Below are some of the most interesting things I came across this week. Click here to subscribe to our free weekly newsletter and get this post delivered to your inbox each Saturday morning.

LINK

As my friend Eric Cinnamond writes, “the affordability crisis was created by an extended period of elevated debt growth, fiscal deficits, and a Federal Reserve determined to keep the cycle going through rate cuts, debt monetization, and perpetual bull markets. In other words, too much easy money, too many asset bubbles and bailouts, and a government that hasn’t faced sufficient pressure to rein in unsustainable spending.”

CHART

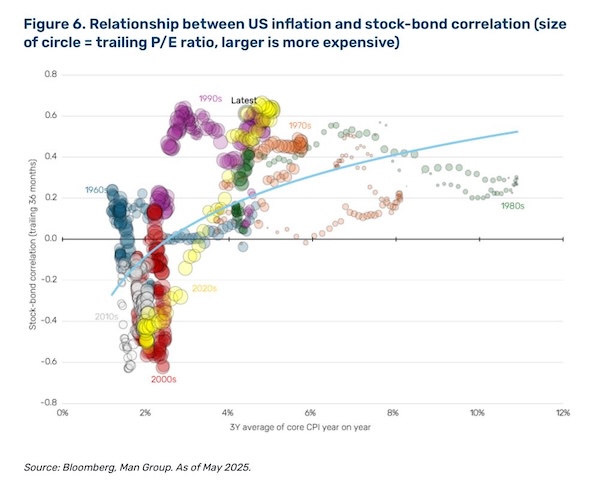

All of these unsustainable trends are now potentially reaching their limits, pointing to the possibility of major changes for markets and economies in the years ahead. “What does regime change out of secular stagnation look like on this framework? Certainly inflation remaining above 3% on a smoothed basis. Certainly stock-bond correlation staying above +0.2 on a smoothed basis. Probably also semi-regular excursions above 5% inflation, with consequent multiple compression,” writes Man Group’s Henry Neville.

STAT

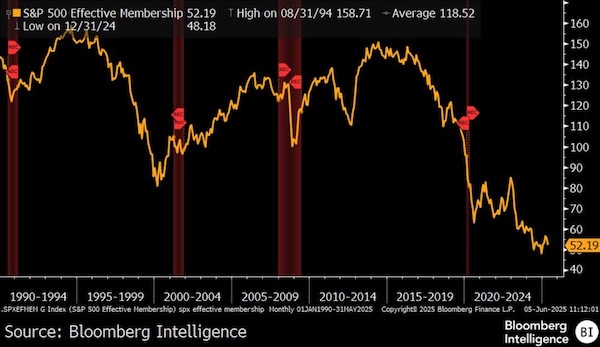

A U.S. stock market more highly-leveraged than ever to the old regime looks especially vulnerable to this sort of development. As Bloomberg’s Gina Martin Adams notes, “The S&P 500 is the most concentrated it’s ever been… The effective membership is 52.2 and has been falling since its June 2014 high of 150.4 — 2.2 standard deviations below the average since 2000.”

CHART

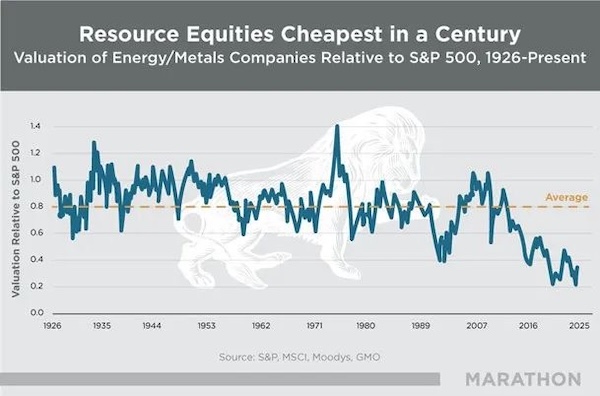

There are areas, however, within the broad stock market that are both deeply undervalued and well-positioned to benefit from the new regime. As my friend David Hay writes, “natural resource shares are exceptionally cheap relative to the S&P 500. This sector appears to be basing since 2020. If so, it may be establishing a springboard to generate market-beating returns over the balance of this decade.”

STAT

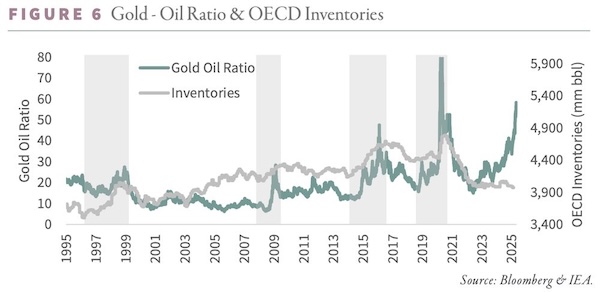

Within the natural resource space, energy looks uniquely attractive. “Since 1990, the median forward 12-month return for spot WTI crude has been about 4%. But when oil has traded at these kinds of relative discounts—when an ounce of gold buys more than 25 barrels—that median return has jumped to 30%,” writes Goehring & Rozencwajg.