Rumors of the demise of tech bubble 2.0 started percolating last year. Q1 of this year proved it wasn’t an exaggeration. Last month the Wall Street Journal reported that funding for startups fell 25% during that period, the largest decline since tech bubble 1.0 burst.

For many of the hottest startup communities outside of Silicon Valley it was even worse. According to Quartz, Seattle saw funding fall 28.5%. Denver-Boulder saw a 40.93% decline and in Austin it was worse still. The hottest of hot spots was down 63.5% in Q1.

Part of the problem is startups just got way too overvalued, as celebrity VC Peter Thiel recently told Bloomberg. And a rising number of failures (as a product of sky-high burn rates and silly business models) has changed investor risk appetites in the space. VC Bill Gurley recently wrote:

In late 2015, many public technology companies saw a significant retrenchment in their share prices primarily as a result of a reduction in valuation multiples. A high performing, high-growth SAAS company that may have been worth 10 or more times revenue was suddenly worth 4-7 times revenue. The same thing happened to many Internet stocks. These broad-based multiple contractions have an immediate impact on what investors are willing to pay for the more mature private companies.

Late 2015 also brought the arrival of “mutual fund markdowns.” Many Unicorns had taken private fundraising dollars from mutual funds. These mutual funds “mark-to-market” every day, and fund managers are compensated periodically on this performance. As a result, most firms have independent internal groups that periodically analyze valuations. With the public markets down, these groups began writing down Unicorn valuations. Once more, the fantasy began to come apart. The last round is not the permanent price, and being private does not mean you get a free pass on scrutiny.

At the same time, we also started to see an increase in startup failure. In addition to high profile companies like Fab.com, Quirky, Homejoy, and Secret, numerous other VC-backed companies began to shut their doors.

So valuations got too high, more and more companies have failed to live up to the hype and now valuations are falling. It’s the classic boom-bust cycle at work that should be all too familiar to anyone whose been around longer than just the past boom (aka, “half”) cycle.

The average unicorn saw its valuation fall > 8% in Q1: https://t.co/ugAJNBbwli ht @MarathonWealth pic.twitter.com/uxKnIO0cLn

— Jesse Felder (@jessefelder) March 31, 2016

Strangely, however, amid falling valuations and a significant decline in funding, Venture Capital firms are doing an amazing amount of fundraising themselves. In fact, during the massive decline in funding in Q1, VC’s did a record amount of fundraising – so where’s the disconnect? The WSJ reports today:

Mr. Rabois says the record fundraising actually is a bearish sign. Winter is coming, he says, and venture capitalists know it. “One of the reasons people are raising all these funds isn’t because they want the money, but because they believe their own metrics are inflated at the moment, and they want to get that money before companies in their portfolios start crashing and burning,” he said.

So it’s just a last grab for easy cash before it all dries up, or, ‘crashes and burns.’ VC’s clearly see the writing on the wall. Startups see it, too. They’re starting to cut back in an attempt to avoid getting caught in the rising tide of startup failures. This is where those incredible burn rates meet falling liquidity and the balance sheet fires really start to rage. Gurley again:

Layoffs have also become more prevalent. Mixpanel, Jawbone, Twitter, HotelTonight and many others made the tough decision to reduce headcount in an attempt to lower expenses (and presumably burn rate). Many modern entrepreneurs have limited exposure to the notion of failure or layoffs because it has been so long since these things were common in the industry.

The point Gurley makes is an important one: Many founders today weren’t around for the bursting of tech bubble 1.0 and so don’t understand how quickly or painfully it can all go south. And they now face a new challenge they can’t have imagined even six months ago: falling employee morale. Startup employee, Anna Weiner writes:

Our culture has been splintering for months. Members of our core team have been shepherded into conference rooms by top-level executives who proceed to question our loyalty. They’ve noticed the sea change. They’ve noticed we don’t seem as invested. We don’t stick around for in-office happy hour anymore; we don’t take new hires out for lunch on the company card. We’re not hitting our KPIs, we’re not serious about the OKRs. People keep using the word paranoid. Our primary investor has funded a direct competitor. This is what investors do, but it feels personal: Daddy still loves us, but he loves us less.

We get ourselves out of the office and into a bar. We have more in common than our grievances, but we kick off by speculating about our job security, complaining about the bureaucratic double-downs, casting blame for blocks and poor product decisions. We talk about our IPO like it’s the deus ex machina coming down from on high to save us — like it’s an inevitability, like our stock options will lift us out of our existential dread, away from the collective anxiety that ebbs and flows. Realistically, we know it could be years before an IPO, if there’s an IPO at all; we know in our hearts that money is a salve, not a solution.

With falling valuations, reduced funding, the IPO market shut down, and growing layoffs as the easiest tool to address problematic burn rates, just this sort of morale challenge must be growing across the startup universe. And once the bust reaches the employee level the confidence game is up.

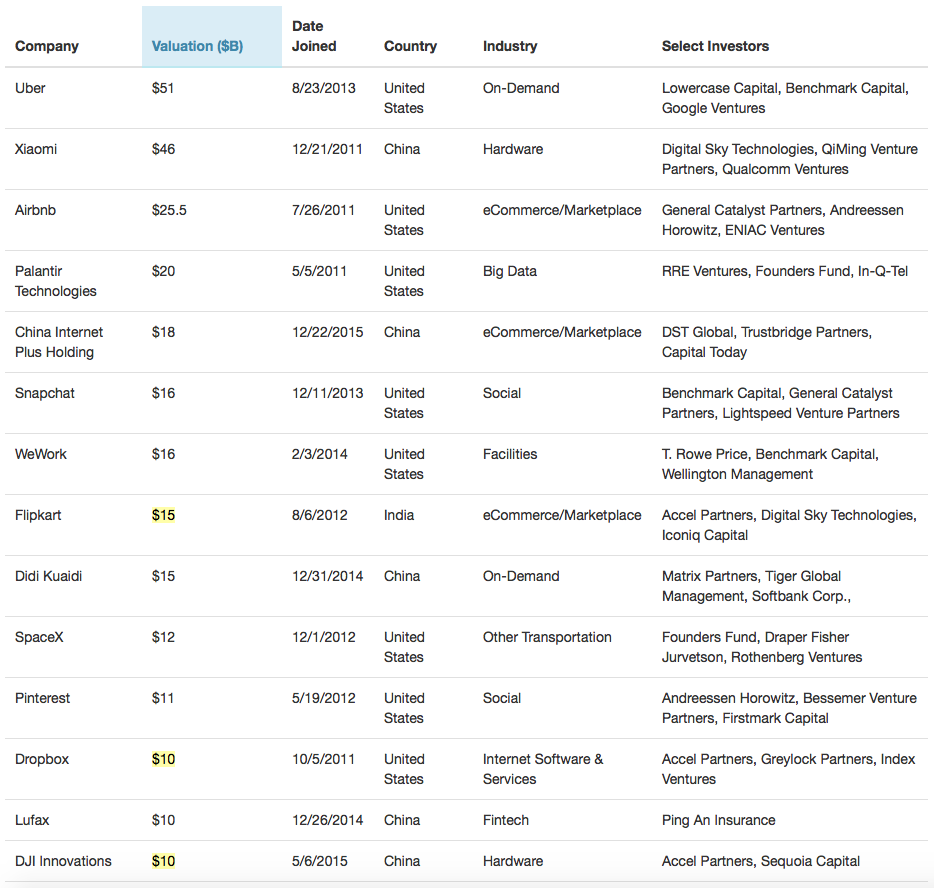

The gold rush is over. As Weiner writes, “ours is a ‘pickax-during-the-gold-rush’ product, the kind venture capitalists love to get behind.” And boy did VC’s get behind these sorts of companies. Just take a look at the list of the most highly-valued startups and think about how many of these business models have leveraged the growth in mobile/apps/smart-phones:

Chart via CBInsights

Chart via CBInsights

Now think about how many highly-valued startups not on this list were also built around the mobile boom. This was the startup gold rush of the past decade that was kicked off when Steve Jobs introduced the first iPhone back in June of 2007. And VC’s know all about getting rich during the gold rush. As my friend Jeff recently wrote:

How do you get rich in a gold rush? Not by looking for gold – by selling maps and shovels. You’ll make an absolute fortune selling maps and shovels in a gold rush. But your growth rates and business might not be sustainable in the long term.

VC’s certainly made an ungodly fortune during the recent boom. Now that it’s ending we’ll soon find out just how how sustainable these “pickax-during-the-gold-rush” business models really are. And considering the fact that the FANGs and their ilk have sold as many maps and shovels as anyone, it will probably be a public market story as much as a private market one.

FANG via @CyrilRcube pic.twitter.com/CFHgd5lMge

— Jesse Felder (@jessefelder) April 29, 2016