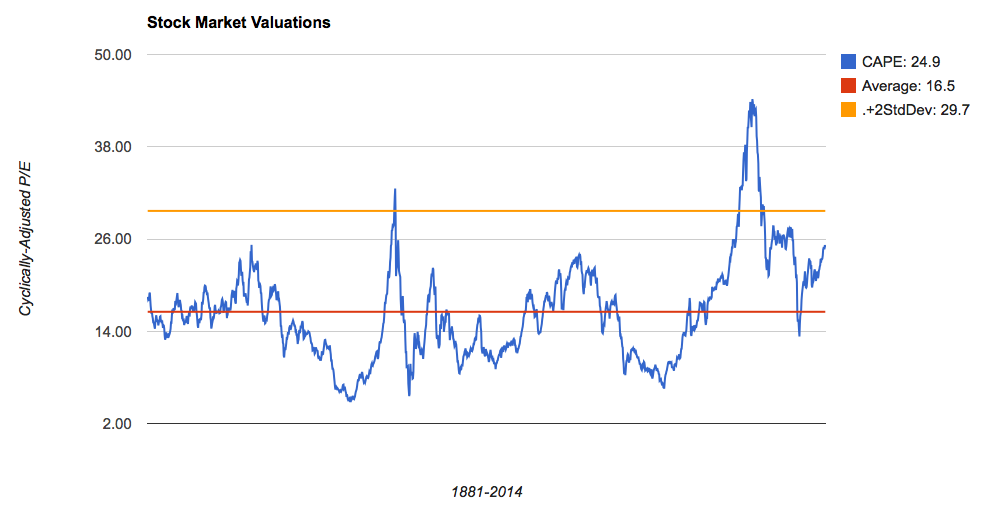

The other day I wrote about the various possible ways to define a bubble. Jeremy Grantham, one of the financial minds I admire most, defines a stock market bubble as a 2-standard deviation valuation event, that is, when stock valuations exceed their historical average by an amount that occurs less than 5% of the time.

This is exactly what happened during the internet bubble. In fact, valuations at that time far exceeded 2-standard deviations above their historical average. The chart below shows just how extended they became – that massive surge on the right hand side of the chart represents the dotcom bubble (and the prior occurrence is the 1929 bubble):

Data via Robert Shiller

Currently stock valuations are above average but nowhere near as expensive relative to their profits as they were back then.

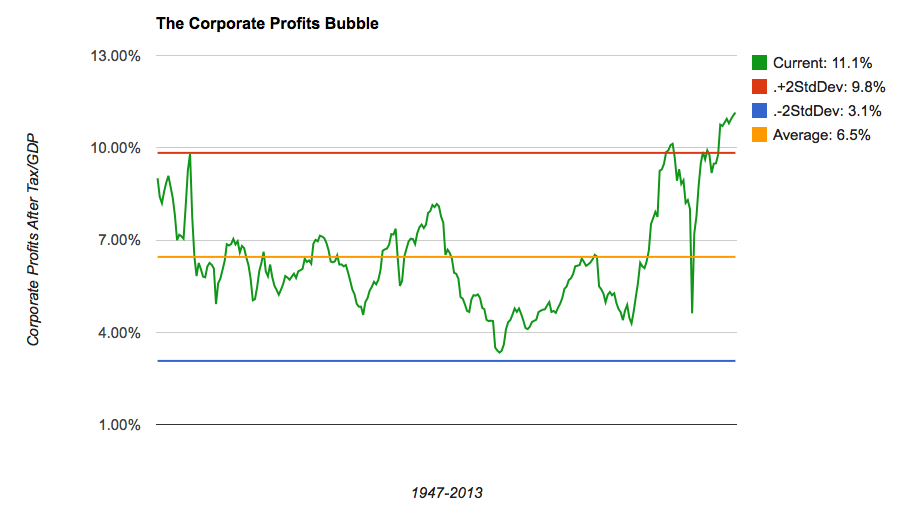

But what if the profits side of this equation was inflated so that this valuation measure was being depressed? In fact, it looks like that is exactly what’s happening right now. The chart below depicts corporate profits as a percent of GDP:

Data via FRED

If we are to use Grantham’s 2-standard deviation definition for a bubble then clearly we currently have a bubble in corporate profits to a degree that hasn’t been seen at any other point during the past 67 years (the data range provided by FRED).

Now some might argue that, “it’s different this time,” and profit margins won’t revert back to average but I find that hard to swallow. I believe Grantham would probably agree as does another brilliant financial mind:

[blockquote2]In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems—and in my view a major reslicing of the pie just isn’t going to happen. –Warren Buffett[/blockquote2]Unless our capitalist system has radically changed somehow then Mr. Buffett is right and profit margins will tend to revert back to their historical average of 6.5% over time. And if this is true then current valuation methods that incorporate inflated earnings as a denominator are simply unreliable.

Maybe this is why Mr. Buffett’s favorite valuation measure doesn’t incorporate earnings; it measures total equity market capitalization to GDP. When we look at this yardstick we can see that current stock valuations don’t look nearly as reasonable as they do relative to earings. In fact, they exceed 2-standard deviations above their historical average, suggesting that, according to Mr. Grantham’s definition, stocks are, indeed, currently in a bubble:

Chart via Doug Short

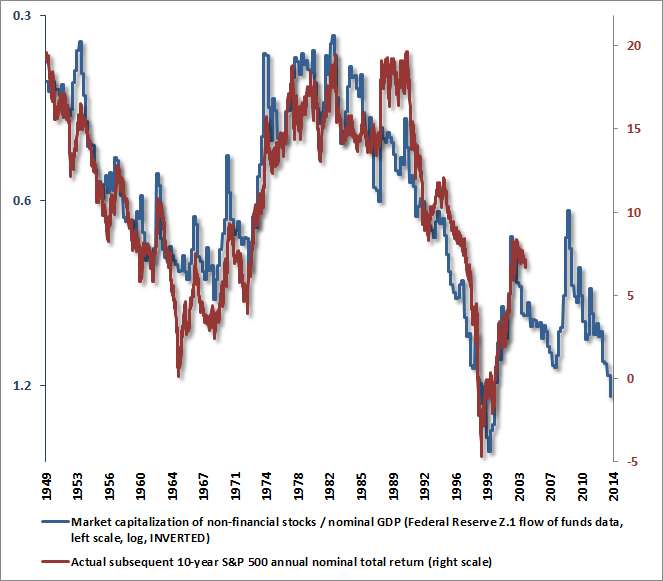

I believe that the reason Mr. Buffett puts so much stock into this measure is due to its practical use: it is one of the best predictors of future returns. The chart below is the inverse of the chart above overlayed with subsequent equity market returns. Right now this indicator suggests that future returns from stocks will be less than zero and it’s got a damn good track record to back it up:

Chart via John Hussman

Ultimately, stocks have only been this unattractive in the past less than 5% of the time (only during the dotcom bubble, really). Just because P/Es look reasonable doesn’t mean stocks are attractive. The “E” could very well turn out to be nothing more than a mirage.