I’m hearing a lot of folks these days draw attention to the fact that the dividend yield on the S&P 500 (2.17%) is now greater than the yield on the 10-year treasury note (1.7%). In doing so, they are obviously making the case that stocks are undervalued relative to bonds.

There are a few problems with this line of thought. First, just because the dividend yield is currently higher than the 10-year treasury yield doesn’t mean stocks will necessarily outperform risk-free treasury notes going forward. If you hold that treasury note to maturity you know exactly what you’re going to get over that time. The same can’t be said for owning stocks which carry far more risk.

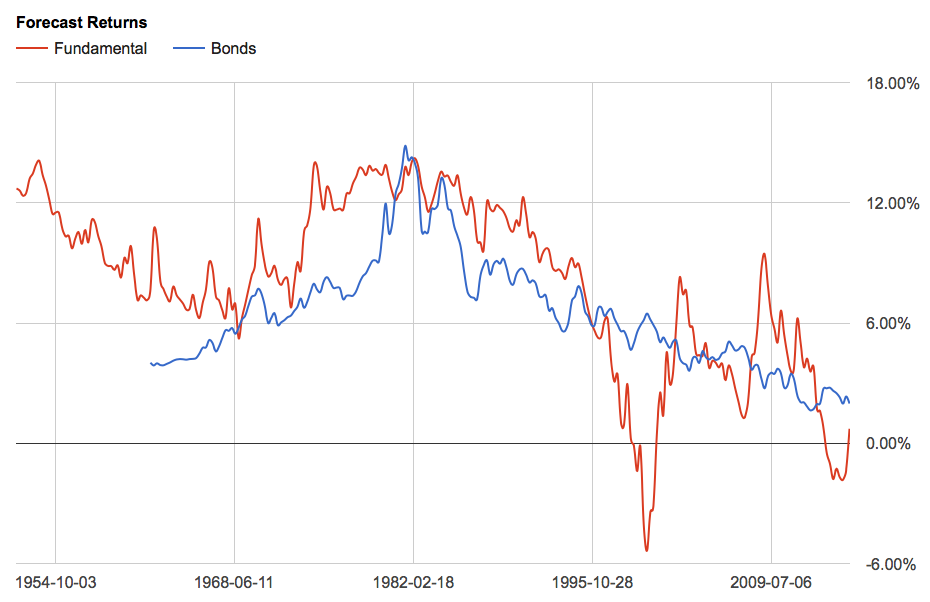

To get an idea of what to expect from stocks, you need to study valuations. Personally, I like to use the Buffett Indicator (market cap-to-GDP) because it’s about 90% negatively correlated to 10-year future returns. History shows that the higher starting valuations are the lower your future returns will be and vice versa. This has been true regardless of where interest rates have been or where they are going.

Right now valuations, based upon this measure, suggest the total return from owning stocks is likely to be less than the risk-free return on 10-year treasury notes. So why, you might ask, should you take far more risk in owning stocks when you are likely to do better in risk-free treasuries? Good question.

Some might say that high valuations today are justified by low interest rates. And this is really the case folks are making when they compare the dividend yield in owning stocks to the interest rate on the 10-year treasury note. Well, there are a few guys plenty smarter than I am that have demonstrated why this is such a, ‘dumb idea.’ I would mainly direct you to Cliff Asness’ now classic treatise on the subject, “Fight the Fed Model.”

To boil it down to the simplest argument, Cliff shows that low interest rates imply low future inflation and concomitant low earnings growth. High valuations in equities, on the other hand, imply high future growth. Thus, the idea that low interest rates, which imply low growth, somehow justify high valuations, which are completely dependent upon on high-growth, is faulty, at best.

Note to Fed Modelers: Japanese stocks yield infinity more than their 10-year bond.

— Jesse Felder (@jessefelder) February 10, 2016

But probably the best real world example of the inanity of this argument is the experience of Japan over the past couple of decades or so. The interest rate on the Japanese 10-year bond in 1990 was 7%. At the same time, the Nikkei stock market index stood at 39,000 and carried a CAPE ratio of 90. Today, that yield has fallen from 7% to below zero. At the same time, the Nikkei has fallen 60% to 16,000 and a CAPE ratio of 25.

Over the past 25 years, then, both interest rates and stock market valuations have fallen together. According to the Fed Model, this should never happen. Intuitively, though, it makes perfect sense. Japanese inflation and economic growth have fallen dramatically over that time so both of these asset classes have reflected this development in their valuations.

If the Fed Model were a viable way to forecast equities, Japanese stock market valuations should have soared in reaction to such an massive drop in interest rates. In fact, according to the Fed Model, Japanese equity valuations should have no upper limit today. At the very least, they should be trending higher as interest rates have trended lower yet just the opposite has happened. Sadly, even massive buying of equities by the Bank of Japan, which now owns more than half of the country’s outstanding equity ETFs, hasn’t been enough to make this theory a reality.

So even though it’s been demonstrated to be false in both the academic realm an in the financial markets, that clearly hasn’t stopped investors from continuing to embrace it and making costly errors in the process. But before you go buying stocks believing that falling interest rates will support prices you might want to ask yourself this very basic question: “Are plunging interest rates and, perhaps more importantly, a plunging yield curve bullish signs for economic and business fundamentals?” Because those are what really matter to stock market valuations, not some theory that both defies common sense and also has no historical validation anywhere in the real world.