“The four most dangerous words in investing are ‘it’s different this time.'” -Sir John Templeton

I’m hearing a LOT of “it’s different this time” justifications from the bulls in response to record highs in margin debt levels, euphoric sentiment, waning momentum, soaring valuations, etc. (for a full rundown see “The Four Pillars Holding Up The Stock Market Are Crumbling“).

First off, on margin debt, the bulls seem to be dismissing it due to the fact that it is not a reliable catalyst for a reversal of the current uptrend. I would totally agree with that. In and of itself margin debt can’t put an end to the bull market. However, if and when a selloff does occur, the amount of margin debt outstanding can have a major influence on whether it is a mere pullback or becomes something bigger.

Margin calls and forced liquidations exacerbate stock market declines and are much more likely when a selloff begins with pervasive and extended margin debt levels. So when margin debt levels rise, especially to record highs, the likelihood of a new bear market grows. This is why it’s no coincidence that the major peaks and valleys of margin debt levels match up perfectly with the major peaks and valleys in stock prices.

As for valuations, there has been a blowback against Robert Shiller’s CAPE, which shows the market to be significantly overvalued, since he recently won the Nobel Prize in Economics. The common refrain seems to be, “stocks are cheap relative to the past 20 years,” or, “we are in a new era of productivity so old valuations don’t apply,” or, “you can’t compare the past with the current environment because there has never been quantitative easing before.”

Each one of these rationalizations are merely different ways of saying, “it’s different this time.” The funny thing is that yes, it’s always different. Still, history rhymes and assets never fail to revert to mean. So ignore the past at your peril.

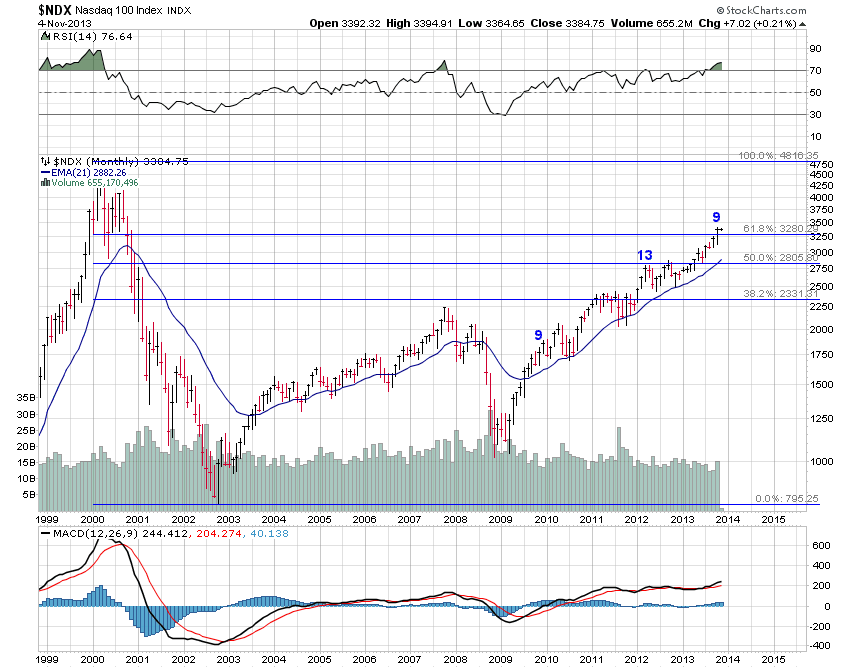

Chart of the Day:

The Nasdaq 100 completed a 9-13-9 DeMark Sequential sell signal last month.