Here in Oregon we have a measure on the ballot which would allow public universities to invest in equities. What I find interesting, besides the fact that Oregon is one of the few states that precludes them from doing so, is how the state pitches the ballot measure:

This measure allows investments in equities by public universities to reduce financial risk and increase investments to benefit students. Additional investment income could benefit students by minimizing tuition increases and enhancing student programs.

In other words, expanding investment options from risk-free securities to risk assets like stocks will “reduce financial risk” for public universities in going forward. While I agree that diversification has historically helped to “reduce financial risk,” what matters most in terms of risk is the price you pay.

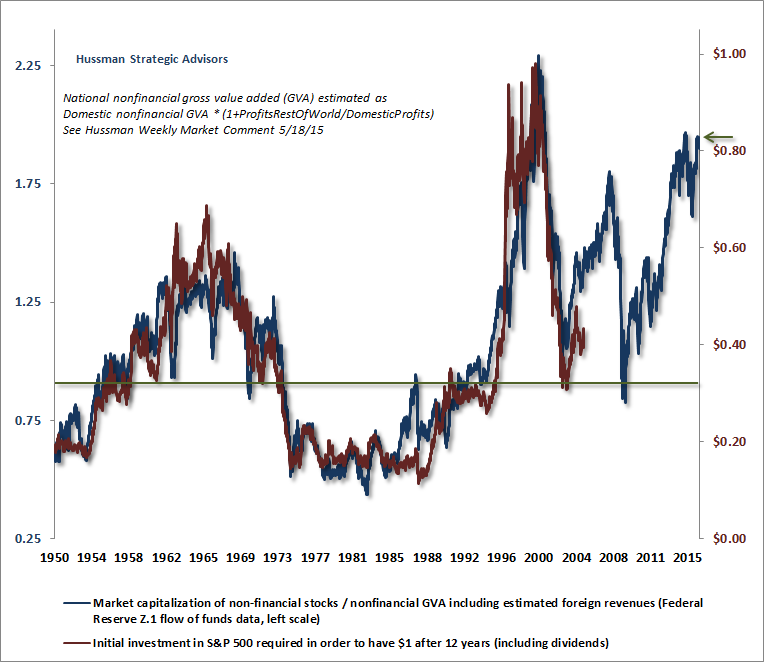

The truth is buying equities today is one of the riskiest propositions in the history of these markets. Valuations are extremely high. As Dr. John Hussman points out, the only time the stock market has been more highly valued than it is today was for a few months at the very peak of the dotcom mania.

Chart via HussmanFunds.com

Chart via HussmanFunds.com

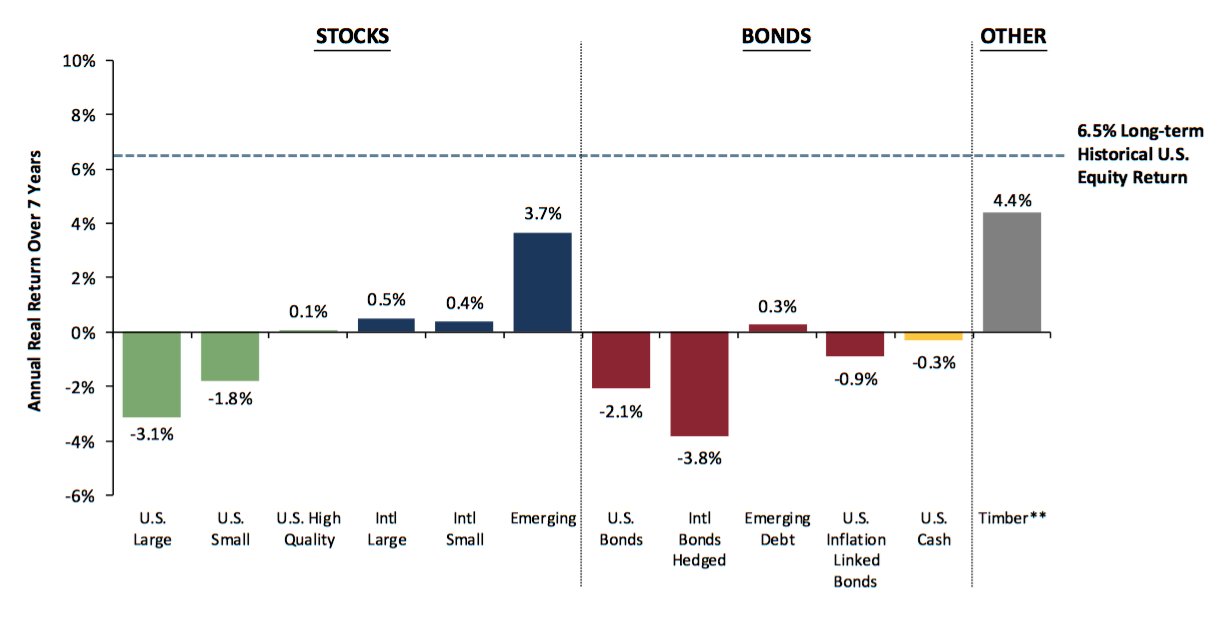

Because prices are extremely high today, returns going forward will be extremely poor. As Warren Buffett has said time and again, “the price you pay determines your rate of return.” According to GMO points out, high valuations today mean the average annual real return from owning stocks over the next 7 years is a negative 3.1%:

Chart via GMO.com

Chart via GMO.com

High valuations also mean greater risk of loss. Mark Spitznagel demonstrates in his book The Dao of Capital how this works using a version of the Q Ratio. When valuations are low drawdowns are usually minimal. Conversely, when stocks are very highly valued as they are today (in that 4th quartile in the chart below), drawdowns are usually very substantial.

Chart via The Dao of Capital

Chart via The Dao of Capital

So if Oregon wants to claim that they aim to reduce risk in funding public universities by diversifying their investment options that’s fine. However, claiming that investing in equities today will allow them to accomplish this goal is misleading at best. Prices today mathematically discredit that argument.

What might be the most fascinating part of this whole thing is that there has been no effort at all to propose any counterargument to be included in the voter’s guide. In other words, there is a clear consensus today that buying stocks means reducing risk. And from a sentiment perspective, this idea could only be believable, in the eyes of both politicians and voters, after one of the most powerful and sustained bull markets in history.