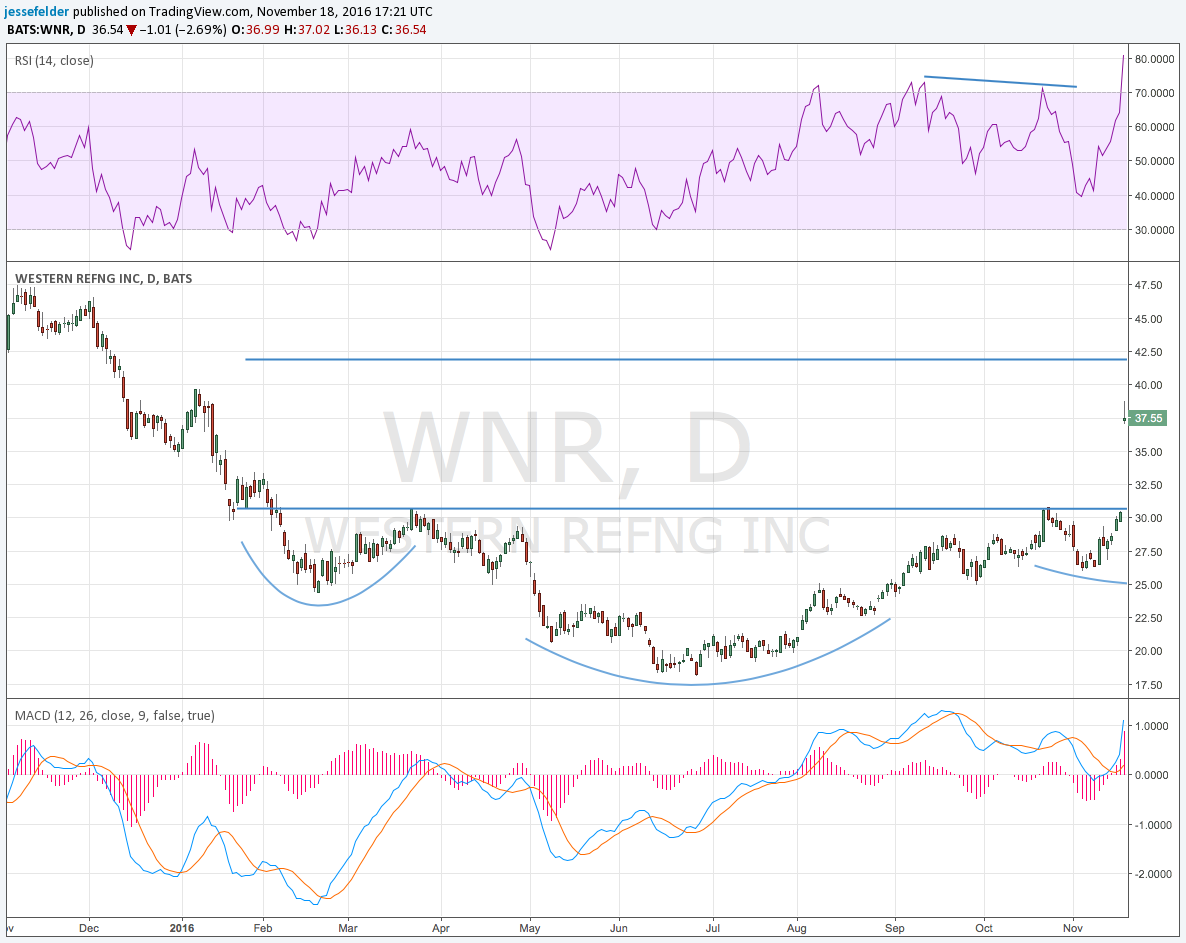

Yesterday Tesoro announced it was buying Western Refining at more than a 20% premium to its closing price on Wednesday. The deal values WNR at $37.30 per share, pretty close to our fair value estimate of about $39. It’s still a bit below the inverted head and shoulders projection in the chart below…

…but TSO doesn’t look much different than WNR from a technical perspective. If it continues what looks like a bottoming process and is able to resume its uptrend, WNR shareholders will benefit and possibly even see that $42 target in the chart above.

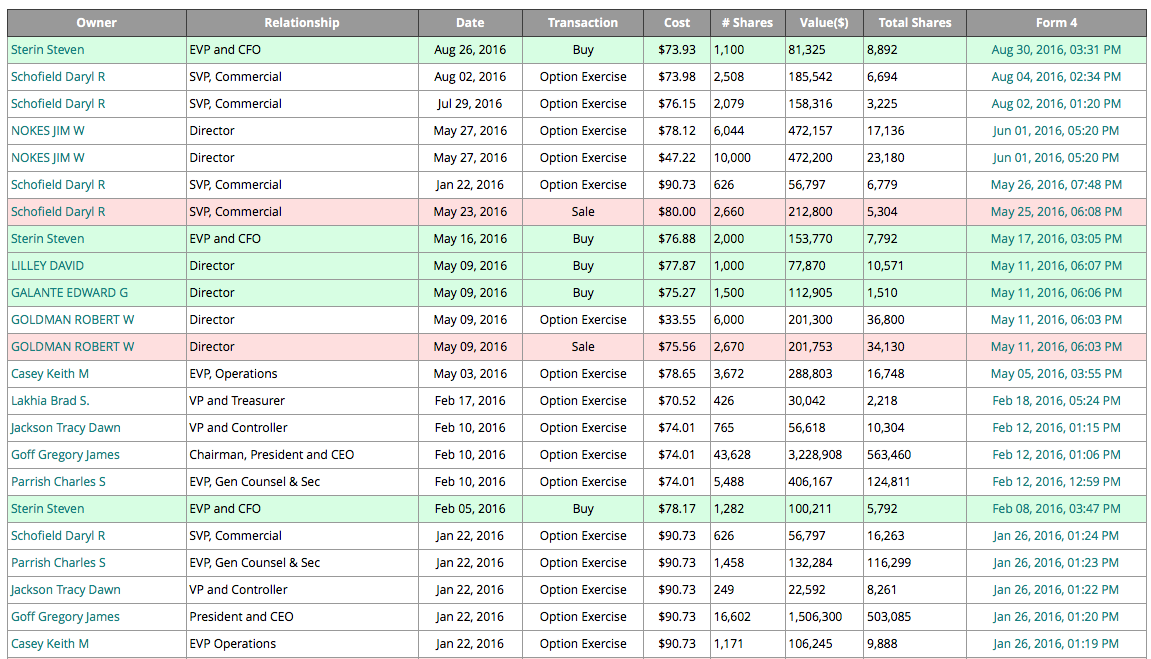

TSO doesn’t look nearly as cheap to me as WNR did. However, the CFO, Steve Sterin, certainly sees something he likes in TSO shares. He’s been a consistent buyer all year long. His $370,000 in purchases amounts to half of his base salary in 2016. Many other executives have exercised options without selling any, even to pay the associated taxes, and it’s hard to see that as anything but bullish for the shares.

For these reasons, like WNR’s management I’m happy to take TSO shares in the deal while I monitor how the transaction plays out and how it may benefit both companies.