Behold:

With the S&P 500 price/revenue ratio more than twice its historical norm prior to the late 1990’s market bubble, the ratio of market capitalization to GDP also more than twice its historical norm, the most lopsided bullish sentiment in decades, an overbought market trading at a record highs – and two standard deviations above its 20-period moving averages at weekly and monthly resolutions, a “log-periodic” bubble at its most likely finite-time singularity (see Estimating the Risk of a Market Crash), bond yields well above their 6-month average, an economy where growth in real GDP, real final sales and employment are all near or below the growth rates at which historical recessions have started, and our own estimates of prospective market return/risk quite negative based on a broad ensemble of observable market conditions, we view prospective near-term and multi-year returns as strongly unfavorable, and prospective market risk as unusually elevated.

Read his full weekly report at HussmanFunds.com

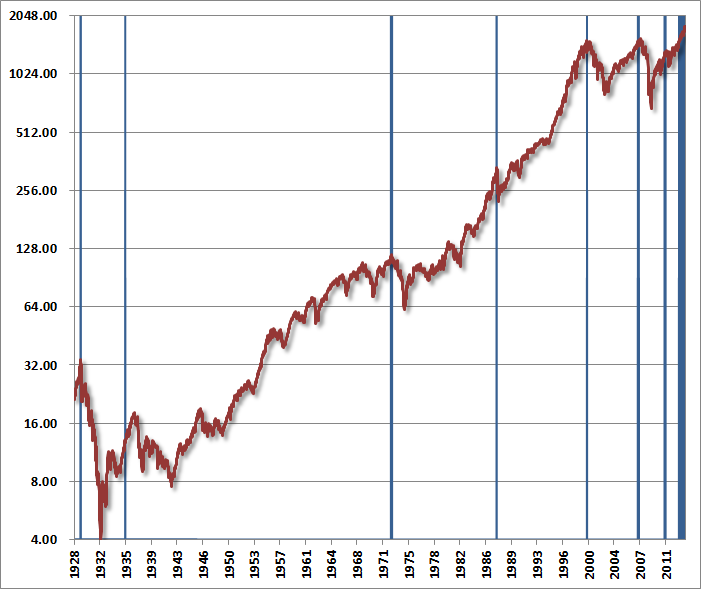

Here’s his chart of previous points in history when all of these data points lined up: