I always love hearing people say things like, “interest rates are so low they can’t go any lower!” That’s the sort of superficial thinking that gets investors into trouble and provides opportunities for those willing to look a bit deeper.

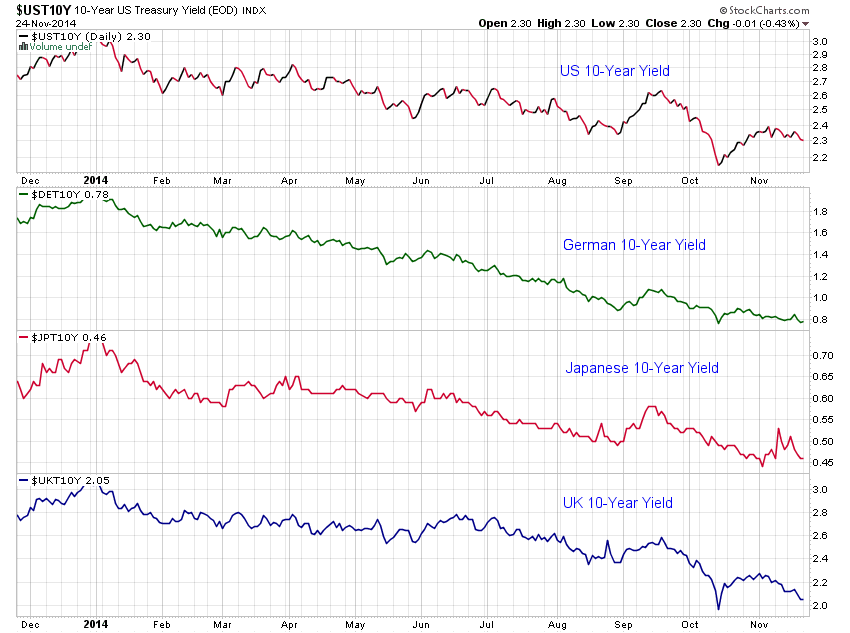

So let’s take a look and see if that’s actually true – that rates are as low as possible right now. Taking a quick look around the world at other developed nations it’s pretty plain to see that our bonds, even at a meager 2.3%, offer pretty incredible relative value:

The UK is paying a fairly comparable 2%. But Germany pays less than 0.8% and Japan’s minuscule yield is hardly worth mentioning. In fact, borrowing for next to nothing in Yen and then converting to dollars and purchasing long bonds (called a “carry trade”) has been a “no-brainer” (another kind of thinking that can get investors into trouble) for a long time now.

The question that comes to my mind when I look at this chart is, “why couldn’t our rates go as low as the UK, or Germany, or even Japan?” Maybe I’m just not imaginative enough but I can’t think of a bulletproof reason our rates should find a floor at current levels.

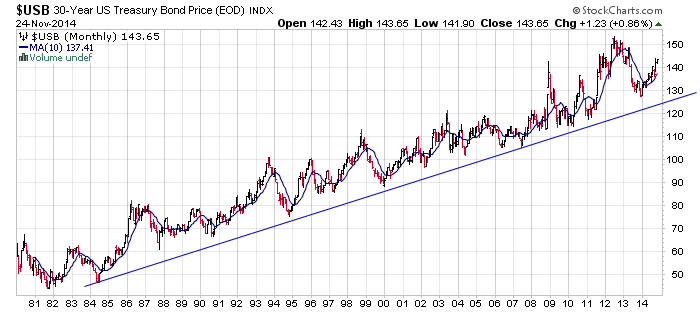

What’s probably even more important to consider is the fact that the Fed’s Quantitative Easing activities have dramatically reduced the supply of these bonds and because they are reinvesting the proceeds of maturing bonds that will remain the case for quite some time. And what happens when you dramatically reduce supply while demand holds fairly steady? That’s right! The price goes up. This isn’t rocket science, folks.

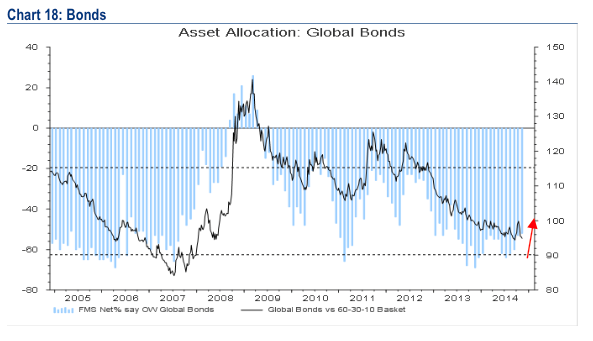

Then consider the fact that demand has been muted because portfolio managers (and individual investors) have absolutely hated these things for at least the past year. They haven’t been this underweight since 2007 right before long bonds went on an epic 50% run over 18 months:

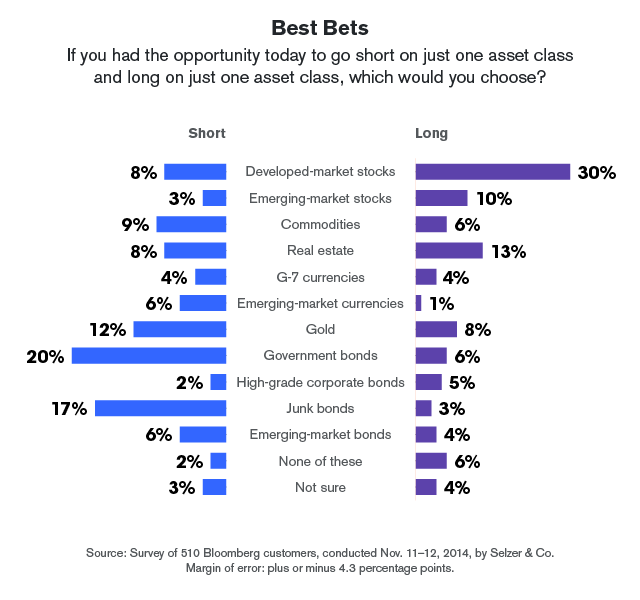

I’ll remind you that long bonds have been the best performing asset class so far in 2014 despite this meager demand from portfolio managers. It’s pretty amazing to consider that they still consider them their favorite short idea:

Imagine how they’ll do if portfolio managers and individual investors decide rates aren’t going higher any time soon and so they shouldn’t hate/short them anymore. Not to mention the potential for a “flight to safety” out of high-yield, leveraged loans or even stocks. Ultimately, I can see the distinct possibility of a real blowoff type of move at some point.

And wouldn’t that be the most fitting way for this epic bull run to end?

See also: “The $400 Billion Bond Mismatch Keeping Bears at Bay” -Bloomberg