Below are some of the most interesting things I came across this week. Click here to subscribe to our free weekly newsletter and get this post delivered to your inbox each Saturday morning.

STAT

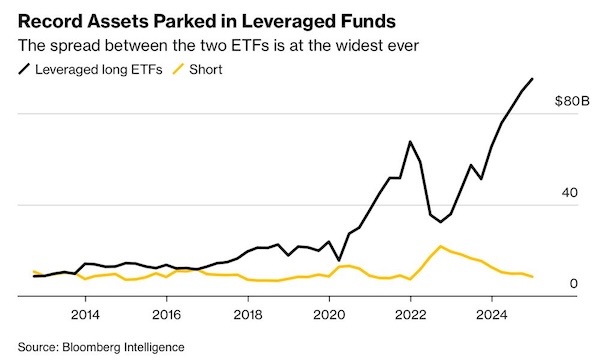

The appetite for leverage in the stock market currently appears insatiable. “Retail daredevils — undeterred by recent Wall Street jitters over AI and crypto — are going long, pumping up leveraged funds to nearly $100 billion, while pessimistic market wagers languish,” reports Bloomberg.

LINK

As Ruchir Sharma explains, “The longer the bull run lasts, the more investors feel emboldened to buy any dip… The bailout culture dates to the first rescue of a major US bank in 1984, and the first explicit Fed vow to prop up the stock market in 1987. Since then, rescues have grown more generous and automatic, encouraging greater speculative frenzies and steadily rising market valuations. Investors have come to see risks as asymmetric, with a state cap on losses and no limit on gains.”

CHART

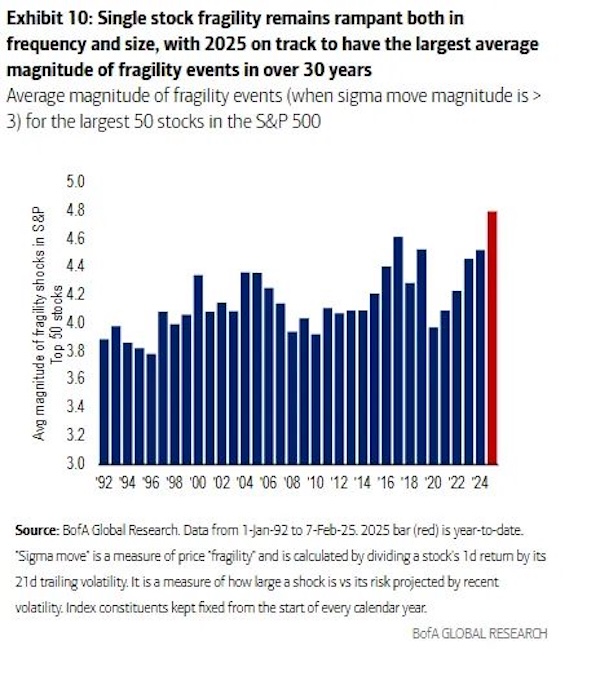

But there are growing signs within the stock market that suggest the success of BTFD may not be as successful going forward as it has been in the past. According to Bloomberg, “Rising instability among some of the biggest US stocks is driving a measure of single-stock ‘fragility’ to record levels, with the market increasingly vulnerable to whipsaw patterns among clusters of shares such as occurred in the dot-com bubble of the late 1990s.”

LINK

Furthermore, the “ripple effects of DeepSeek,” have only just begun to spread outward. As Peter Garnry writes, “If open source AI wins and more efficiency gains can be innovated in AI models the narrative of AI only being possible with ever more powerful Nvidia GPUs collapses.”

LINK

At the same time, many alternatives to the Magnificent 7 are starting to look more attractive. “Just a few months ago, the perception was that the only place to deploy capital safely was in a handful of US mega-cap tech names and gold. Fast forward to today and one can make a cogent case for US treasuries, LatAm debt and equities, Chinese equities, European equities, infrastructure plays and commodities. Suddenly, the investment landscape is more interesting than it has ever been,” writes Louis Vincent-Gave.