“We’ve never had a decline in house prices on a nationwide basis.” -Ben Bernanke, July 2005

Just because something has never happened in the past doesn’t mean it can’t happen in the future. Believing this to be true is just another form of recency bias or extrapolation which, as I have written, is the single greatest mistake investors make. Furthermore, the sort of confidence that underlies the willingness to use the word “never” can be a wonderful sentiment signal on its own.

“In the investment world when you hear ‘never,’ as in rates are ‘never’ going up, it’s probably about to happen.” –Jeff Gundlach

This certainly proved true after Ben Bernanke famously used the word back in the summer of 2005. Real estate prices were just beginning to embark on their very first year-over-year decline on a nationwide basis just as he was denying the very possibility. The fact that Dr. Bernanke was so comfortable extrapolating the historical record indefinitely into the future and to disregard all of the evidence of a bubble should in itself have served as a clear warning.

More recently we have seen this sort of confidence appear in the bond market. Over the summer I wrote a pair of posts tracking what I thought was an ongoing “blowoff” in bonds (here and here). Since then I’ve collected a number of headlines that reflect exactly the sort of confidence that inspires the word “never” (or, in some cases, “forever”).

Normal Interest Rates May Never Return –Business Insider, May 11

Why We’ll Never See ‘Normal Interest Rates Again –Investing.com, July 11

Why Ultra-Low Interest Rates Are Here To Stay –WSJ, July 13

Markets Now Expect Inflation To Remain Low…Forever –WSJ, August 25

What If Rates Never Rise? -Financial Times, September 30

Certainly, Jeff Gundlach, widely considered the “Bond King,” seems to think this sort of sentiment is likely to mark a long-term top in the market. And he’s not alone. Ray Dalio, another major player in the world of bonds, recently warned about the awful risk/reward setup they currently offer calling them a “very bad deal.”

“It would only take a 100 bp rise in Treasury yields to trigger the worst price decline in bonds since the 1981 crash.” –Ray Dalio

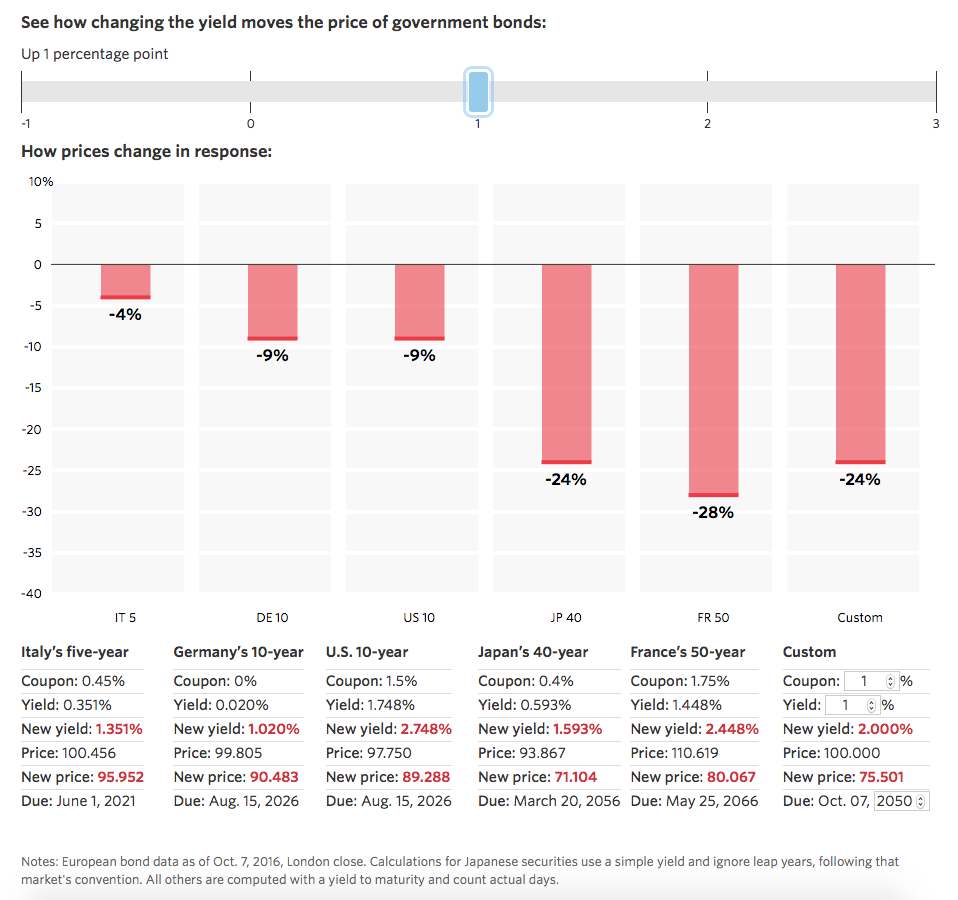

For those unaware of how this bond market math works, the WSJ recently created a helpful calculator here:

Another thing investors may want to consider is the fact that equity prices over the past several years have become very sensitive to interest rates, as well. If interest rates were to rise again, in defiance of all of the “never” calls we have seen recently, it would likely mean equity valuations would fall at the same time. Ray Dalio again explains:

If interest rates rise just a little bit more than is discounted in the curve it will have a big negative effect on bonds and all asset prices, as they are all very sensitive to the discount rate used to calculate the present value of their future cash flows. That is because with interest rates having declined, the effective durations of all assets have lengthened, so they are more price-sensitive.

Here, too, we have seen investor confidence soar. The explosion in the popularity of passive investing in recent years has been enabled by growing faith in a single idea (emphasis theirs, not mine): “The S&P 500 has NEVER suffered a loss in a 20-year period.” Clearly, investors are once again extrapolating history out indefinitely into the future in assuming they “can’t lose” so long as they have a long enough time horizon.

However, as Keynes famously noted, “in the long run we are all dead.” I think Japanese equity investors would likely endorse this idea. It’s been nearly 30 years since their major stock market index peaked. And before you say that can “never” happen here you might want to consider the implications of that sort of confidence.

Related: