Below are some of the most interesting things I came across this week. Click here to subscribe to our free weekly newsletter and get this post delivered to your inbox each Saturday morning.

LINK

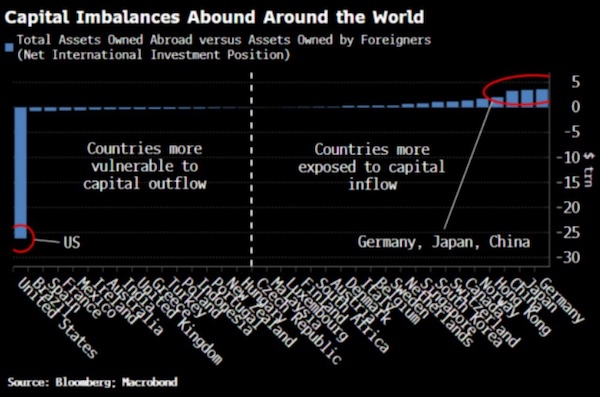

Sifting through the noise surrounding the trade war, it’s clear that a reordering of global trade is underway with the intent of reducing unsustainable imbalances. “Many are recognizing that whatever happens with tariffs, these problems won’t go away, and that radically reduced interdependencies with the U.S. is a reality that has to be planned for,” writes Ray Dalio.

CHART

However, it’s important to remember that, as Simon White points out, “Tariffs should reduce the US’s trade and current-account deficits. That means financial-account imbalances will fall, too. Countries in which foreigners own more assets than they themselves own abroad (US) are exposed to capital outflows and fx declines.”

LINK

Moreover, some of the non-tariff remedies proposed for to reducing these imbalances are already creating a growing sense of unease among foreign holders of dollar-based assets. “In Chinese academic and policy circles, it is the suggestion of a selective US default that is most alarming — and some influential scholars are now advocating a move towards outright de-dollarisation, rather than gradual adjustments to the mix of assets,” reports the Financial Times.

LINK

To the extent that increased globalization was good for both economic growth and persistent disinflation, the reversal of that trend threatens to undo those benefits. As Stephen Roach writes, “The fracturing of global trade, when coupled with US President Donald Trump’s attacks on central-bank independence and preference for a weaker dollar, threatens a prolonged period of stagflation.”

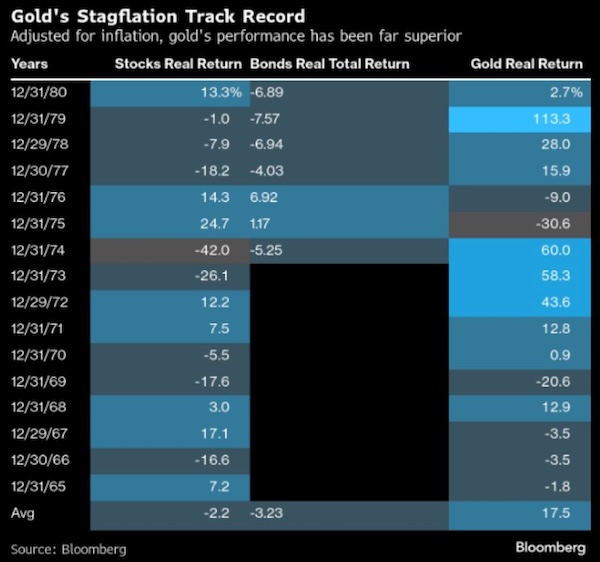

STAT

For investors, this shift in the underlying macro environment has important implications for asset allocations. “Stagflation in the 1970’s offers plenty of evidence that gold can outperform in such an environment — and it’s precisely what’s been underpinning its stellar rally this year,” notes Bloomberg. The evidence regarding the performance of financial assets, like stocks and bonds, is clearly less benign than that for real ones.