I recently detailed why using the ‘Fed Model‘ to buy stocks has never been more dangerous. In this post, I want to demonstrate another method that shows why stocks aren’t attractive relative to bonds right now.

Way back in 1992, Warren Buffett wrote about this very thing. In his letter to Berkshire Hathaway shareholders that year, he suggested investors ought to simply weigh the valuations of stocks versus bonds and buy whichever is more attractive. That only sounds rational, right?

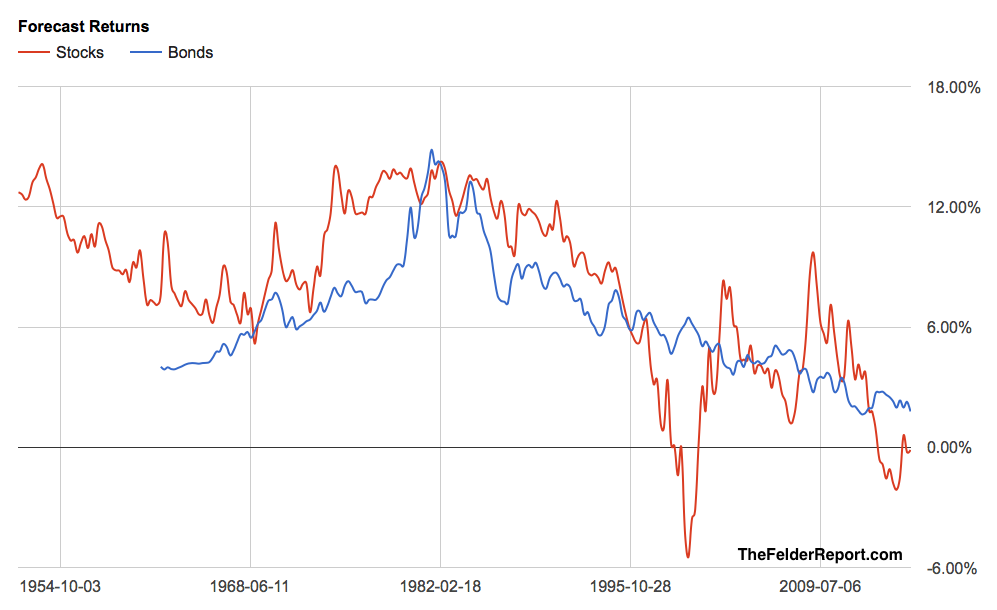

Looking at bonds today, the 10-year Treasury currently yields 1.6%. Not great but it is what it is. And that’s the easy part of this two-fold process. Determining what stocks are likely to return over the next decade is a bit more difficult.

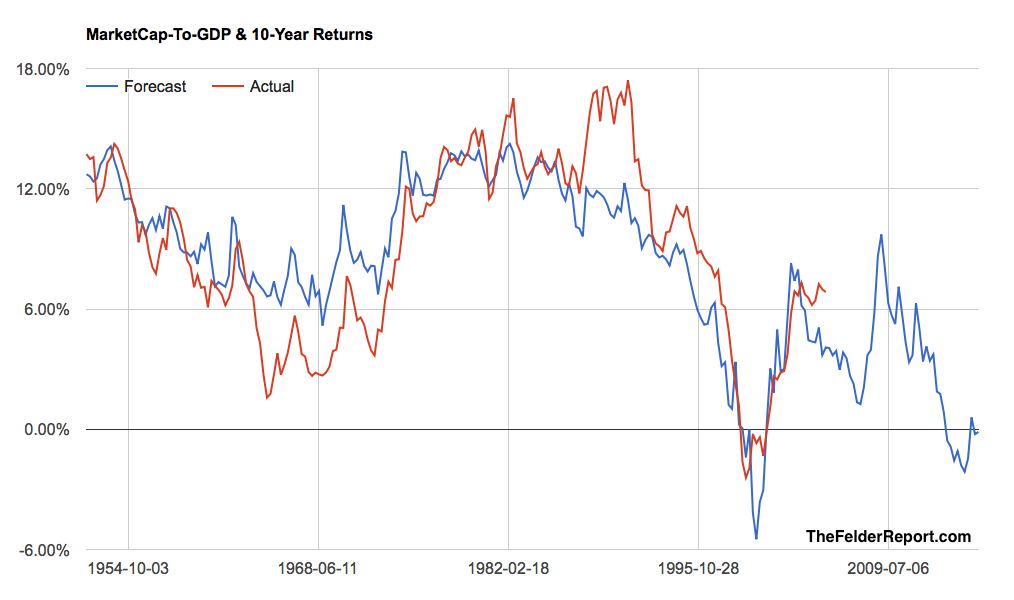

But Warren gives us an effective tool for this process, as well. His favorite valuation indicator for the broad stock market, total market cap-to-GDP, is very highly correlated with future 10-year returns in the stock market. When stocks have been very highly valued, forward returns have been very poor and vice versa.

Right now, this indicator once again shows the broad stock market to be very highly valued. In fact, it is so highly valued that it forecasts a negative average annual return over the coming decade. So while bonds’ super-low yields appear to be very unattractive, according to this measure, stocks’ prospective returns are even worse.

Now nobody really knows what the coming decade holds for these or any other asset classes. That said, history suggests that both are very highly valued and likely to disappoint investors expecting any sort of real return at all.

So the real question investors should be asking themselves is, “what sort of risk am I taking in heavily owning stocks or bonds in attempting to achieve little or no return over the next 10 years?”