We are approaching the 20th anniversary of Alan Greenspan’s famous “irrational exuberance” speech. Many remember those two words but few remember their context:

Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past.

But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? And how do we factor that assessment into monetary policy? We as central bankers need not be concerned if a collapsing financial asset bubble does not threaten to impair the real economy, its production, jobs, and price stability.

Indeed, the sharp stock market break of 1987 had few negative consequences for the economy. But we should not underestimate or become complacent about the complexity of the interactions of asset markets and the economy. Thus, evaluating shifts in balance sheets generally, and in asset prices particularly, must be an integral part of the development of monetary policy.

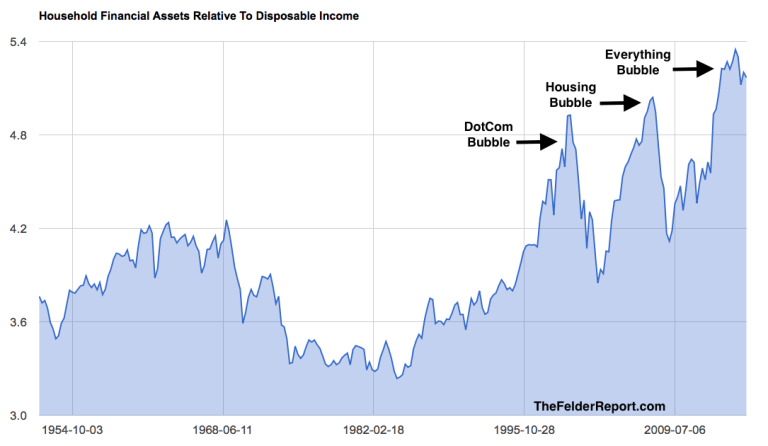

In December of 1996, Greenspan was clearly beginning to worry about the economic fallout of a bursting asset bubble. Back then he had a front row seat and, in fact, a strong hand in creating the dotcom bubble, whether he admits it or not. He was so worried about the consequences of “irrational exuberance” that he declared these concerns “must be an integral part of the development of monetary policy.” And this was before he had even witnessed any of the actual economic consequences we have now lived with for two decades. Clearly, his worries were well founded but he wasn’t quite worried enough.

The financial well-being of entire generations has been permanently damaged. Think of the Baby Boomers whose retirement dreams turned to nightmares through two stock market crashes in less than a decade. Think of the Generation Xers whose dreams were shattered by the housing bubble and the mortgage crisis. As a group these latter folks, even though they are now entering their peak earnings years, are flat broke almost a decade after it all began. And the major media outlets wonder openly why the average American has next to nothing in savings. He was explicitly encouraged by the single most powerful institution on the planet to put his savings into great peril, time and again.

Now I should be clear that over the decade following this famous speech, while he remained Fed Chairman, he did nothing to incorporate these prescient concerns into Fed policy. Just the opposite. After the dotcom bubble burst he engineered the housing bubble to try to ameliorate the damage done by the first. It’s one thing to worry about the risks of financial bubbles you have a hand in creating; it’s something else to actually do something about them. So while we can admire his foresight we should not honor it by overlooking his cowardice in failing to do anything about it.

Now I should be clear that over the decade following this famous speech, while he remained Fed Chairman, he did nothing to incorporate these prescient concerns into Fed policy. Just the opposite. After the dotcom bubble burst he engineered the housing bubble to try to ameliorate the damage done by the first. It’s one thing to worry about the risks of financial bubbles you have a hand in creating; it’s something else to actually do something about them. So while we can admire his foresight we should not honor it by overlooking his cowardice in failing to do anything about it.

Since then, and with the benefit of witnessing the actual fallout of these epic busts, many at the Fed (and even more outside of it) have openly discussed this dilemma of directly addressing asset bubbles. Eric Rosengren, head of the Fed Bank of Boston, became the latest to openly echo Greenspan’s concerns regarding “irrational exuberance” in the financial markets. Robert Shiller won a Nobel Prize for work in this very area. Still, nothing has been done to actually address these massive economic risks. After 20 years and two bursting bubbles whose effects are still plaguing the economy it’s still nothing more than sporadic public hand wringing by the people with the power to do something about it.

In recent years the Fed has only doubled down on these policies by directly pursuing a “wealth effect.” Rather than give a boost to the broad economy, however, these central bankers have only accomplished an even greater and more pervasive financial asset perversion. Stocks, bonds and real estate have all become as overvalued as we have ever seen any one of them individually in this country. The end result of all of this money printing and interest rate manipulation is the worst economic expansion since the Great Depression and the greatest wealth inequality since that period, as well.

Someday, possibly soon, the public will finally decide it’s had enough of the escalating boom bust cycles the Fed has exacerbated, if not directly engineered, over the past couple of decades. Falling confidence in these technocrats and the resulting rising populism will serve as a clarion call for a new brand of Fed Chairman with the courage to finally address the glaring danger asset bubbles pose to financial stability and the long-term economic health of our nation. She will be the 21st century’s version of Paul Volcker. Rather than breaking the back of inflation in the traditional sense, she will break the cycle of unwarranted asset inflation at the direction of the Fed and all of its deleterious consequences. At least I hope it’s not irrational to believe so.