“Whenever you find yourself on the side of the majority, it is time to reform (or pause and reflect).” -Mark Twain

One of the simplest but most important lessons an investor can learn is this: capital follows returns; returns don’t follow capital. In other words, money comes into a sector only after it has had a terrific run in terms of investment performance. Furthermore, that influx of new money necessarily means that the run of terrific performance will soon come to an end.

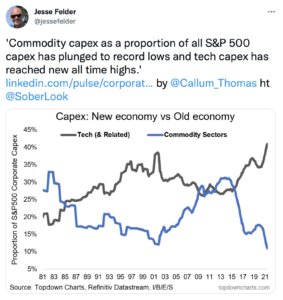

A chart recently shared by Callum Thomas illustrates this point. First look at just the blue line, which represents the proportion of capital expenditures made by commodity sectors as a share of total spending by S&P 500 companies. In 2000, after a long period of under-performance which saw capital flee the sector, commodity sectors put in a major bottom as valuations became very cheap and the lack of investment resulted in a dearth of supply which supported prices.

A chart recently shared by Callum Thomas illustrates this point. First look at just the blue line, which represents the proportion of capital expenditures made by commodity sectors as a share of total spending by S&P 500 companies. In 2000, after a long period of under-performance which saw capital flee the sector, commodity sectors put in a major bottom as valuations became very cheap and the lack of investment resulted in a dearth of supply which supported prices.

Over the coming decade, these stocks outperformed the broad stock market in dramatic fashion. This eventually attracted a great deal of capital in the early-2010’s. That influx of money resulted in significant over-valuation of the stocks as well as over-investment in production which eventually led to oversupplies and a crash in prices.

Now look at the gray line, which represents the proportion of capital expenditures made by the tech sector as a share of the total. In 2000, as commodity sectors were largely being shunned by investors, the tech sector’s terrific performance over the prior decade led to a massive inflow of capital. The result was extreme over-valuation of tech stocks as well as massive over-investment in capex. That combination precipitated a crash not long afterwards.

The dearth of investment that came about as the result of the tech crash, however, set the stage for a reset in both valuations and in the overall supply of tech products and services. And just as commodity sectors were in the process of peaking, the tech sector was beginning to take off again on another stretch of incredible performance.

Today, the situation looks very much like it did just over 20 years ago. The technology sector’s terrific run has attracted another massive inflow of money that has pushed up valuations and has been invested into greatly expanding the availability and breadth of tech products and services. At the same time, commodity sectors have been starved of capital, resulting in deeply discounted valuations and a severe restriction of investment in supplies.

If history is a guide, the coming years should see terrific returns in commodity sectors once again and terrible returns for the tech sector. That’s just the natural result of the trends in the flow of capital in recent years. Investors will eventually come around to this way of thinking. But, by the time they do, it will likely be time to go the other way yet again.