On Friday, the Wall Street Journal officially ran an obituary for the TED spread proclaiming: “The Ted Spread Is Dead, Baby. The Ted Spread Is Dead.” The article explains:

This spread charts the difference between the London interbank offered rate and the yield on three-month U.S. Treasury bills. Libor is a dollar-denominated global gauge of private-sector credit strength, particularly that of banks, and three-month bills measure an ultrasafe bet—the U.S. government’s creditworthiness. Ted stands for Treasury-Eurodollar rate, the Eurodollar being the greenback denominated lending reflected in the Libor rate.

For the past year and a half the spread has been creeping higher, rising from 0.2 of a percentage point at the turn of 2015, to 0.653 of a percentage point on Wednesday. That is the highest it has been since May 2009, in the aftermath of the global financial crisis, surpassing other moments of extreme stress, like the euro sovereign-debt crisis around 2011.

But there is a problem with that. Looming U.S. regulation of money-market funds has driven Libor higher, meaning that it isn’t quite the indicator that it once was.

Now this is clearly the consensus view of the TED spread today. The markets have largely ignored its recent widening. This is most notable in the divergence between the TED spread and the VIX which are normally highly correlated.

The Wall Street Journal then is merely representing the “first level thinking” of the masses, as the media almost always does. However, a successful investor must look beyond this simplified view and practice, in the words of Howard Marks, “second level thinking.” Marks’ concept of second-level thinking simply entails asking yourself, ‘what is the consensus and is it right?’

We already know the consensus is to dismiss the recent widening of the TED spread to new money market regulations. The market tells us as much. But is this explanation valid? Is it enough?

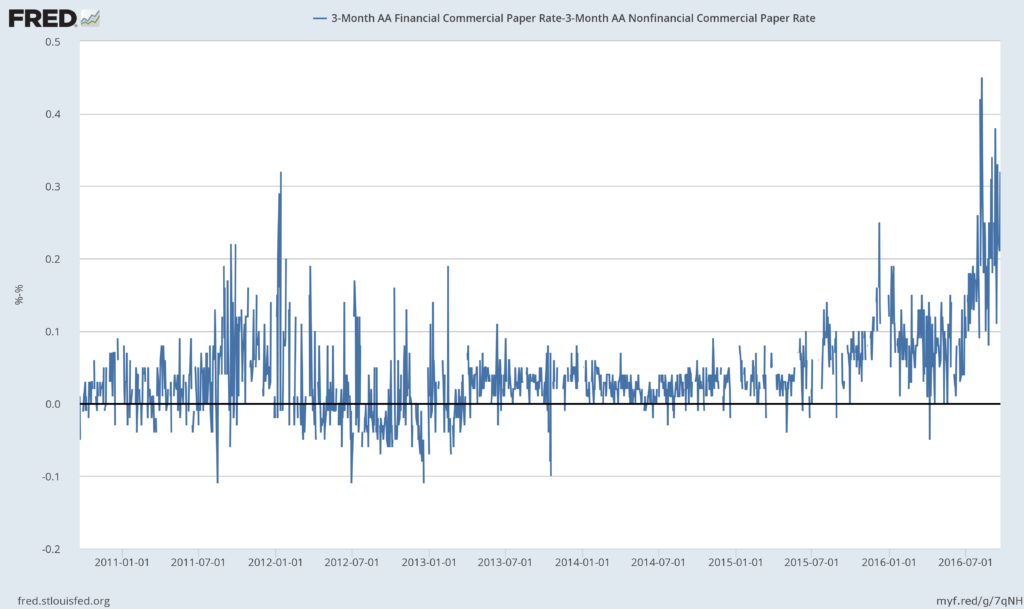

One measure I’ve been watching in this regard is the difference between the yield on AA-rated financial commercial paper and that of AA-rated nonfinancial commercial paper. My reasoning is this: If all of the widening in the TED spread were due to money moving out of commercial paper and into government paper it should affect these equally. And this is just not the case.

The spread between these two yields, like the TED spread, has now moved to its widest level since the financial crisis. In other words, spreads in the commercial paper market are confirming the message of rising financial stress in the widening TED spread rather than contradicting it, as most would have us believe.

Furthermore, anyone who has taken a glance at Deutsche Bank’s stock chart recently or that of any of the European bank stocks, for that matter, would not be surprised at all by these sorts of indicators showing rising financial stress. The only thing that is truly surprising is the fact that the consensus is so willing to disregard all of this evidence at the same time and buy the idea that money market reforms are the sum total of the issue.

Now these indicators may not lead to another financial debacle. That’s not my point. My point is that to write them off as worthless is an oversimplified view and possibly a very good sign of far too much complacency in the markets right now. Finally, if the VIX is to catch up to the TED spread that complacency could become problematic for the most crowded trade on Wall Street.