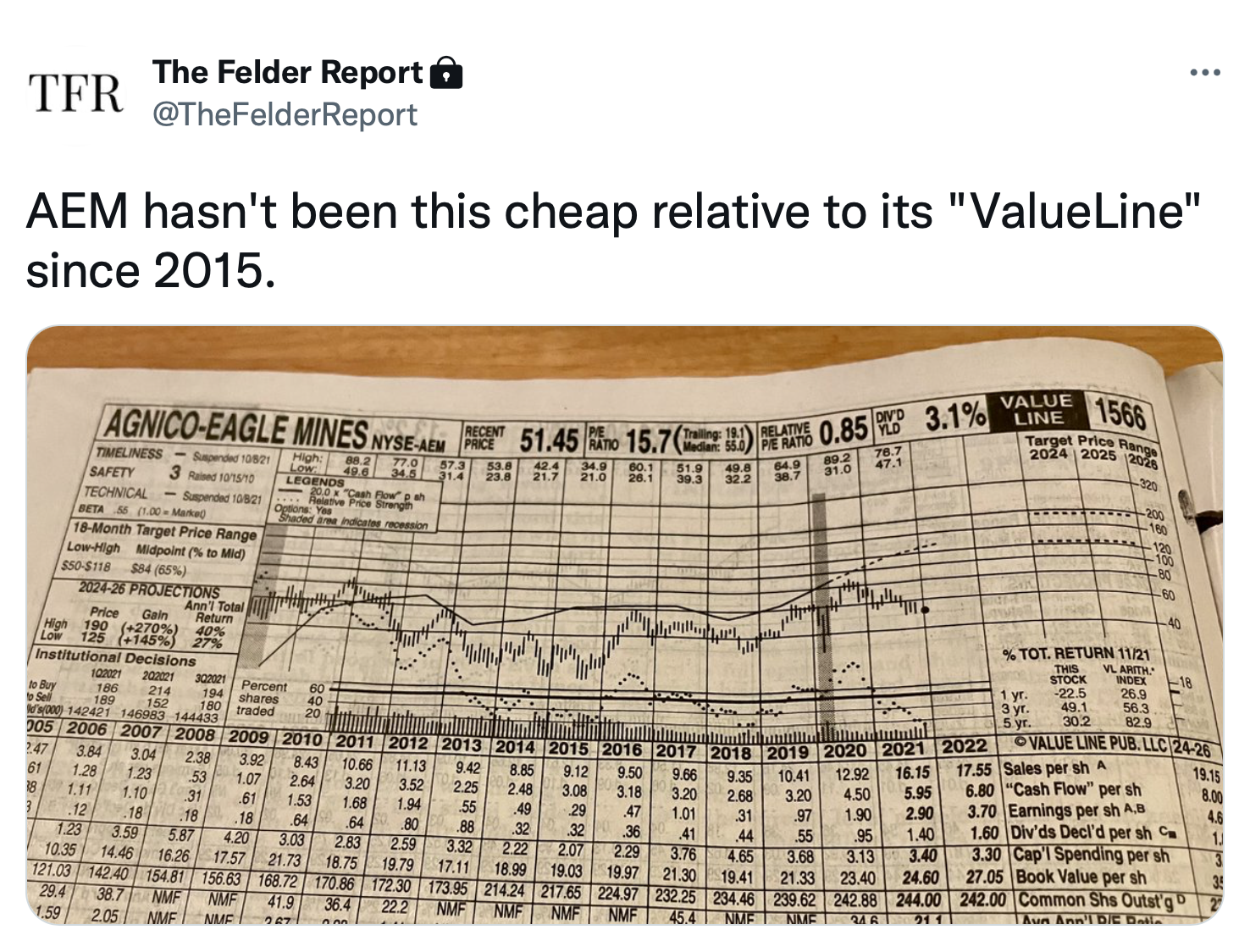

Yesterday, in doing research for this report, I tweeted a photo on our private twitter feed (request access here) of the ValueLine report for Agnico Eagle Mines, Ltd. (AEM), perhaps the highest quality major precious metals mining company in the world. Today the stock is up nearly 10%. I’m not suggesting my tweet had anything to do with that, of course. All I’m pointing out is that what appears on our twitter feed is regularly more timely than what I can possibly publish here. (I wish it were the other way around but such is the nature of the technology).

Yesterday, in doing research for this report, I tweeted a photo on our private twitter feed (request access here) of the ValueLine report for Agnico Eagle Mines, Ltd. (AEM), perhaps the highest quality major precious metals mining company in the world. Today the stock is up nearly 10%. I’m not suggesting my tweet had anything to do with that, of course. All I’m pointing out is that what appears on our twitter feed is regularly more timely than what I can possibly publish here. (I wish it were the other way around but such is the nature of the technology).

And, yes, I still read ValueLine. It’s something I’ve done since I first started researching stocks professionally 25 years ago. I look at it as an effective way to visually screen for value opportunities. In fact, some of my best investment ideas have come from just reading through these weekly reports looking for stocks that trade well below their “value lines.” And when I recently read the report covering the mining stocks I was struck by the discount to its own “value line” that AEM now trades at.

Typically, Agnico Eagle has traded at a premium to the precious metals mining group due to the superior quality of its mines and relative attractiveness of their locations. Today, however, the stock trades at a discount to Barrick and Newmont, the only two mining companies that produce more than Agnico Eagle does. Perhaps this is due to the fact that investors feel it is overpaying for Kirkland Lake, another miner it is in the process of acquiring. But, in my view, at just eleven times earnings, AEM is hardly overpaying and the acquisition only enhances the quality of the company’s portfolio of assets.

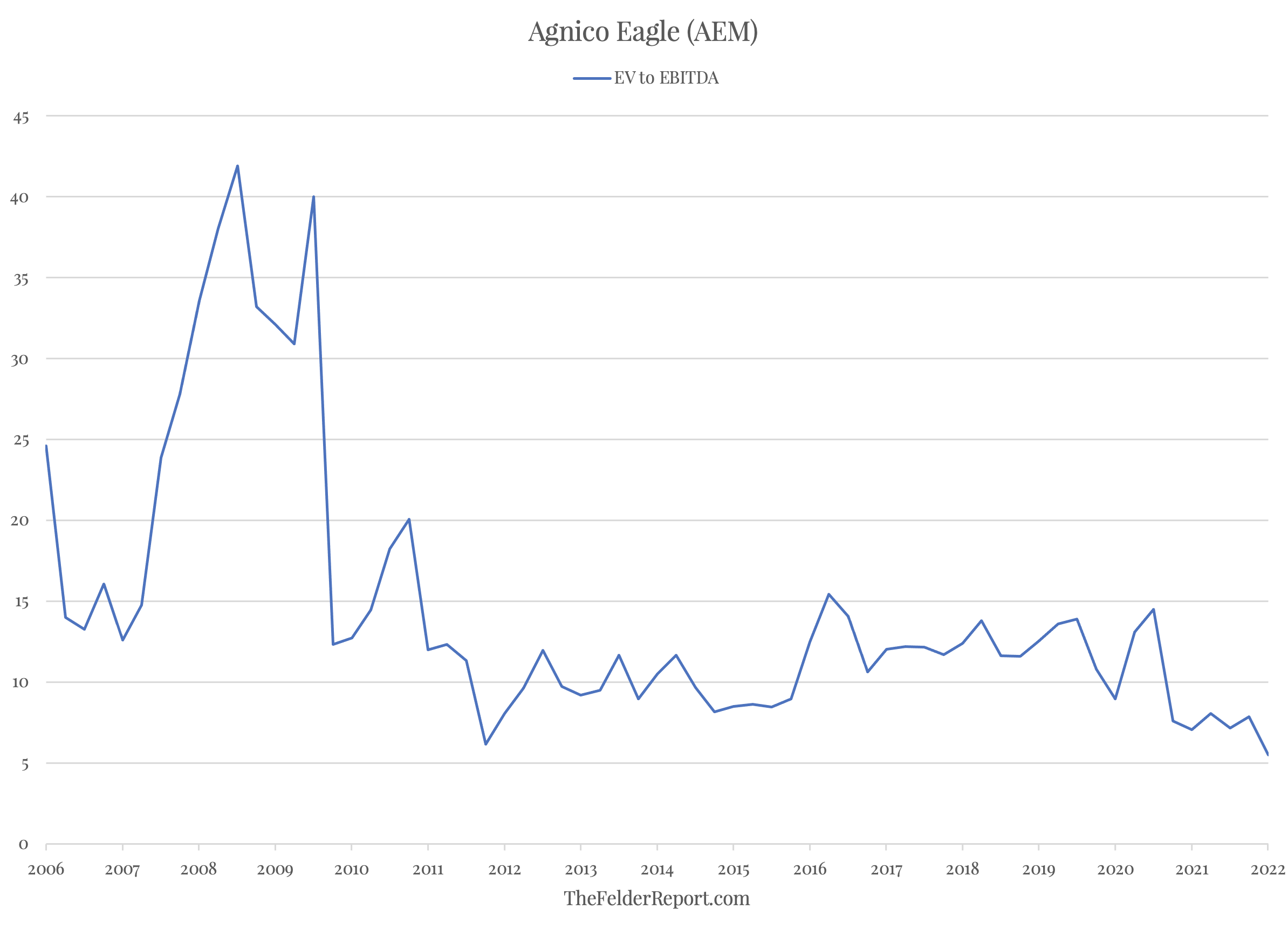

Currently, AEM trades at just five-times enterprise value-to-EBITDA. This is the cheapest the stock has been in at least 15 years. Over the past decade, AEM has traded between 10 and 15 times so you could argue the stock could double from its current level and still be cheap relative to its own history. And if the gold price resumes its bull market, as I believe it will, EBITDA will only continue to grow at a rapid rate, making today’s stock price that much cheaper.

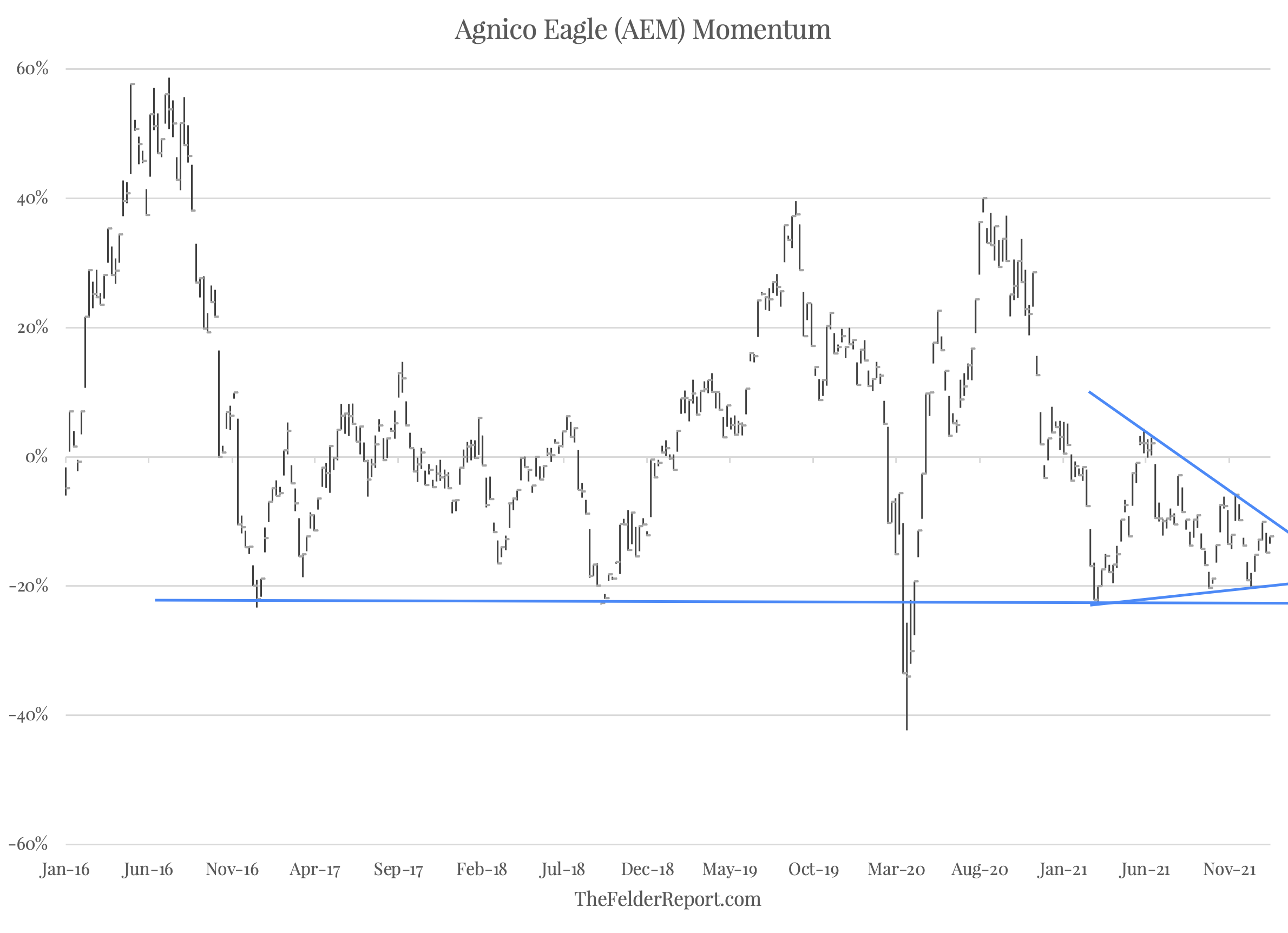

Technically, the stock has recently been testing long-term price support at the $50 level (and momentum support at -20% relative to the 40-week moving average). As the stock made new 52-week lows late last year, in the context of a bullish wedge pattern, momentum failed to confirm, leaving a bullish divergence. This suggests downside momentum is possibly waning just as the stock tests support, the sort stuff trading bottoms are made of.

{kind=link}

In bear markets and prolonged corrections you’re supposed to use the weakness to upgrade the “quality” of your portfolio. AEM appears to be the highest quality major miner in the world, now trading at a significant discount to not only the broad market and its peers but also to its own history. In addition to this fundamental “margin of safety”, AEM also shows technical signs of potentially reversing from downtrend to uptrend. As such, it looks like an attractive way to take advantage of a resumption of the bull market in gold prices.