While it seems most executives are offloading shares as fast as the market will allow, there is at least one CEO going the other direction. As I noted recently, the insider buying in the energy industry has been very significant lately. One of the places where it has been especially so is at Continental Resources (CLR), an oil and gas exploration and production company focused in the North Dakota and Oklahoma shale plays.

Harold Hamm founded the company back in 1967 at the ripe old age of 21. Today, he is a billionaire, executive chairman and the largest shareholder of CLR and he can’t seem to own enough of it. Since late June he’s bought over 10 million shares, worth roughly $178 million. As my friend Asif Suria noted at the time, this takes his stake in the company to over 80% of the total shares outstanding. In a press release related to his purchases, Hamm said:

I firmly believe Continental’s current share price reflects an uncommon value as the global pandemic has negatively impacted worldwide crude oil demand. Recent purchases underscore my confidence in the Company’s continued operational excellence and strong financial performance. Continental is poised to deliver significant shareholder value for many years to come and I believe there is no management team more aligned with shareholders than Continental.

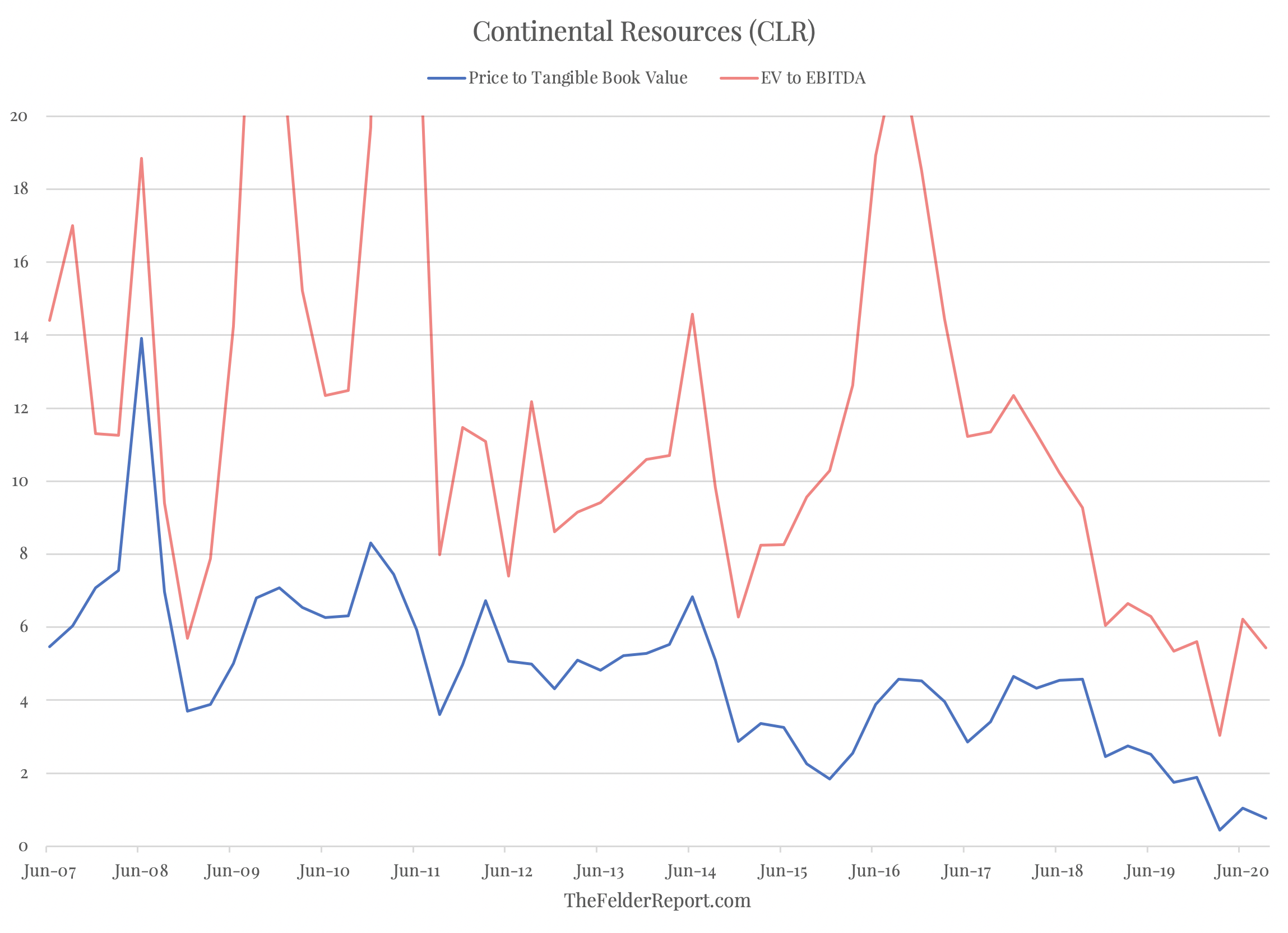

As to the “uncommon value” claim, the stock currently trades a just two times free cash flow. Looking back at its valuation history, the stock has really never been this cheap before based on price-to-tangible book value or enterprise value-to-EBITDA. To trade back to its historical averages based on these measures, the stock would need to rise from $13 per share today to $65.

CLR, like many others in the energy space, appears to be trading as if energy demand will never come back and will be permanently depressed going forward. Any upside surprise then in terms of demand could make for significant upside for the shares. Technically, the stock completed a weekly DeMark Sequential 9-13-9 buy signal back in March but has been unable to overcome its downtrend line dating back to late-2018.

But the pullback from this attempt at a trend line breakout has now retraced 61.8% (Fibonacci) of the gains from the March low. This level ($12.5) also coincides with minor short-term support dating back to May and June so this looks like a good spot for the shares to stabilize and try to embark on a new leg higher, building off of the March low.

In total, CLR looks like an attractive opportunity within a sector that presents an unusually attractive opportunity on its own. More conservative investors may want to wait for a break of the longer-term downtrend line before making a commitment. However, it may not hurt to start nibbling now with a plan to add either on a breakout or a test of the March lows.