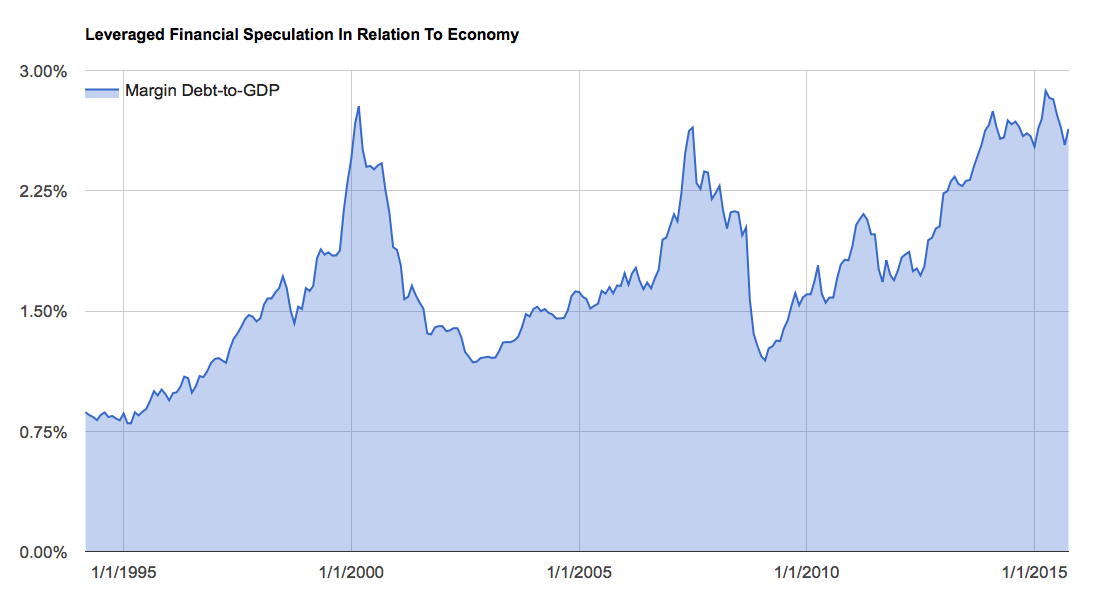

Margin debt made a comeback in October. With stocks rising 10% or so during the month this should not be surprising at all.

What is interesting, however, is the level of margin debt-to-GDP. As I’ve written many times before, I prefer this measure because it’s been highly correlated to forward 3-year returns in stocks for the past couple of decades.

With October’s gain of nearly $20 billion, margin debt-to-GDP has now risen back to 2.64%. This is equal to the level it achieved at the peak of the last major bull market, in July 2007. Before this, the only other month it ever got this high was February of 2000, just prior to the peak of the dotcom bubble. In other words, this is pretty rarified air.

To me, this simply suggests potential demand for stocks from this point is very limited (how much more can speculators borrow?) while potential supply is substantial (what happens when they decide it’s time to pay back these loans?).