Over the past few months the “blow off” camp has gotten fairly crowded. First, Jeremy Grantham said that we are very nearly in bubble in the stock market currently. However, he believes that bubbles don’t just fizzle out. They usually end in an epic move that runs faster and farther than anyone could ever imagine. Specifically, he’s looking for valuations to come fairly close to what we saw back in 1999.

Then, a few months later, David Tepper said that because this year rhymes (of course, history never repeats) with 1998 we could see a 1999-style surge in the stock market in 2015. Today, like in the late 90’s, money is being made too easy resulting in yet another asset bubble, he says. He is also looking for valuations that reach levels close to what we saw back in 1999 (according to him, today’s p/e is a mere 16 compared to 1999’s 40 but there are much better ways to measure valuations, in my humble opinion).

Recently, Richard Russell wrote a piece in which he revealed that he believes we are are only now entering the third phase of this bull market. He reminds us that gains in the third phase are usually equal to those of both phases one and two. Stocks have roughly tripled since the 2009 low (700 to 2100) so his expectation is about 3,500 on the S&P 500, almost 70% higher than its current level.

Just this week, Jim Rogers hopped aboard the “blow off” bus by saying he believes the stock market is probably due for some sort of decline but if stocks decline to any significant degree, the Fed will turn the printing presses back on and like never before sending stocks to ridiculous heights.

So we now have at least four respected pundits predicting an amazing “blow off” run for stocks. Know that I respect each of these individuals greatly and in their own right. Rogers is a hero of mine and I have as much admiration for Grantham’s work as for anyone in the industry.

Having said that, I strongly believe that the more popular a prediction becomes the less likely it is to come to pass. And this “blow off” thesis is getting fairly popular now. More importantly I’d like to try to examine what factors would have to align for this thesis to work.

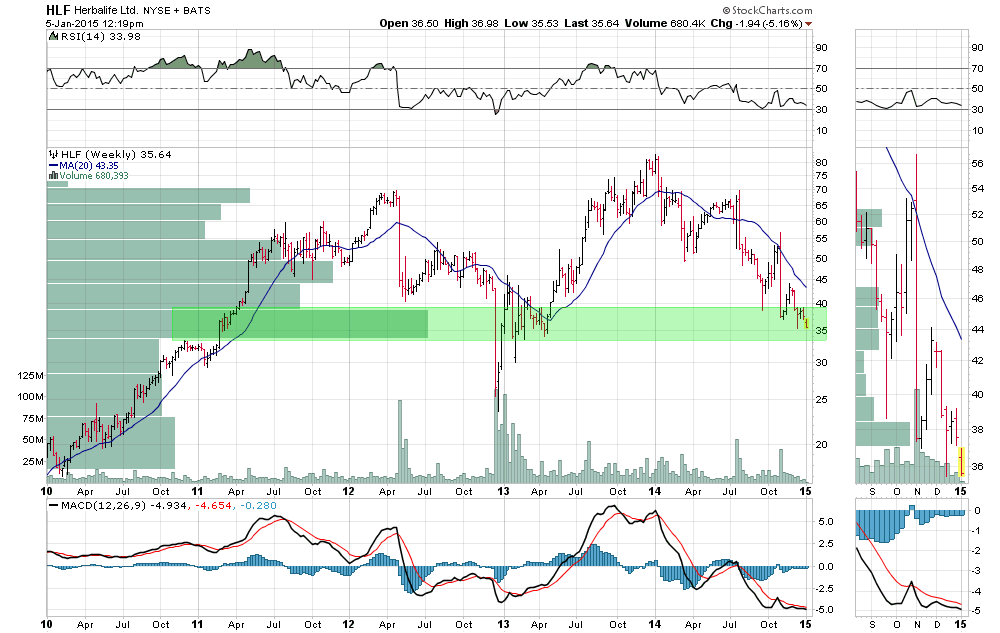

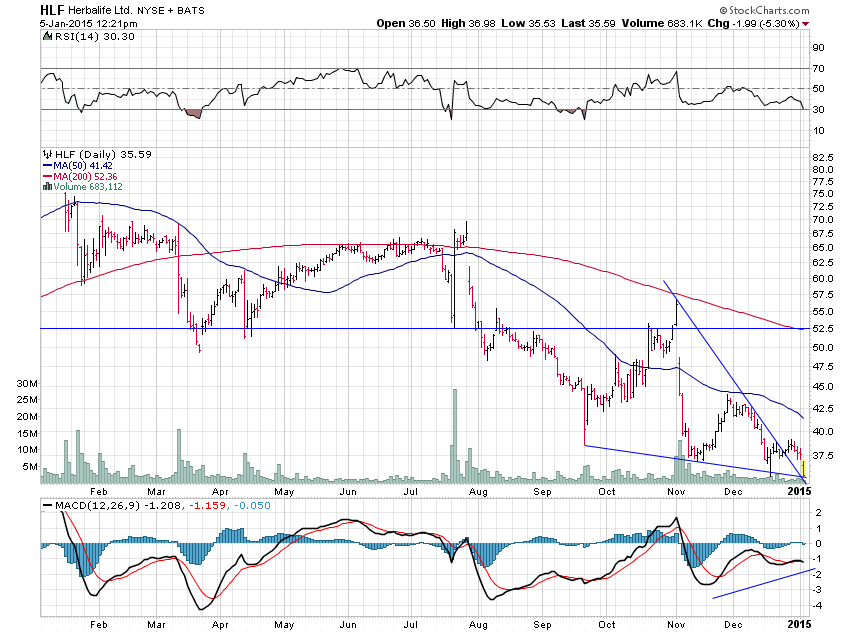

First, the credit markets, which I have been watching very closely, would have to rebound. The high-yield market has been showing signs of weakness since mid-summer last year. This makes sense as that area of the bond market has about a 14% exposure to companies directly affected by the oil crash. Leveraged loans, however, only have a 4% exposure and have been just as weak as high-yield so we can’t just write off the waning risk appetites there to the energy sector. I believe both would have to improve significantly for stocks to have any chance of a “blow off.”

Second, the global markets would have to avoid any significant fallout from the crashes in oil and in some emerging market currencies. There is a chance, though I have no idea how to put any probability on it, that there could be significant ramifications from the sharp moves we have seen recently in these areas.

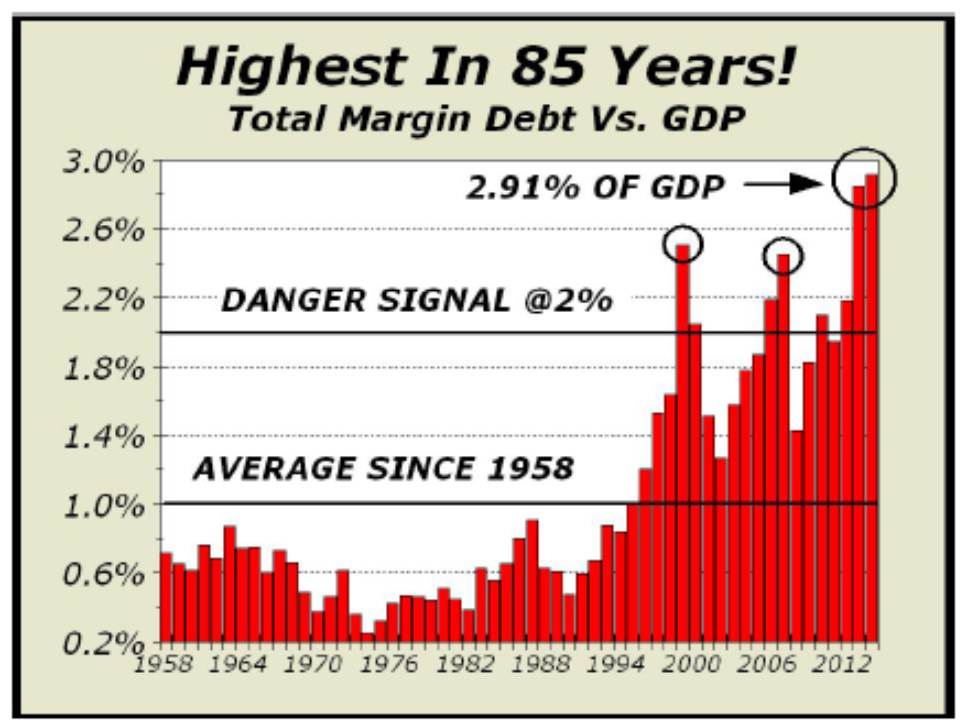

Third, because sentiment and valuations go hand-in-hand, investors would have to become even more bullish than they are today. This would mean allocating an even greater percentage of household assets to equities, a statistic that is already fairly stretched and looks to possibly be peaking. It would also mean they would have to take on even more margin debt which, in relation to GDP (or inflation-adjusted, take your pick) is already far higher than what we saw at the peak of the internet bubble.

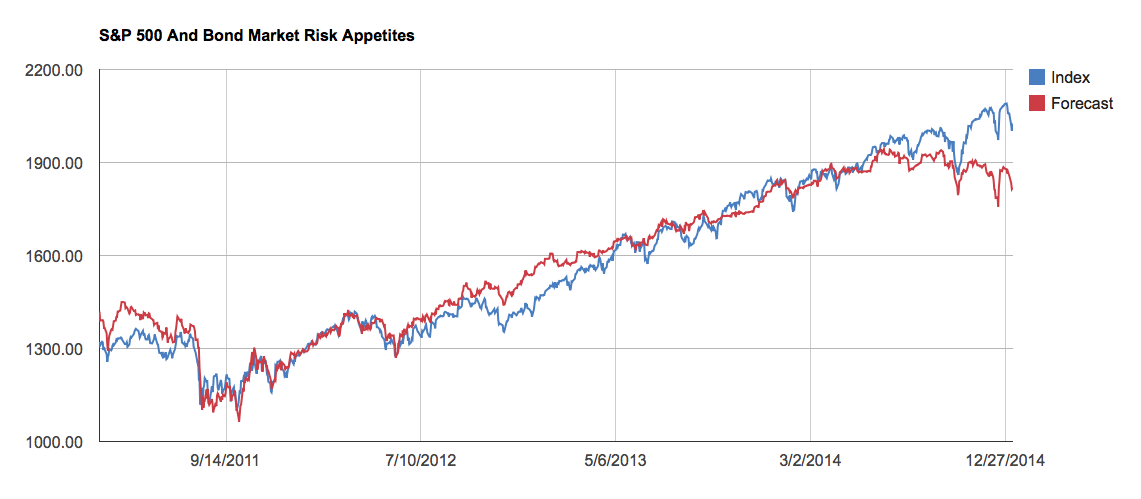

Chart from CrossCurrents via CNBC

Chart from CrossCurrents via CNBC

Fourth, baby boomers would have to, at the very least, maintain their current equity exposure. If this retiring generation decides at some point that they have too much exposure to equities it could create an incredible headwind for the markets. In fact, the San Francisco Fed recently suggested the S&P 500 could finish as low as 1,290 a decade from now, 40% lower than its current level.

Finally, market participants must to continue to have full faith in powers of the Fed to manage not only the stock and bond markets but the economy and the dollar, as well. This is not a given. I believe that the Fed is not as powerful as the markets currently give them credit for being. If stocks began to fall in response to some dislocation in the currency or commodity markets the Fed may be hard-pressed to create a fix. Investors should have learned this lesson in 2008 when the markets essentially ignored every effort on the part of the Fed to reign in the financial crisis.

Ultimately, a number of things have to align nearly perfectly for the stock market to see another 1999-style surge. I do, however, envision one major possible driver of an equity blow-off. Should investors, both foreign and domestic, decide that Europe, Japan and emerging markets are not the best place for their money and that the US is the right place, we could see a continued surge in the dollar and increasing demand for our investment assets.

But what might make them move so dramatically out of those markets? I think the most likely reason would be a dislocation in one or more of them. In that case, which asset class here would most likely benefit? Risk assets, like stocks and high-yield? Or risk-free treasury bonds? I believe investors looking for a safe haven would most likely pick the latter. This is one reason I wrote a couple of months ago that treasury bonds could be about to blast off. They have already risen 10% since then but in this scenario that could be only just the beginning.

As I wrote earlier, I have tremendous respect for these guys who are looking for a “blow off” in stocks. They could very well be proven right, yet again as they have many times during their careers. All in all, however, I think there are a lot of things that need to go exactly right for a “blow off” in stocks to materialize. What’s more likely, in my mind, is that we see a “blow off” in the bond market, something almost nobody expects right now.