I would LOVE to see a study of 'Warren Buffett Has Lost His Touch' headlines and major market peaks… http://t.co/DE1GmERIxq $BRKA

— Jesse Felder (@jessefelder) August 15, 2014

I tweeted this yesterday because Buffett invests for the full cycle. His outperformance usually comes during bear markets (for a variety of reasons including the quality of the companies he’s invested in, the “margin of safety” he demands from his purchases and the fact that he keeps some significant powder dry to take advantage “fear”).

During bull markets he just hopes to keep pace but during the final euphoric phase of bull runs he tends to lag (again for similar reasons including his focus is on larger, more established companies rather than the young, high-flyers that typically soar during these periods; the “margin of safety” he demands is simply not available when valuations are stretched and his growing cash position becomes a performance anchor).

Long story short, his underperformance during the later stages of bull runs is something the world’s greatest investor consciously tolerates in order to be in position to take advantage of the flipside of the cycle. Still, the media loves to rib him for it – every time. So I was curious to see if it could be quantified as a contrarian indicator.

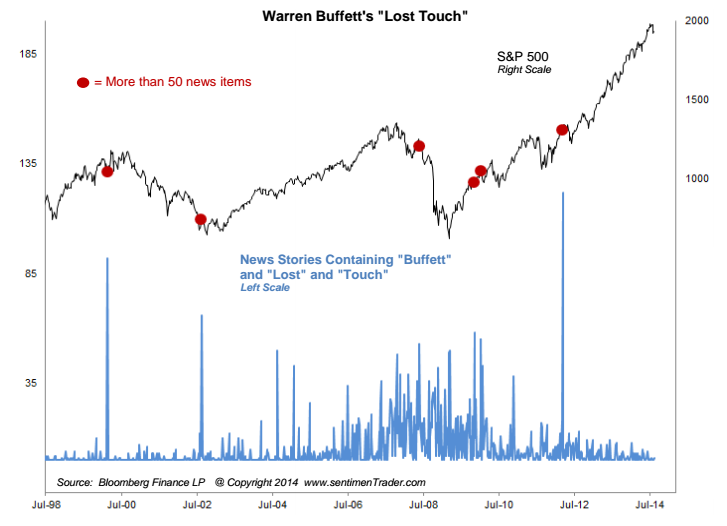

Thank you, Jason Goepfert! Jason ran a scan of headlines related to Warren Buffett ‘losing his touch’ and found:

Sure enough, spikes in these stories tended to occur near market turning points, including near the peaks in 2000 and 2008, the trough in 2002 and lesser intermediate-term corrections in 2010 and 2012.

However, aside from the Forbes article I tweeted yesterday we aren’t seeing much of a confluence of these sorts of stories in the media… yet. But I’m sure Jason will let us know if and when they do start to pile up.

However, aside from the Forbes article I tweeted yesterday we aren’t seeing much of a confluence of these sorts of stories in the media… yet. But I’m sure Jason will let us know if and when they do start to pile up.

For more of these kinds of sentiment studies check out SentimenTrader.com where Jason regularly publishes some superb work.