Below are some of the most interesting things I came across this week. Click here to subscribe to our free weekly newsletter and get this post delivered to your inbox each Saturday morning.

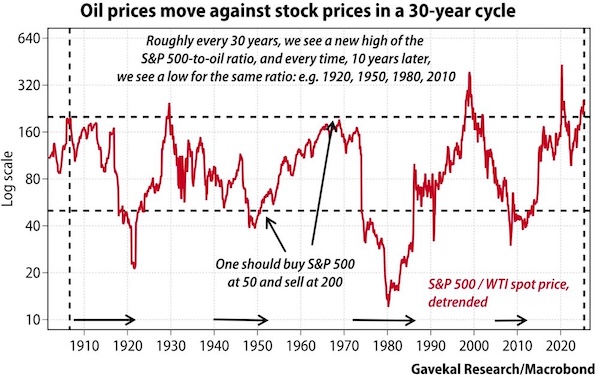

CHART

The 30-year cycle in the oil price suggests that, “We have likely seen the S&P 500 index peak versus oil in this cycle. Since the world has not invested much in the last 15 years drilling for oil, the shortage could arrive earlier than in past cycles,” writes Charles Gave (via David Hay).

STAT

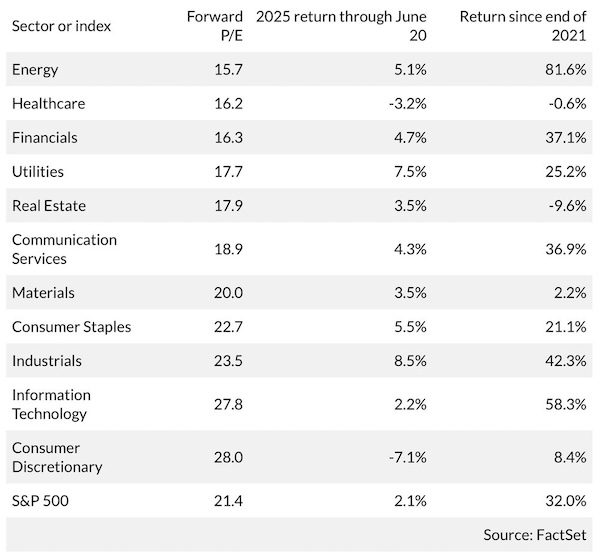

As Philip Van Doorn points out, despite generating the highest total return since 2021, the energy sector is still the cheapest of all 11 within the S&P 500 Index.

LINK

This can be explained by the fact that, “The market continues to value Chevron and Exxon Mobil primarily as cyclical oil companies. It has not yet priced in the possibility that these firms will become direct electricity suppliers to hyperscalers, a role that could warrant higher valuation multiples,” reports Ben Levinsohn.

POST

As noted by Luke Kawa, the ability to scale up production today to meet this soaring demand or even the growing demand from reshoring manufacturing is more limited than it has been at any point in over a decade: “Yeah the SPR is low, but the <real> SPR is…also low US drilled but uncompleted wells (i.e. DUCs).”

LINK

Thus, “the oil market may be lulled into a sense of complacency in the near term amid Iran’s weakened position. But this could very well be the catalyst for higher prices in the coming years as Iranian production declines just as other sources of supply peak,” writes Amrita Sen.